The buy-now-pay-later (BNPL) company, Affirm Holdings (AFRM), is starting to dust itself off and find its footing after a bruising start to 2026. Morgan Stanley has come out swinging in its defense as analyst James Faucette named it the firm’s Top Pick, backed it with an “Overweight” rating, and set a $76 price target.

Faucette has hung his hat on three pillars. These include the potential for upward estimate revisions, private credit fears that Morgan Stanley explicitly views as overdone, and a strong near-term catalyst path that could keep momentum from slipping through the cracks.

Yet, AFRM stock stayed under pressure due to concerns tied to the private credit market. However, the underlying funding data turns that narrative on its head. The company’s latest securitization drew demand that comfortably outpaced supply at 6x oversubscribed, while average funding costs have moved down in a steady glide from 7% in Q3 FY 2025 to 6% in Q2 FY 2026.

This dynamic enhances Affirm's position because robust demand and lower finance costs allow it to fund more loans, scale operations faster, and maintain margins without losing ground. It also alleviates private credit concerns, as data demonstrates that investors continue to support the company when it matters most, and funding remains available.

Morgan Stanley believes the Affirm 2026 Investor Forum, scheduled for May 12, could act as a major catalyst, with the company likely to raise its Gross Merchandise Volume (GMV), margin, and EPS targets at the event. This hands investors a clear reason to keep AFRM shares on their radar right now.

About Affirm Stock

Affirm Holdings operates a fintech platform that powers its payment network through point-of-sale financing, merchant commerce tools, and a consumer app. It allows shoppers to break purchases into installments and brings merchants together with originating banks and capital markets partners so funding flows smoothly at checkout.

Since opening its doors in 2012, the San Francisco, California-based firm has grown into a business that now holds a market cap of $21.49 billion.

Its stock has taken investors on quite a ride as it surged 54.25% in the past 52 weeks, then hit a speed bump with a 12.75% drop in 2026, before turning on the afterburners again and skyrocketing 24.96% in just the past five trading sessions.

At current levels, AFRM stock is trading at 20.61 times forward adjusted earnings and 5.19 times sales, which places it well above industry benchmarks and shows investors have not been shy about paying a premium.

Affirm Surpasses Q2 Earnings

Despite a challenging macro environment, Affirm maintained its performance when it released its fiscal Q2 fiscal year 2026 results on Feb. 5. Revenue increased 29.6% year-over-year (YOY) to $1.12 billion, exceeding analyst projections of $1.06 billion. EPS grew 60.9% from the year-ago value to $0.37, clearing the Street’s estimate of $0.27.

GMV reached $13.8 billion, marking a 36% YOY increase. The active consumer base expanded to 25.8 million, up 23% from the prior year, and users leaned in further as transactions per active consumer climbed 20% to 6.4.

With total transactions increasing 44% YOY to 54.9 million, transaction momentum likewise maintained its vigor. Repeat customers accounted for 96% of that activity, or 52.5 million transactions, which shows that once users step in, they tend to stick around.

The Affirm Card business turned into a clear standout, with Card GMV surging 159% YOY to $2.19 billion. The active consumer base for the card jumped 121% to 3.7 million users, while the attach rate stood at 14% across the broader platform, which signals that the company is spreading its wings beyond its traditional BNPL model.

The balance sheet adds another layer of comfort, as the company ended the quarter with approximately $2.3 billion in total liquidity across cash and equivalents plus securities available for sale, set against approximately $1.1 billion in convertible debt.

Looking ahead, management expects Q3 fiscal year 2026 revenue to land between $970 million and $1 billion for the quarter, while full fiscal year 2026 revenue is projected to come in between $4.086 billion and $4.146 billion.

On the other hand, analysts expect Q3 fiscal year 2026 EPS to surge 1,600% YOY to $0.17. For the full fiscal 2026 year, they forecast EPS to rise 626.7% to $1.09, followed by a further 57.8% increase to $1.72 in fiscal 2027.

What Do Analysts Expect for Affirm Stock?

Citizens Financial Group analyst David M. Scharf has kept a “Market Outperform” rating on AFRM stock and set an $85 price target, even after bringing it down from $105. Whereas Cantor Fitzgerald analyst Ramsey El-Assal reiterated an “Overweight” rating and left the price target unchanged at $85.

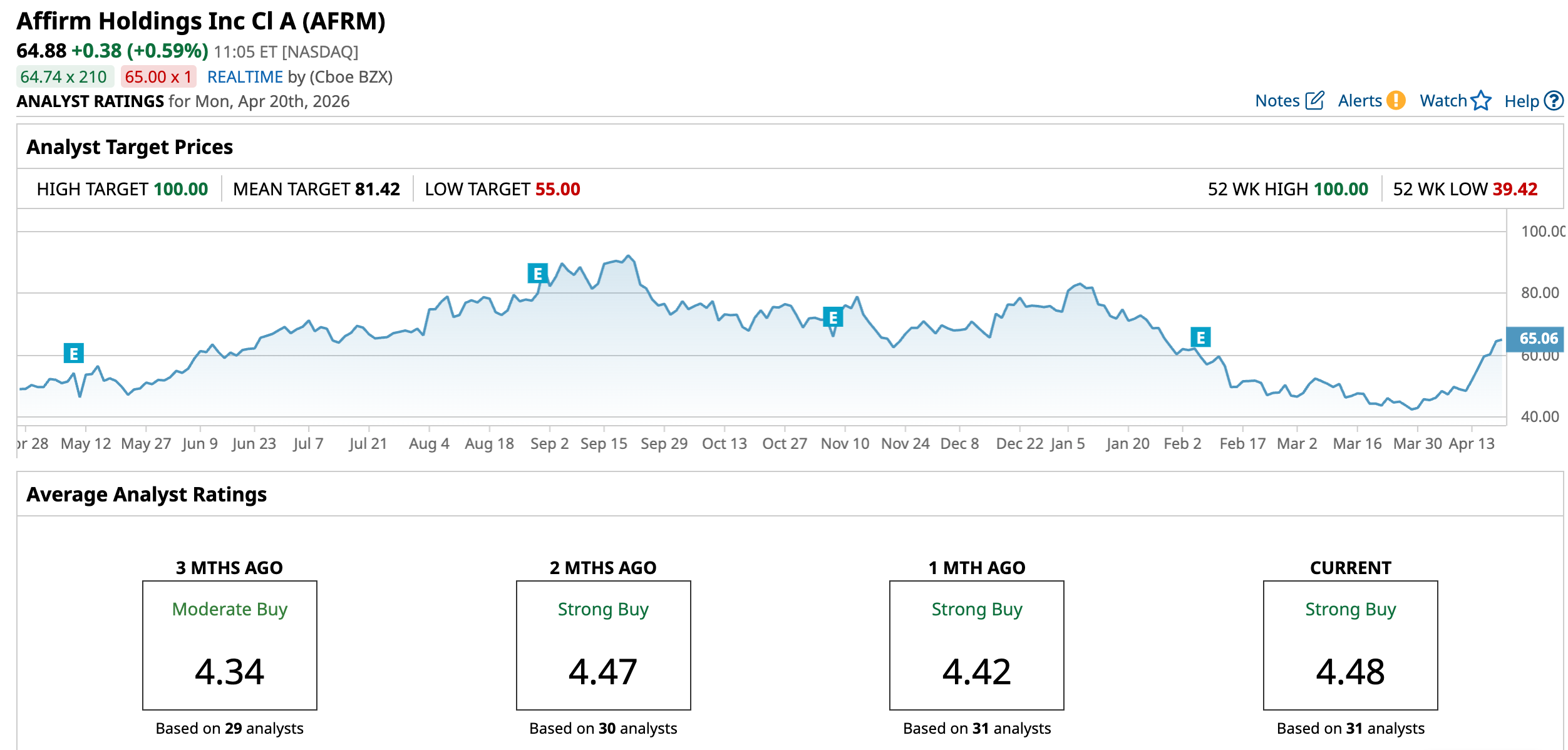

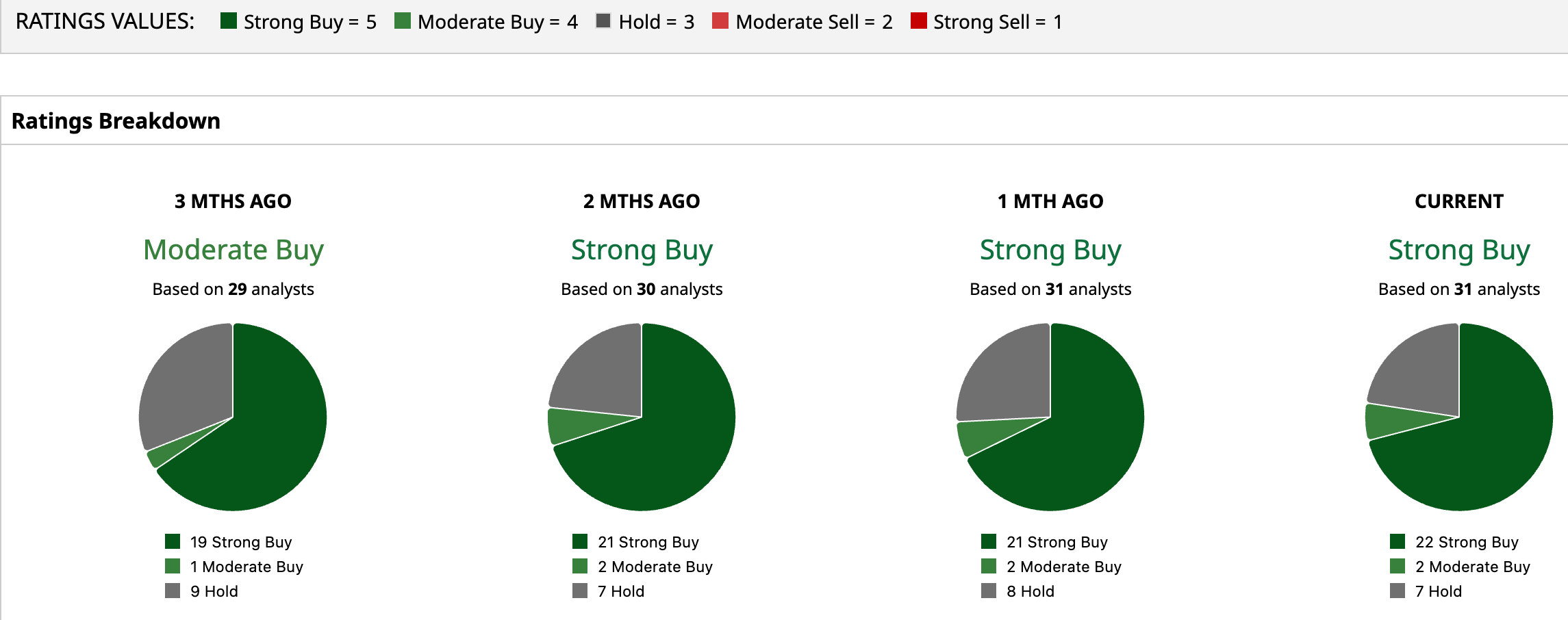

Wall Street has backed the stock with an overall rating of “Strong Buy.” Among 31 analysts covering the stock, 22 have issued “Strong Buy” ratings, two have gone with “Moderate Buy,” and seven have stayed with “Hold” calls.

AFRM stock carries an average price target of $81.42, which signals potential upside of 25.5%. Meanwhile, the Street-High target of $100 points to a gain of 54% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)