%20the%20world's%20rendezvous%20for%20startup%20and%20leaders%20by%20Frederic%20Legrand.jpg)

Presently, Meta Platforms (META) is not facing a broken business. It is facing a tougher kind of investor question. Can it keep growing fast while spending heavily on AI and trimming costs at the same time? Reuters reported that Meta plans a first wave of layoffs starting May 20, with more cuts later in 2026. The move comes as the company tries to stay lean while funding its AI push.

That matters because Meta still sits in a powerful spot. It controls Facebook, Instagram, WhatsApp, and Threads, and that family of apps still gives it one of the biggest advertising engines in the world. Meta is also leaning hard into generative AI and Reality Labs, which keeps the story exciting but also expensive.

What makes Meta different

Meta is not just another big tech company. It has scale, reach, and advertising power that few rivals can match. Nearly 4 billion users move through its ecosystem, and that gives Meta a direct line to advertisers across the globe. At the same time, it is pushing into AI, smart glasses, and spatial computing, so the company still has room to reinvent itself.

In January, it signed a multiyear deal with Corning (GLW) worth up to $6 billion for fiber and connectivity tied to U.S. data centers. It also partnered with Oklo (OKLO) on a nuclear power campus in Ohio to help support future AI data center demand. Those moves show Meta is building the infrastructure for a much larger AI push.

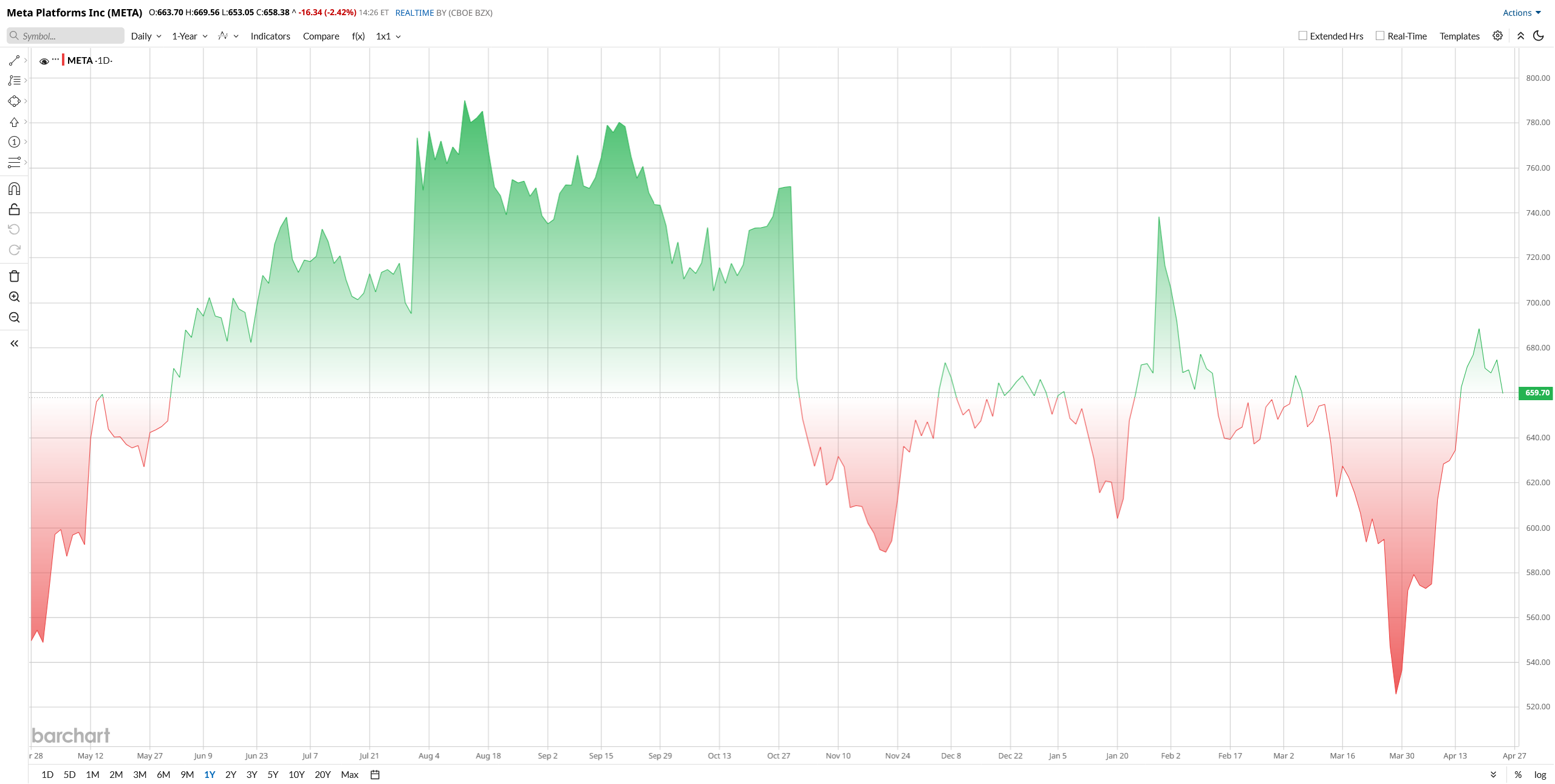

The stock has been okay in 2026, but not amazing. Meta's shares were up 3% for the year as of mid-April, though they were still below last summer’s peak and have since flatlined year-to-date (YTD). Barchart’s technical data shows the stock near $660, above its 50-day average of about $630 but below its 200-day average of about $681. That is not a bad setup, but it does show the stock is still trying to find its footing.

Meta does not look inexpensive. Barchart puts its forward P/E around 21 times, versus a sector median closer to 13 times. Its EV to EBITDA is about 15 times, while the peer average sits near 11 times. That means investors are still paying up for growth, even after the recent spending pressure.

Why the Layoff News Matters

The layoffs are not a business crisis on their own. They are more of a signal. Meta is telling investors it wants to run tighter while it keeps pouring money into AI infrastructure. Barchart described the move as a kind of restructuring by choice, and that is probably the right read. Investors liked the idea enough for the stock to edge higher after the news. The message is simple. Meta aims to protect margins without slowing its AI roadmap.

Still, cuts can change sentiment fast. If investors start thinking Meta is trimming because growth is slowing, the tone shifts. For now, the market seems to view this more as discipline than distress.

The Latest Quarter Still Looked Strong

Meta’s latest reported quarter was strong. In Q4 2025, revenue rose 24% year-over-year (YoY) to $59.89 billion, while full-year 2025 revenue climbed 22% to $200.97 billion. Net income was $22.77 billion in the quarter and $60.46 billion for the year. Operating income reached $24.75 billion in Q4 and $83.28 billion for the full year.

There was plenty to like underneath the surface, too. Family Daily Active People averaged 3.54 billion, showing the user base is still massive. Reality Labs revenue jumped 74% to $470 million, helped by Quest demand and AI-enhanced smart glasses, although the unit still loses money. Meta also said a new runtime model across Instagram Feed, Stories, and Reels lifted conversion rates by 3%.

CEO Mark Zuckerberg summed up the mood by saying, “We had a strong business performance in 2025. I’m looking forward to advancing personal superintelligence for people around the world in 2026.”

What To Watch in the Next Report

Meta is set to report first-quarter 2026 results on April 29. Analysts expect about $55.36 billion in revenue and adjusted EPS of around $6.71. That is a high bar, because Meta has been posting big numbers, and investors now expect the company to keep delivering.

The next report should tell investors whether ad pricing stays strong, whether AI tools keep lifting conversion rates, and whether heavy spending starts to squeeze margins. Meta also said 2026 capex will be much higher as it builds out data centers and superintelligence infrastructure, so cost control matters more than ever.

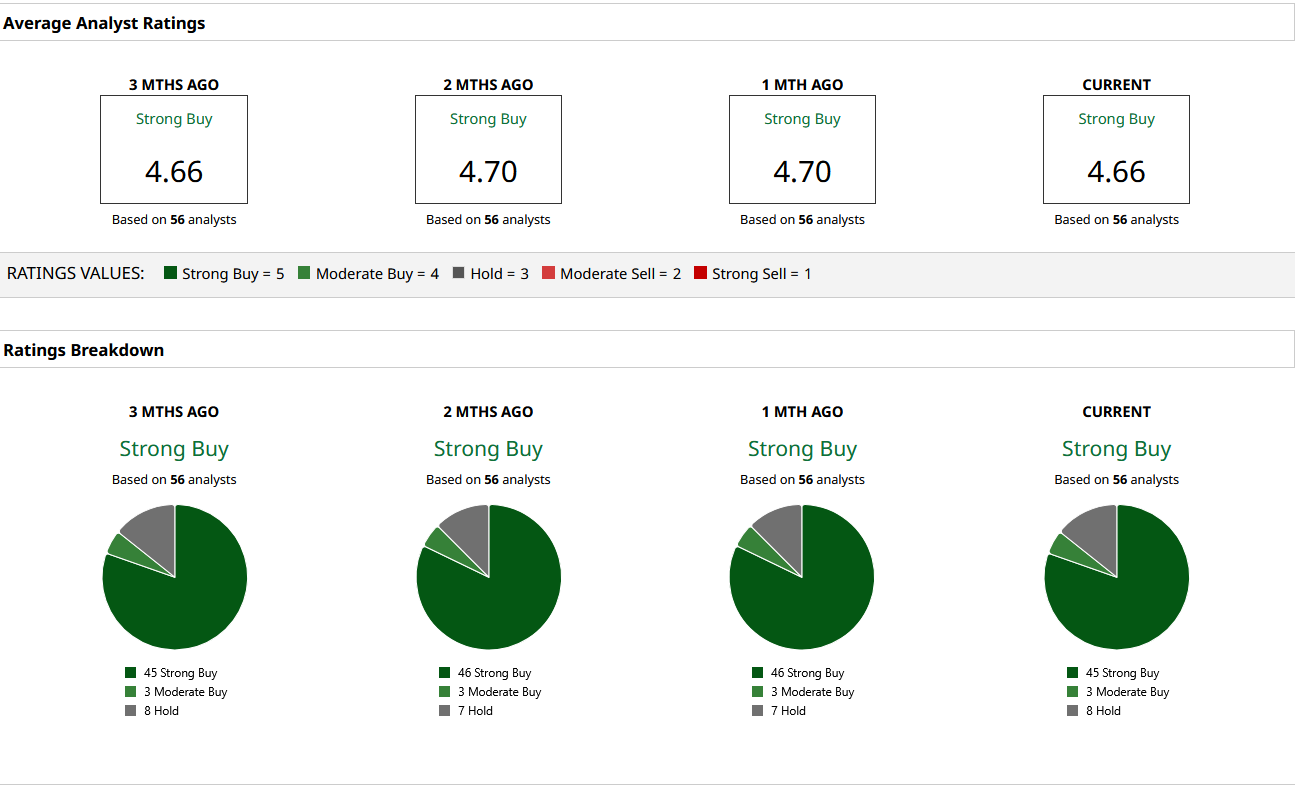

What Does Wall Street Think of META Stock?

Wall Street is still pretty bullish on META stock. BofA lifted its target to $885 and called Meta an infrastructure powerhouse that could turn free cash flow positive in 2026.

Overall, analysts have a “Strong Buy” consensus with an average price target of $853.87, implying about 30% upside. That is a strong vote of confidence, even with the stock looking expensive.

So in conclusion, the layoffs are not a sell signal by themselves. They look more like a smart cleanup move. But with META stock already priced for a lot of good news, investors may want to see the April 29 report before getting more aggressive.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)