In a market dominated by artificial intelligence (AI) giants and semiconductor heavyweights, smaller tech companies often get overlooked, even when their fundamentals are improving rapidly.

Here’s one data intelligence company and a forgotten telecom tech player that Wall Street is starting to notice.

Tech Stock #1: NIQ Global Intelligence (NIQ)

Valued at $3.4 billion by market capitalization, NIQ Global Intelligence (NIQ) is a data analytics and market intelligence company. It collects massive amounts of data from retailers, online platforms, and shoppers, then uses analytics and AI to turn that data into insights. These insights help businesses make pricing, product launch, marketing, and inventory decisions.

While NIQ stock has underperformed the broader market and dipped 30% year-to-date (YTD), analysts see huge potential upside going forward.

NIQ has deeply embedded AI into both its products and internal operations. The company processes an enormous scale of consumer data, covering approximately $7.4 trillion in global spending. Its systems process nearly 4 trillion data records every week, resulting in a huge and constantly updated intelligence layer for clients. This data advantage generates a significant moat. The company's revenue is consistent and predictable due to its subscription-based business model. In 2025, organic revenue grew 5.7% year-over-year (YOY) to $4.2 billion. Net dollar retention rate stood at 105%, indicating that existing consumers are sticking but also increasing their business with the company.

Notably, its AI-driven segments are expanding much faster. E-commerce revenue increased by 32% in 2025, while newer AI-powered analytics solutions are witnessing double-digit growth rates. Customers' data consumption increased by over 30% YOY and more than 60% of NIQ's top clients have already implemented at least one AI-native solution. Furthermore, AI automation has reduced data processing costs by up to 70% in certain markets and improved engineering productivity by roughly 10%. These cost efficiencies have boosted profitability for the company. Adjusted net income stood at $61.9 million in 2025, compared to a loss of $149 million a year ago.

As a result of improving profitability and cost efficiencies, the company also generated $334.5 million in unlevered free cash flow (FCF) and plans to generate $235 million to $250 million in FCF in 2026. The company is also working on using FCF to actively reduce debt. This combination of rising cash flow and declining leverage strengthens the balance sheet, allowing the company to engage in growth projects or make smart acquisitions.

Analysts predict that NIQ’s earnings will increase by 322% in 2026, followed by 23% growth in 2027. The stock is still undervalued at 13.5 times forward earnings as the market hasn’t recognized the scale of its AI opportunity. As AI progresses from experimental to real-world application in areas such as pricing, product development, and marketing optimization, NIQ's platform becomes increasingly important. NIQ is transforming from a standard data company into an AI-powered intelligence platform. This is most likely why analysts believe NIQ stock has significant upside potential going forward.

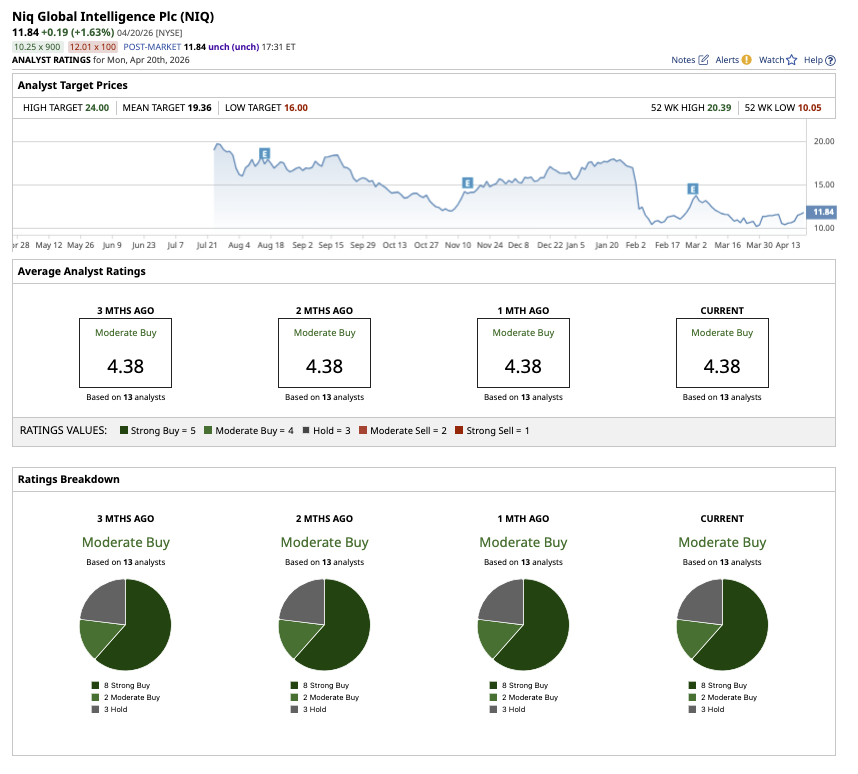

Analysts have a mean target price of $19.36 for NIQ stock, which implies potential upside of 69% from current levels. Plus, the high price estimate of $24 implies the stock can rally as much as 109% over the next 12 months. Still, despite the strong upside potential, NIQ carries risks. The company operates in a competitive market, and maintaining its technological edge will require continuous investment.

Overall, NIQ holds a consensus “Moderate Buy” rating on Wall Street. Out of the 13 analysts covering the stock, eight have a “Strong Buy,” two recommend a “Moderate Buy,” and three analysts have a “Hold" rating.

Tech Stock #2: Allot Communications (ALLT)

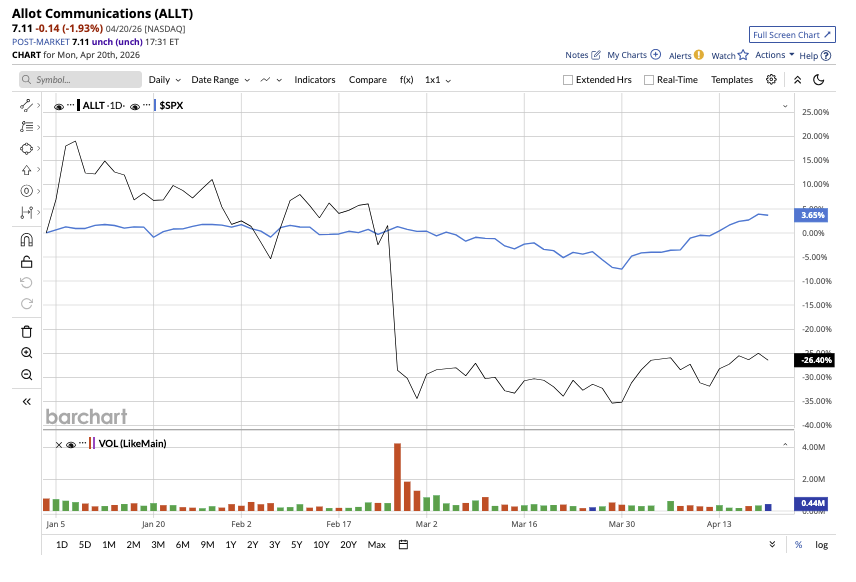

Valued at $350 million by market cap, Allot Communications (ALLT) is a network intelligence and security company for telecom operators. It helps mobile carriers and internet providers monitor, manage, and secure their network traffic. After years of struggling, Allot is finally undergoing a structural transformation that analysts are optimistic about. With rising recurring income, expanding margins, and a rapidly growing cybersecurity market, some analysts believe ALLT stock could return more than 75%. That's despite the stock falling 25% YTD.

Allot is transitioning to a cybersecurity-first company by providing cybersecurity services directly across telecom networks. Its Security-as-a-Service (SECaaS) platform has emerged as the key growth driver, allowing telecom carriers to give consumers built-in security capabilities. This move has resulted in a subscription-based, recurring revenue model that improves the company's visibility and stability. In 2025, more than 60% of total revenue came from recurring sources, with total revenue increasing 11% YOY to $102 million. Its SECaaS annual recurring revenue (ARR) surged 69% YOY in December to $30.8 million.

Each new telecom agreement significantly increases Allot's addressable market. When a carrier uses its platform, the firm gains immediate access to potentially millions of end consumers. Allott is actively growing its global partnerships and, while the company has a lot of potential in the fast-developing cybersecurity space, it is also a extremely competitive market. As the firm continues to scale its recurring revenue segment, its business will become more resilient. Adjusted EPS rose by a staggering 475% YOY to $0.23 in 2025. Margins also improved, with gross margins expanding to around 72%. Allot Communications ended the year with $88 million in cash and zero debt, giving it a strong financial foundation to invest in growth initiatives.

This combination of growth, profitability, and balance-sheet strength is rare among small-cap tech stocks. This is probably why analysts are turning bullish on ALLT stock. Analysts predict that Allot’s earnings will increase by 34% in 2026, followed by 31% growth in 2027. ALLT stock is valued at 33 times forward earnings due to its evolving business model and the broader AI megatrend.

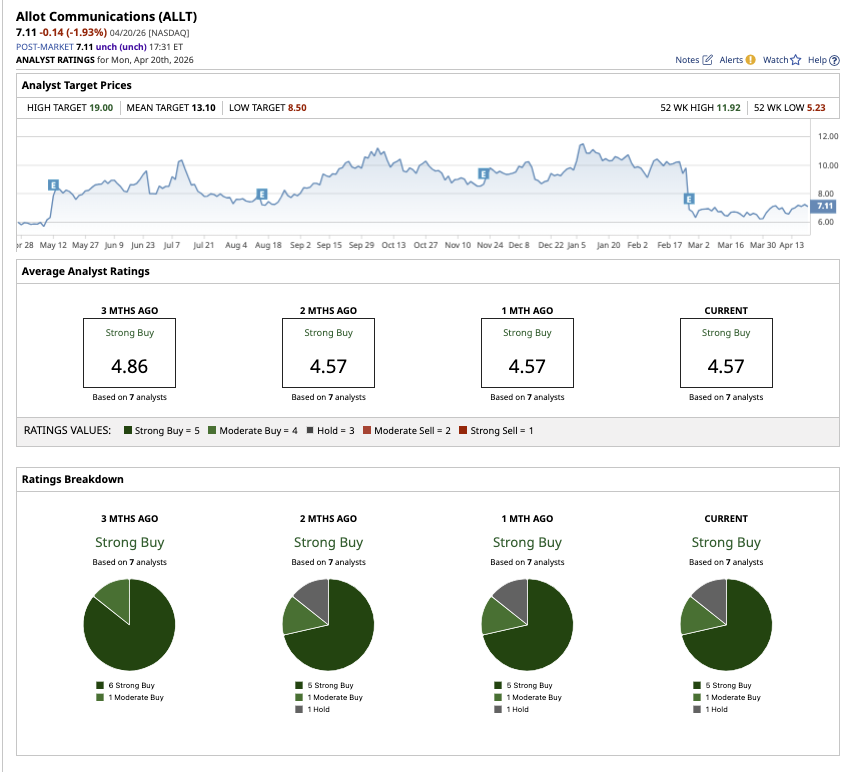

Analysts have a mean price target of $13.10 for ALLT stock, which implies potential upside of 78% from current levels. Plus, the high price estimate of $19 implies the stock could rally as much as 158% over the next 12 months. Overall, ALLT stock holds a consensus “Strong Buy” rating on Wall Street. Out of the seven analysts covering the stock, five have a “Strong Buy,” one recommends a “Moderate Buy,” and one analyst has a “Hold" rating.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)