/PayPal%20Holdings%20Inc%20sign%20on%20building-%20by%20Sundry%20Photography%20via%20Shutterstock.jpg)

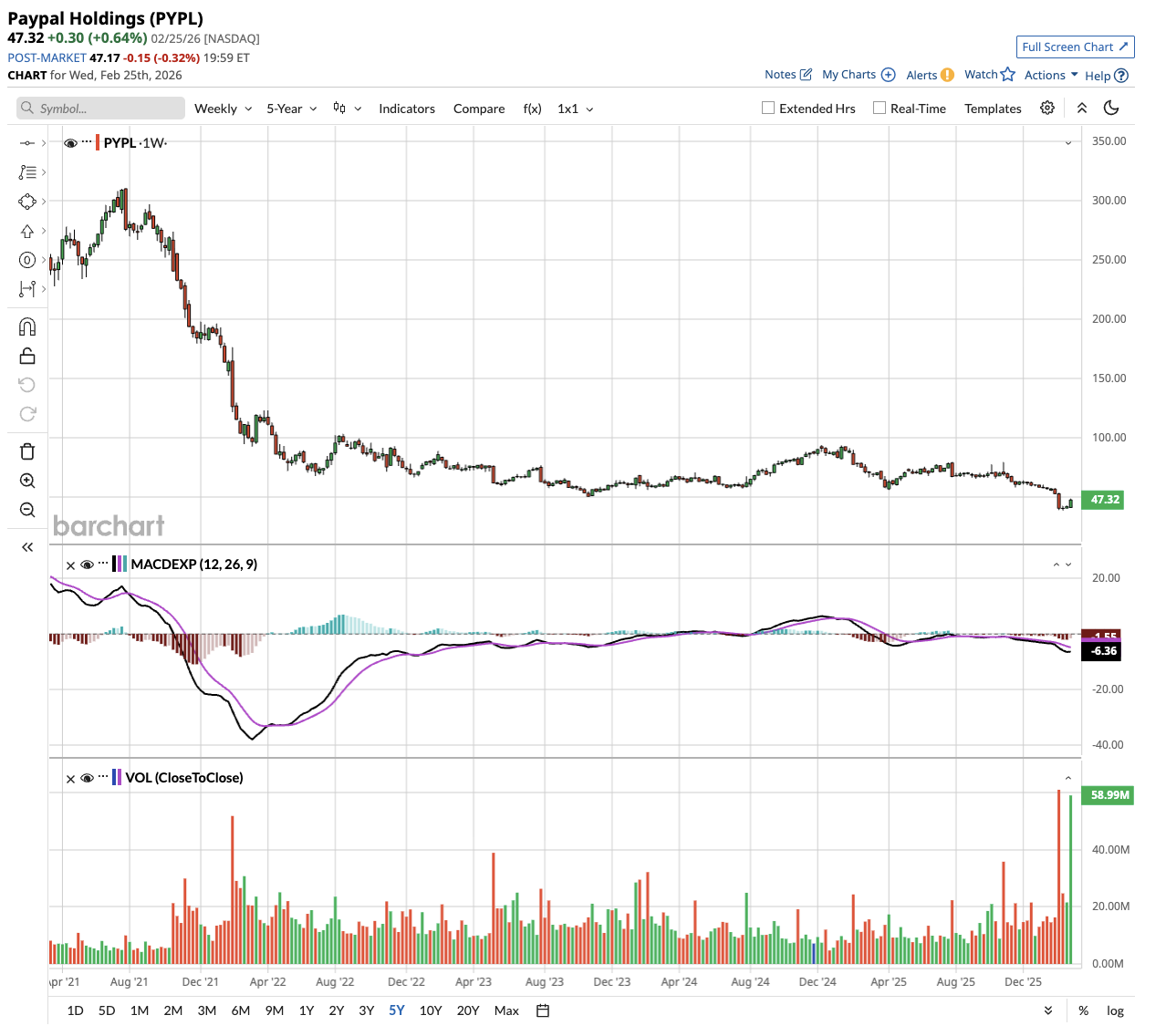

PayPal (PYPL) can't seem to catch a break in 2026. The stock has already dropped 21% year-to-date (YTD), following a rough 2025 in which shares lost nearly a third of their value. Then came a CEO shakeup, a disappointing profit forecast, and now a report that rival Stripe may be eyeing a buyout.

Investors are understandably asking: What do you do with PYPL stock right now?

Is PayPal Stock a Good Buy Right Now?

To understand the Stripe news, you first need to understand why PayPal is in this position.

The core problem is its branded checkout business, which grew just 1% in Q4 of 2025, down from 5% in the previous quarter.

Three things drove that slowdown:

- First, U.S. retail spending weakened, especially among lower- and middle-income consumers squeezed by higher cost of living expenses.

- Second, growth in Germany, one of PayPal's largest international markets, pulled back amid economic softness and rising competition.

- Third, high-growth categories such as travel, ticketing, and crypto all decelerated after strong runs.

On top of macro pressures, PayPal's execution also fell short. The company was too slow to upgrade merchant integrations and to deploy the latest checkout experience at scale.

It was also rolling out new checkout features without simultaneously enabling biometric authentication, which, when combined, can lift conversion rates by two to five percentage points.

Full-year 2025 revenue came in at $33.2 billion, up just 4%. Adjusted earnings per share grew 14% to $5.31, but the holiday quarter missed analyst expectations. Revenue of $8.68 billion fell short of the $8.80 billion Wall Street had forecast, according to data compiled by LSEG.

For 2026, PayPal guided adjusted profit to range from a low-single-digit decline to a slight increase. Analysts had been expecting roughly 8% growth, according to LSEG. The company also walked away from the specific 2027 targets it had set at its investor day just one year prior.

New CEO, Stripe Rumors, and More

The CEO change added another layer of uncertainty.

PayPal's board replaced outgoing CEO Alex Chriss with Enrique Lores, formerly of HP (HPE), effective March 1. The board said execution under Chriss "was not in line with its expectations." Chief Financial Officer Jamie Miller is serving as interim CEO during the transition.

Wall Street reacted cautiously. Analysts at Evercore ISI flagged the key question: Will Lores attempt another multi-year turnaround or explore strategic options for some of the company's assets?

That question got a lot more interesting fast.

Bloomberg reported that Stripe, the private fintech giant, is weighing a bid for all or part of PayPal, according to people familiar with the matter. The report sent PayPal shares up nearly 20% over the last two trading sessions. Valued at $159 billion, Stripe is on track to hit $1 billion in annual run rate for Services beyond payments.

PayPal and Stripe declined to comment on the report. The discussions are said to be in early stages, and nothing is confirmed.

PYPL Stock: Buy, Sell, or Hold?

There are genuine reasons to be cautious here.

Branded checkout, which still accounts for more than half of PayPal's profit, is struggling. The 2027 outlook has been shelved. A new CEO is coming in, and meaningful improvement in branding will take time to materialize.

But there are also bright spots.

- Venmo revenue hit $1.7 billion in 2025, growing roughly 20% year-over-year (YoY), and is on track to surpass $2 billion ahead of schedule.

- The Enterprise Payments business returned to double-digit volume growth in the fourth quarter. Buy Now, Pay Later (BNPL) topped $40 billion in total payment volume, growing more than 20%.

- And PayPal has also applied to form PayPal Bank, a move that could unlock small business lending and interest-bearing savings accounts.

A Stripe acquisition, if it materialized, could represent a significant premium to current prices. But it's early-stage speculation, not a deal.

Analysts tracking PayPal forecast revenue to increase from $33 billion in 2025 to $46.5 billion in 2030. Comparatively, free cash flow is forecast to expand from $6.41 billion to $11.84 billion in this period. If PayPal stock is priced at 10x forward FCF, which is below its 10-year average of 23x, it could more than double over the next three years.

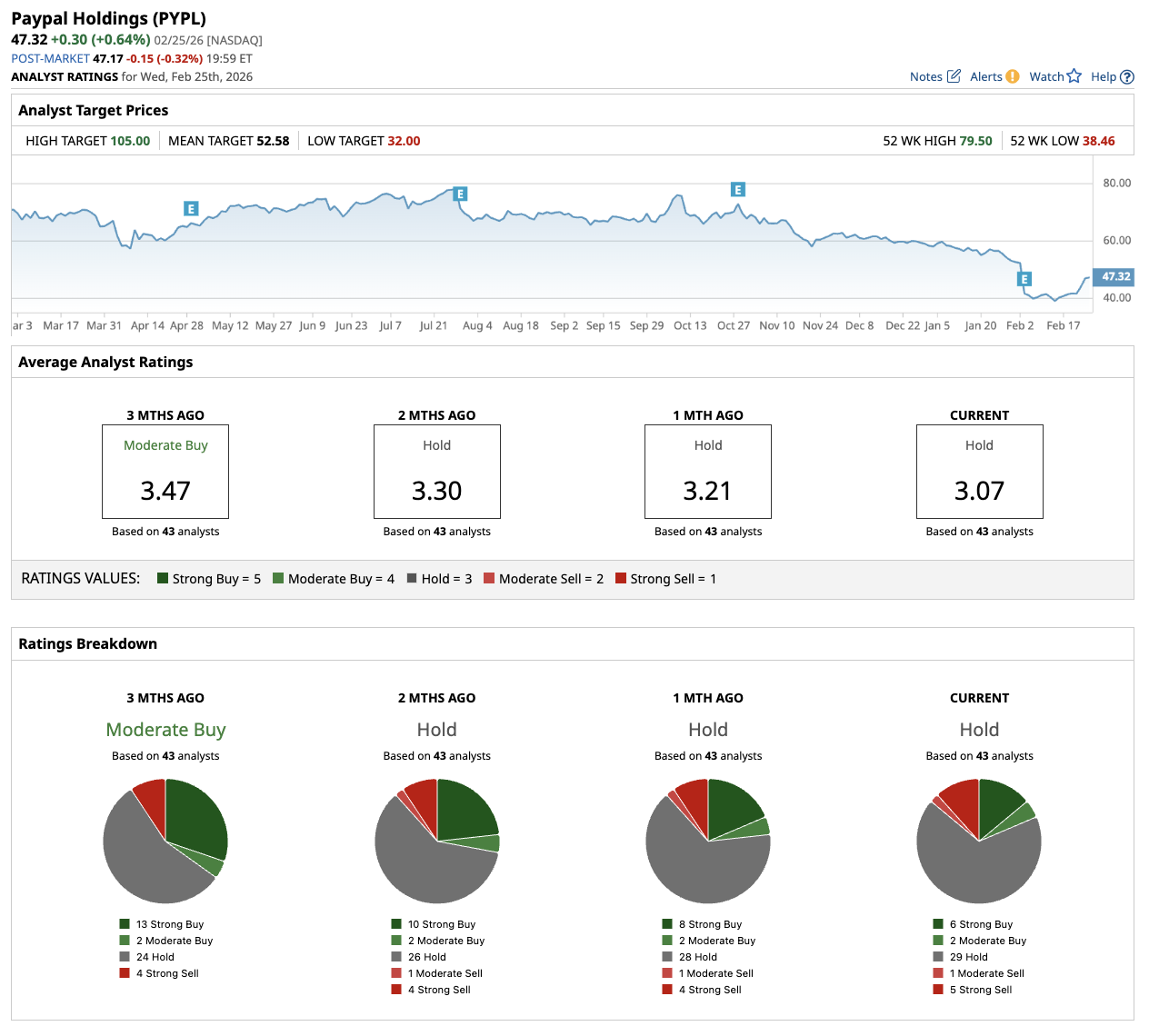

What Analysts Are Saying About PYPL Stock

Out of the 43 analysts covering PYPL stock, six recommend “Strong Buy,” two recommend “Moderate Buy,” 29 recommend “Hold,” one recommends “Moderate Sell,” and five recommend “Strong Sell.” The average PayPal stock price target is $52.58 above the current price of about $47.

For long-term investors, PYPL stock looks more like a hold or a cautious buy on weakness than a sell. The business still processes $1.8 trillion in annual payment volume. The brand still carries real weight. But patience will be required.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Robot%20arm%20industrial%20automation%20manufacturing%20by%20Eakrin%20via%20Adobe%20Stock.jpeg)