/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

SoFi (SOFI) stock has experienced significant volatility in recent months. Shares of the financial technology company have declined 40.7% from the 52-week high, due to its high valuation and concerns about equity dilution following recent capital raises. These concerns have been compounded by persistent geopolitical tensions and an uncertain economic backdrop.

Despite this backdrop, sentiment around SoFi stock has shifted ahead of its first-quarter earnings release on April 29. The stock has rebounded 18.5% over the past week, suggesting renewed investor confidence.

Fundamentally, SoFi continues to perform well. Its platform is acquiring new members at a robust pace, while simultaneously deepening engagement with its existing customer base. Cross-selling remains a key driver as users adopt multiple financial products, thereby enhancing lifetime value and diversifying revenue streams. These dynamics have contributed to solid top line expansion and improved unit economics.

This momentum in SoFi’s business will likely sustain in Q1, with the company expected to deliver solid top and bottom line growth.

SoFi to Sustain Solid Momentum in Q1

SoFi enters the first quarter of 2026 with strong operating momentum, supported by broad-based growth across its core business segments. The company closed 2025 on a high note, reporting adjusted net revenue of $ 1.1 billion in the fourth quarter, a 37% year-over-year (YOY) increase. A significant portion of this growth was driven by its Financial Services and Technology Platform divisions, which together generated $579 million in revenue, up 61% YOY, and accounted for more than half of total revenue.

Management has guided for adjusted net revenue of $1.04 billion, implying YOY growth of around 35%. This anticipated growth reflects sustained traction in both member acquisition and product adoption, which remain key drivers of the company’s top line growth.

Also, SoFi is benefitting from deeper engagement with its existing customer base. The company is seeing increasing cross-product adoption, with members adding multiple financial services over time. This dynamic is strategically significant. It enhances customer lifetime value while reducing acquisition costs, effectively improving unit economics as the platform scales.

Revenue diversification is another important factor supporting SoFi’s growth. The financial technology company continues to shift toward fee-based income streams, which are generally more stable and less capital-intensive than lending. Strength in the Loan Platform Business, alongside contributions from referral fees, interchange revenue, and brokerage services, is expected to sustain this trend.

SoFi has scaled its fee-based revenue to an annualized run rate of nearly $1.8 billion, up significantly from less than $1.2 billion just over a year prior. This transition toward capital-light revenue reduces exposure to credit risk and interest-rate volatility, thereby improving overall business resilience.

SoFi’s balance sheet also remains solid. Growth in deposits is lowering SoFi’s cost of funding, thereby enhancing net interest margins and profitability. Combined with operating leverage from higher revenues and ongoing efficiency improvements, this creates a favorable backdrop for earnings expansion. Analysts project earnings of $0.12 per share for the quarter, implying its bottom line will double YOY.

Overall, SoFi is well-positioned to deliver strong growth in Q1, which could support its stock price.

The Bottom Line

While SoFi stock came under pressure due to valuation concerns and broader macro uncertainty, its business is performing exceptionally well, with top and bottom line growth at a solid pace. Heading into its Q1 earnings release, SoFi appears well-positioned to deliver robust financial results, supported by continued member growth, deeper product adoption, and a strengthening balance sheet.

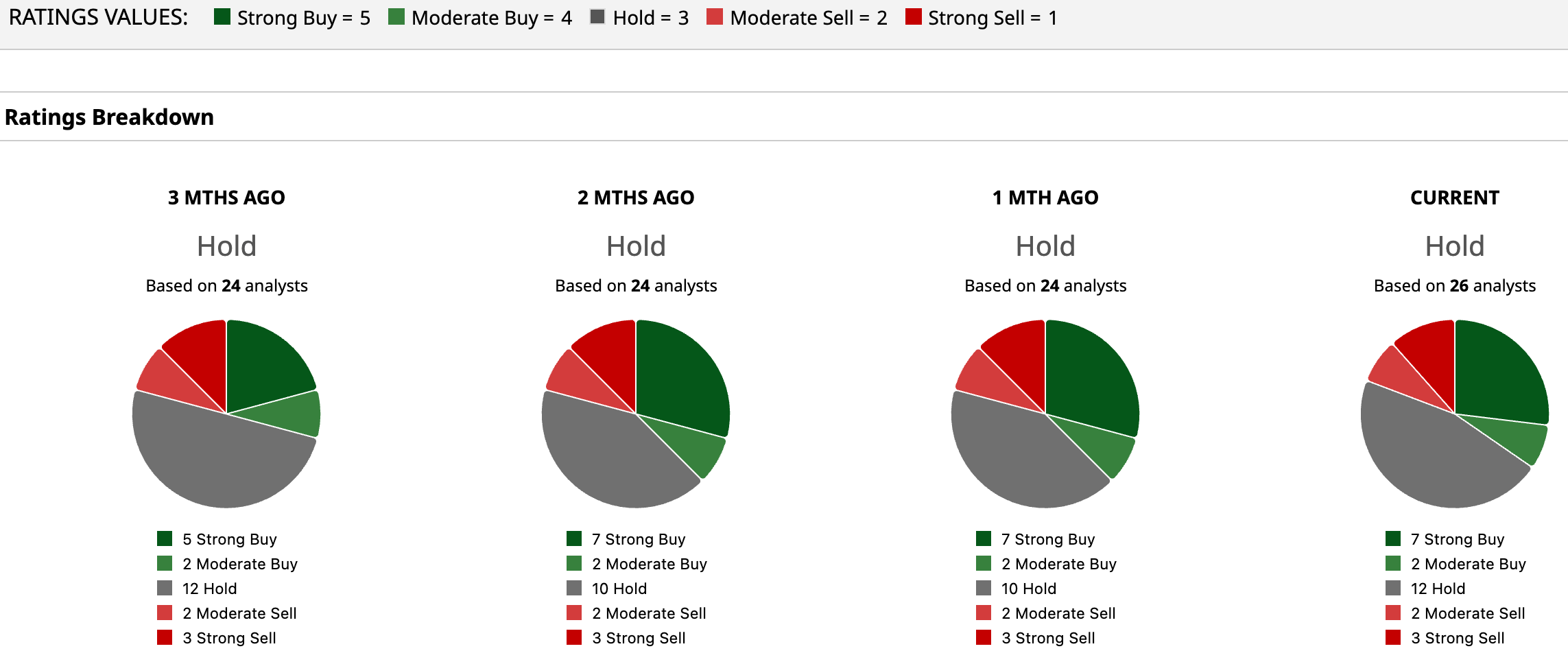

While analysts maintain a “Hold” consensus rating on SoFi stock, its strong growth trajectory, improving unit economics, and strategic shift toward more stable, fee-based revenue streams align well for growth.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)