The ceasefire between the U.S. and Iran is on shaky ground, raising concerns about shipping through the key Strait of Hormuz. As peace talks between the two nations collapsed, President Donald Trump threatened to blockade the Strait, prompting aluminum prices to climb to a four-year high on April 13.

That’s because the Middle East accounts for approximately 9% of global aluminum output, making the Strait of Hormuz extremely important for metal exports, with key producers in Saudi Arabia, the United Arab Emirates and Bahrain.

In fact, the blockade of the sea route is not the only concern these producers face. Emirates Global Aluminium, the Middle East’s top producer, invoked a force majeure on some contracts that allows it to miss contracted deliveries without penalty as the Al Taweelah production plant sustained heavy damage in an Iranian strike. Another top producer, Bahrain’s Alba, also cut production last month after it was unable to ship metals through the Strait of Hormuz.

The Trump administration recently enacted a naval blockade on Iranian ports, with the U.S. Central Command announcing that it has been “fully implemented.” Against this backdrop, should you consider investing in U.S.-based aluminum producer Alcoa (AA) now?

About Alcoa Stock

Based in Pittsburgh, Pennsylvania, Alcoa stands as a major vertically integrated aluminum producer. It extracts bauxite ore, processes it into alumina, and then smelts it into primary aluminum for global industries. The firm manages plants dedicated to these key steps, delivering materials to sectors such as automotive, aerospace, packaging, and building.

Through its alumina and aluminum divisions, Alcoa converts natural resources into vital metals, prioritizing streamlined manufacturing across its global sites. Alcoa has a market capitalization of $18.6 billion.

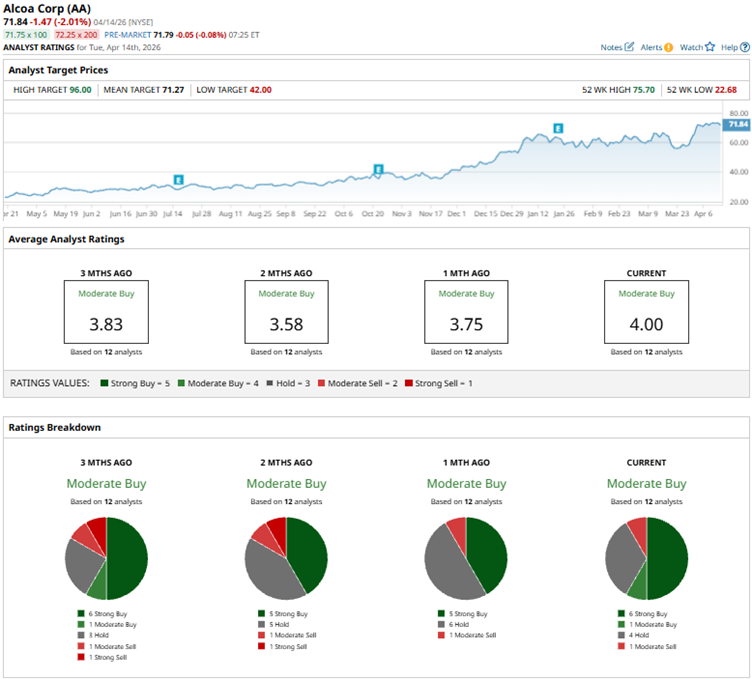

The disruptions due to the Iran war have cut global aluminum supply, spiking prices and benefiting Alcoa's upstream model, which integrates bauxite and alumina production. Over the past 52 weeks, AA stock has gained 186%, while shares are up 35% year-to-date (YTD). AA stock reached a 52-week high of $75.70 on April 9, but after declining 2% over the past five days, shares are down 13% from that level.

Alcoa stock is trading at a cheaper valuation compared to its peers. Its forward price-to-earnings (P/E) ratio of 9.5 times is lower compared to the industry average.

Alcoa Delivered a Solid 2025 Performance Amid Supply Challenges

Last year, Alcoa’s aluminum production increased 5% year-over-year (YOY) as the company restarted capacity at the Alumar (Brazil), San Ciprián (Spain), and Lista (Norway) smelters. Annual revenue increased 8% YOY to $12.83 billion. However, there were supply challenges, as its aluminum total shipments declined 3% annually. Meanwhiile, full-year adjusted EPS grew from $1.35 in 2024 to $3.77 in 2025.

Wall Street analysts have a mixed outlook on Alcoa’s future earnings. For the current fiscal year, EPS is projected to surge 101% annually to $7.57, followed by a roughly 3% decline to $7.37 in the next fiscal year. Analysts also expect the company’s EPS to drop 26% YOY to $1.60 for the first quarter of 2026.

Here’s What Analysts Think About Alcoa Stock

This month, analysts have given neutral to positive views on AA stock. While mixed sentiment persists, analysts have raised their price targets on the stock. On April 9, JPMorgan analysts maintained a “Neutral” rating on Alcoa but raised the price target from $68 to $70. BMO Capital analyst Katja Jancic also raised the price target from $65 to $75 but kept the rating at “Market Perform.”

However, on the same day, Morgan Stanley analysts upgraded their rating from “Equal Weight” to “Overweight” and raised the price target from $64 to $80. As the global supply of aluminum remains constrained, analyst Carlos De Alba believes the tight physical market reinforces upside in aluminum prices and regional premiums, although softer demand might offset some of that. De Alba also projected Alcoa’s realized pricing in the aluminum segment higher by 13% in 2026 and more than 20% in 2027, which spells upside for the company’s EBITDA and EPS over the same period.

Wall Street analysts are moderately bullish on AA stock, with a consensus “Moderate Buy” rating. Of the 12 analysts rating the stock, six analysts have a “Strong Buy” rating, one analyst suggests a “Moderate Buy,” four analysts offer a “Hold” rating, and one analyst has a “Moderate Sell” rating. The consensus price target of $71.27 is roughly flat from current levels. However, the Street-high price target of $96 represents 36% potential upside from here.

The Key Takeaway

As a U.S.-based upstream producer with integrated bauxite mining, alumina refining, and smelting, Alcoa avoids heavy reliance on disrupted Gulf routes or Middle Eastern raw materials. This positions it to ramp up stable output from its facilities amid global shortages. Moreover, the company has bolstered its key operations through better control following the 2024 acquisition of Alumina Limited. Elysis, its joint venture with Rio Tinto (RIO), also hit a major milestone last year by deploying an industrial-scale, carbon-free anode in an existing smelter, thereby advancing decarbonization.

Given its market position, Alcoa may be well-equipped to capitalize on current geopolitical dynamics and realize higher spot aluminum prices.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Sign%20of%20Intel%20at%20entrance%20%20by%20michaelmond.jpeg)