/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOG) (GOOGL) will report its first-quarter results on April 29, amid solid operating momentum but rising cost pressures. The tech giant’s core businesses, including Search and YouTube, continue to deliver steady growth, driven by higher engagement. At the same time, the cloud segment is witnessing solid artificial intelligence (AI)-driven demand.

Overall, Alphabet’s dominance in digital advertising and growing share in enterprise cloud services are likely to drive its top line. However, its increased investments in AI will likely hurt margins.

Alphabet’s accelerating investment cycle, focused on AI capabilities and supporting infrastructure, is likely to materially impact profitability. Capital expenditures are projected to climb sharply in 2026 to a range of $175 billion to $185 billion, up from $91.4 billion in 2025. Moreover, spending is expected to ramp up as the year progresses.

While AI investments are necessary to strengthen Alphabet’s competitive positioning, they will compress margins and hurt free cash flow in the near term.

Alphabet Q1 Preview: Balancing Strong Growth With Rising AI Costs

Alphabet’s Q1 financials will reflect the ongoing strength in its core businesses. The Google Services segment, including Search, YouTube, and subscription products, could continue to report steady growth despite seasonal softness in advertising.

Search is benefitting from higher engagement, improving monetization, and the integration of AI-enhanced features that refine query relevance and advertising efficiency. These improvements strengthen Google Search’s competitive positioning while sustaining pricing power in a performance-driven advertising environment.

YouTube advertising is also expected to support its growth. The platform’s scale and engagement continue to attract performance marketing budgets, even amid broader macro uncertainty.

Supporting the company’s growth is the solid momentum in Google Cloud. The segment has been expanding rapidly, supported by enterprise adoption of AI-centric solutions. Demand remains robust despite capacity constraints.

Google Cloud Platform (GCP) is gaining traction, and a substantial portion of Google Cloud customers now leverage its integrated AI stack, which spans proprietary hardware, foundational models, and enterprise tools. This integration enhances customer value and drives higher product adoption rates, effectively increasing revenue per client.

Notably, in Q4, cloud revenue surged 48%, reaching an annualized run rate above $70 billion. The backlog also expanded significantly, rising 55% quarter-over-quarter to $240 billion, reflecting strong demand for AI-driven solutions across a broad customer base.

Google is also securing larger deals, with the number of contracts exceeding $1 billion in 2025, rising significantly. At the same time, it is strengthening relationships with existing customers, with 75% of them using its vertically integrated AI stack. These customers adopt significantly more products, which helps diversify revenue streams and accelerate growth.

Google now benefits from multiple monetization avenues across its product portfolio, including infrastructure, platform services, and high-margin AI-powered offerings. Notably, it has 14 distinct product lines generating over $1 billion in annual revenue.

Despite these favorable top-line dynamics, profitability is likely to face near-term pressure. Elevated capital expenditures tied to AI infrastructure are expected to weigh on margins in the quarter. Consensus estimates point to a year-over-year decline in earnings per share (EPS).

Analysts estimate EPS of $2.63, down 6.4% from the previous year. Even so, Alphabet has consistently outperformed expectations, beating analyst estimates in each of the past four quarters.

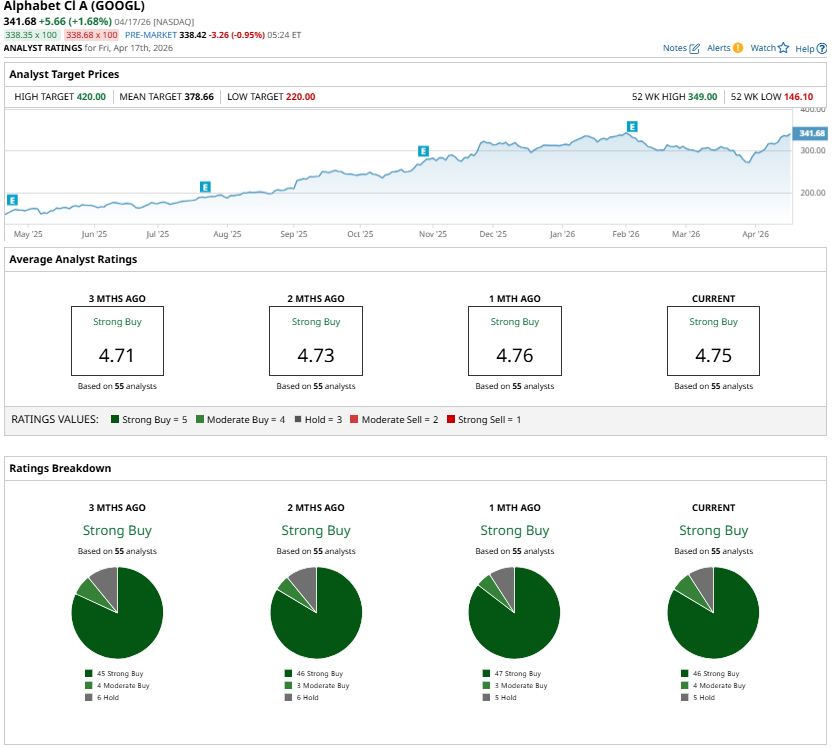

Is GOOGL Stock a Buy, Sell, or Hold Ahead of Q1 Earnings?

From an investment perspective, Alphabet’s fundamentals remain intact. Its dominance in digital advertising, combined with accelerating momentum in cloud and AI, provides a strong foundation for long-term growth.

However, the scale and pace of its AI-related investments are likely to act as a near-term overhang on the stock. Margin compression and reduced free cash flow could limit upside in the short run, particularly in an environment where investors are increasingly sensitive to capital efficiency.

Despite these concerns, market sentiment remains broadly positive, with analysts maintaining a favorable outlook, in the form of a “Strong Buy” consensus, on the stock heading into earnings.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)