/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

The kind of rally SanDisk (SNDK) has delivered over the past year is often what investors associate with early-stage disruptors, but never with a company rooted in decades-old semiconductor technology. Yet here it is, a stock up a staggering 2,817% in just twelve months, but it is still not as hyped as Nvidia (NVDA). This performance was fueled by a powerful mix of artificial intelligence (AI) demand, tightening supply dynamics, and a fundamental shift in how the NAND memory industry operates. SNDK stock is up 284% so far this year, outperforming most high-flying AI stocks and the overall market gain of 4%.

What’s even more striking is that analysts are arguing SanDisk’s story is still unfolding and has plenty of room to run.

AI Is the Catalyst Behind Explosive Demand

Valued at $135.7 billion, SanDisk is a semiconductor company that designs and manufactures NAND flash memory and storage solutions used to store and access data. It’s no surprise AI is the powerful force behind SanDisk’s surge. Its enterprise SSD business, which serves data centers, is seeing rapid growth as AI infrastructure expands globally. In fact, the company reported a 64% sequential increase in data center revenue in the second quarter of fiscal 2026. Total revenue surged 61% year-over-year (YoY) to $3 billion, with an astonishing increase of 408% in earnings per share (EPS) to $6.20.

While data centers are currently the primary growth engine, other segments are also contributing meaningfully. In the edge market, which includes PCs, smartphones, and other devices, AI-driven upgrade cycles are boosting storage requirements per device. Meanwhile, consumers are increasingly turning to premium products such as high-performance SSDs and creative storage solutions. While demand is surging, supply is struggling to keep up. SanDisk expects this imbalance to persist into 2026. The company is prioritizing partners willing to engage in long-term supply agreements, which provide greater visibility and stability.

Why Wall Street Thinks the Rally Isn’t Over

SanDisk’s story is no longer just a story of momentum. It is increasingly being backed by Wall Street confidence in its long-term prospects. Recently, Evercore ISI initiated coverage with an “Outperform” rating and a $1,200 price target while citing a possible bull case of up to $2,600 per share. The firm points to SanDisk’s deep exposure to one of the most critical layers of the AI infrastructure stack, data storage, where demand is rapidly accelerating even as supply is expected to remain tight for years.

Jefferies has also turned more bullish on SanDisk, raising its price target to $1,000 while maintaining a “Buy” rating. The firm highlights upcoming catalysts, including the rollout of advanced quad-level cell SSDs to major data center customers, which could further strengthen SanDisk’s position and drive additional growth. Given its meteoric rise in the past year, one would expect analysts to be cautious. Instead, many analysts see further upside because of various factors. First, the AI-driven demand cycle is still in its early stages. As more firms adopt AI at scale, the demand for high-performance storage will grow.

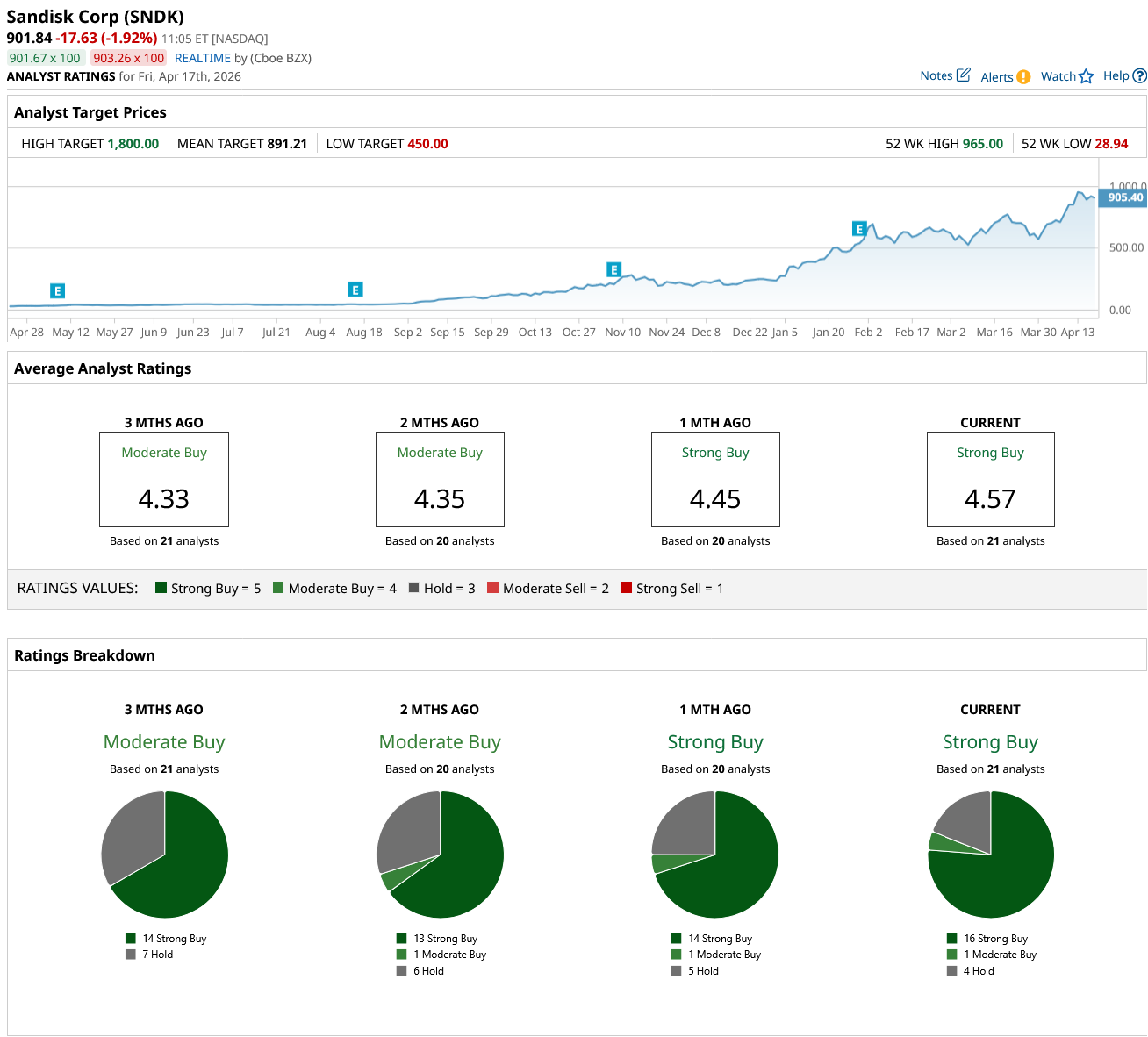

Second, the NAND industry is becoming more disciplined with more focus on profitability rather than blind aggressive expansion. Third, multi-year supply agreements are leading to more stable and predictable earnings. SanDisk’s positioning at the center of AI infrastructure, consumer devices, and enterprise storage gives it multiple avenues for growth. These are the possible reasons why analysts believe SNDK's climb will continue in the next months. The stock has already surpassed its average price target of $891.21. The Street-high estimate of $1,800 indicates Wall Street anticipates potential upside of around 96% over the next 12 months.

SNDK Stock: What Analysts Are Saying, and Investors Should Watch For

Overall, analysts believe SNDK stock is a consensus “Strong Buy.” Of the 21 analysts covering the stock, 16 recommend a “Strong Buy,” one rates it as a “Moderate Buy,” and four suggest holding. Despite the optimism, risks remain. The semiconductor industry has a long history of boom-and-bust cycles, which could create stock volatility. Furthermore, maintaining high margins while scaling production and navigating complex customer relationships requires disciplined management.

Investors should keep an eye on these factors when SanDisk reports its third quarter of fiscal 2026 earnings on April 30. Analysts expect revenue to increase by 176.5% to $4.7 billion in Q3. SanDisk’s earnings could increase to $14.27 per share compared to a loss of $0.30 per share in the year-ago quarter. For the full fiscal year 2026, earnings are expected to increase by 1,339.7% to $43 per share, followed by 148.9% to $107.1 per share. Despite this staggering expected growth, SNDK stock is trading cheap at eight times forward earnings. If the stock hits the “bull case” of $2600, it would mean a whopping 182.7% upside potential. Looking at SanDisk’s earnings projections for the next two years, the target appears to be within reach.

The Key Takeaway

SanDisk’s extraordinary stock performance is rooted in its transformation and the industry it operates in. AI-driven demand, supply discipline, and evolving business models have created a powerful growth engine. If these trends continue, SanDisk may not just be a short-term winner. Instead, it could emerge as one of the significant semiconductor success stories of the AI era.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)