/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

PayPal has fallen a long way, and that is exactly why people are paying attention again. The company used to be one of the biggest winners in digital payments, but the story looks very different now. PYPL stock is down roughly 15% over the past year while over the last five years it has lost about 80% of its value. That kind of drop has turned PayPal into one of the cheaper big fintech stocks in the market, with shares currently trading near the $50 level.

This is usually the kind of setup that attracts strategic buyers hunting for an acquisition target. PayPal is still a big global payments company and remains solidly profitable, reporting full-year 2025 net revenue of $33.2 billion along with GAAP net income of $5.23 billion. Full-year GAAP EPS came in at $5.41, up 35% year-over-year (YOY). But the stock price demonstrates that investors have lost confidence. When that happens, outside investors often start to think there is value to unlock.

That is why recent moves in the market matter. On April 17, PayPal jumped about 3% in one day after a Gordon Haskett note said SG Americas, a broker often linked to activist activity, seemed to be building swap exposure in PYPL stock. That was enough to get the rumor mill going again.

Is PayPal really becoming an activist target or even a full-blown acquisition candidate? Let’s take a closer look.

PayPal Looks Like Prime Activist or Acquistion Bait Right Now

PayPal looks like classic activist bait right now because the gap between what it promised and what it delivered is now spelled out in lawsuits. In early 2025, management told investors it could lift branded total payment volume growth to around 8% to 10% by 2027.

Less than a year later, those targets were scrapped, the CEO was pushed out, and more than $9 billion of PayPal's market capitalization vanished as the stock reset to a harsher reality. Investors’ lawyers now argue that PayPal did not clearly warn about weak branded-checkout trends or rising pressure from rivals while it was selling the growth story.

All of that has turned into a wave of securities class actions and calls for investors to step up as lead plaintiffs. The suits claim PayPal overstated how well it could execute on its plans and played down the real risks around competition and delivery while talking about 2027 goals.

Several law firms are seeking shareholders who bought between February 2024 and February 2026 and then took losses, all pointing to the same breaking point when guidance was pulled, management admitted branded-checkout execution was poor, and the leadership shake‑up hit the news. Many notices repeat the same April 20 deadline to seek lead‑plaintiff status, which shows how many investors feel burned and are now formally organizing.

On top of that, the focus is turning to the people in charge. At least one notice says that both former CEO Alex Chriss and CFO Jamie Miller could face personal liability in the securities case. Another update confirms that former Square chief executive Alyssa Henry will join the board while long-serving director Gail McGovern will step down. That mix of legal heat on senior executives and visible change in the boardroom is exactly the kind of setup that activists look for.

How Should PYPL Stock Be Played Amid the Rumors?

The best way to look at PayPal right now is not as a done deal, but as a stock-trading possibility. Some analysis around the takeover talk has pointed out that any serious buyer would probably have to offer a premium to the current price.

That includes chatter around possible interest from Stripe, which would be a logical rival to explore a deal. At the same time, other views built around the Stripe rumors have stressed that takeover talk on its own does not repair PayPal’s slowing growth. These rumors might move the share price fast, but they do not make the branded-checkout issues or legal problems disappear.

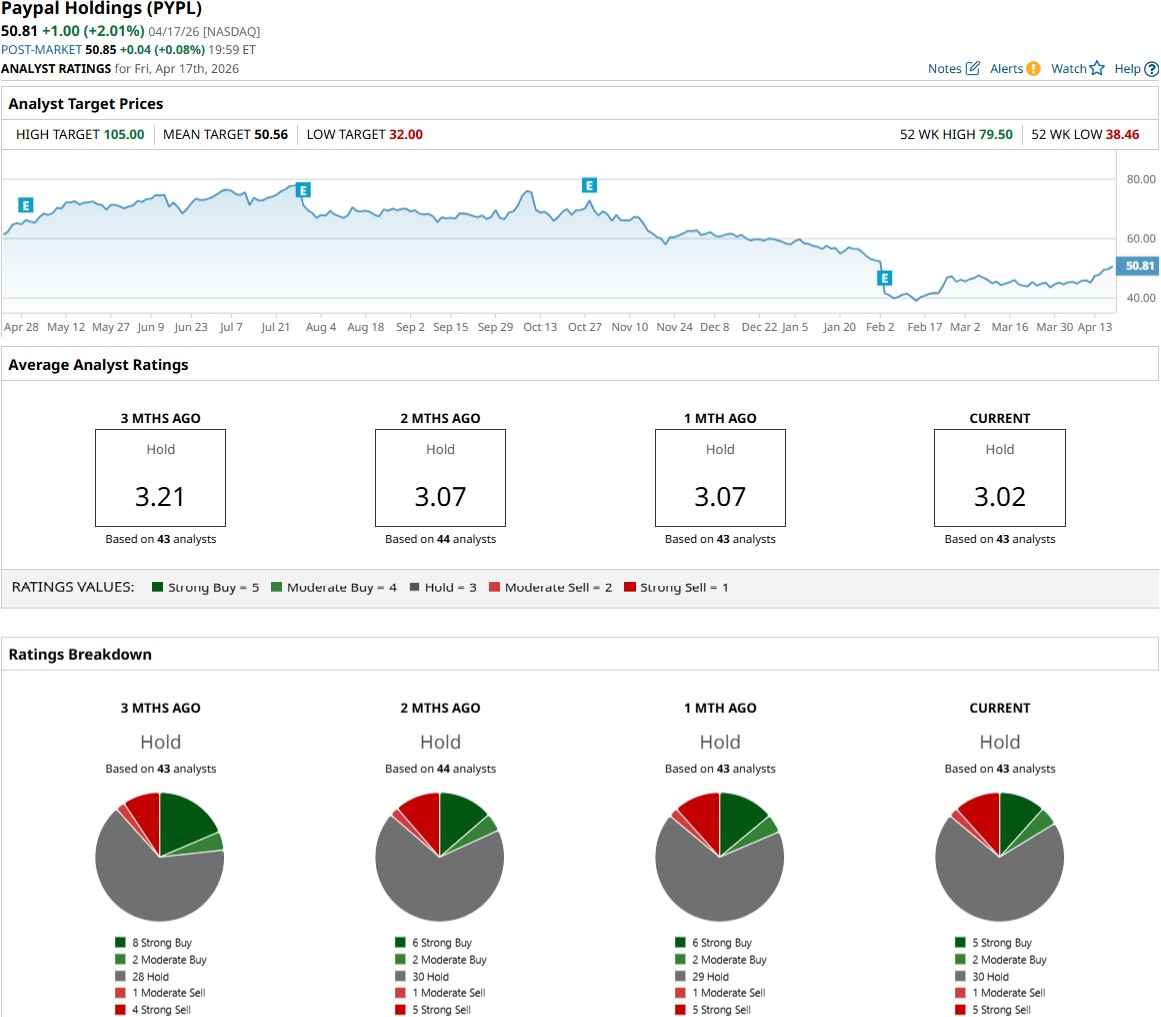

Analyst views reflect that caution, as 43 analysts rate PYPL stock as a consensus “Hold.” The average price target sits at $50.70, which is roughly in line with current prices. That tells the story clearly, as Wall Street is not betting on much upside unless something more concrete happens.

Conclusion

PayPal has all the ingredients of a classic activist or takeover story, but for now, it is still trading mostly on talk rather than firm offers. The combination of a cheap share price, mounting lawsuits, and visible boardroom changes should give PYPL stock a gentle push higher over time, although the ride is likely to be bumpy and driven by news. If management can show even small improvements in execution, any activist involvement would probably add fuel rather than be the main reason to own shares. This looks more like a slow climb with sharp moves on headlines rather than a quick win.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)