/Drone%20flying%20by%20Pexels%20via%20Pixabay.jpg)

Analysts at Jefferies are bullish on Kratos Defense & Security Solutions (KTOS), noting that the stock could climb as much as 26% from current levels. All thanks to a key catalyst – the anticipated production ramp-up of the Valkyrie drone program. In fact, analyst Sheila Kahyaoglu upgraded the stock to a “Buy” rating due to strong growth across key segments, which includes the ramp in production.

Also, it includes a potential 31% compound annual growth in Government Solutions through 2028, driven by hypersonic program demand, which includes its Prometheus joint venture. The upgrade is tied to missile propulsion and the anticipated production ramp-up of the Valkyrie drone program. Even more exciting, the Valkyrie program is expected to transition into higher-rate production, which is critical because it could lead to more predictable revenue streams. All of this would support Jefferies’ bullish outlook.

Kratos’ Valkyrie Advantage

Kratots’ XQ-58A Valkyrie is a low-cost, high-performance unmanned combat aerial vehicle (UCAV). Operating alongside manned fighter jets, such as the F-35, F-22, F-15EXs, and F-18s, the Valkyrie fits into the U.S. military’s evolving strategy of deploying “loyal wingman” drones. As noted in an XQ-58A fact sheet, “The XQ-58A delivers a combination of long-range, high-speed, and maneuverability along with the capability to deliver a mix of lethal weapons from its internal bomb bay and wing stations.”

Fueling upside, KTOS is considered a leader in “affordable mass” because it builds high-quality autonomous systems that cost a fraction of other vehicles' cost. It’s part of the reason it currently works with the U.S. Department of Defense and branches of the U.S. military. It could secure even more contracts as the Pentagon shifts toward more drone-centric systems. In addition, after years of development and testing, the Valkyrie program is expected to transition into higher-rate production, which is critical because it could lead to more predictable revenue streams. All of which supports Jefferies’ bullish outlook.

Recent Bill Could Boost Kratos

In addition, we have to remember that drones are quickly becoming an essential tool for the U.S. government. Not long ago, President Trump recently unveiled the “One Big Beautiful Bill”, which outlined how the U.S. would deliver “massive amounts of inexpensive, American-made, lethal drones to U.S. military units to amplify their combat capabilities,” as noted by Army.mil. Also, U.S. Secretary of Defense Pete Hegseth’s policy directive, Unleashing U.S. Military Drone Dominance, followed that with a plan to approve “hundreds of American products for purchase by the department, powering a ‘technological leapfrog’ by arming combat units with the very best of low-cost American-made drones, and finally, training as the department expects to fight,” according to the publication.

Earnings Have Been Solid

Earnings have been just as impressive. In its fourth quarter, KTOS' EPS of $0.18 beat estimates by $0.13. Revenue of $345.1 million, up about 22% year-over-year (YOY), beat by $17.64 million. And, according to Kratos’ President and CEO Eric DeMarco, as quoted in an earnings release:

“We finished 2025 exceeding our financial objectives for the fourth quarter, generating approximately 20 percent Q4 year-over-year organic Revenue growth, generating a 1.3 to 1.0 book to bill ratio on top of this 20 percent organic growth, having a record backlog of $1.573 billion, and a record opportunity pipeline of $13.7 billion, with the opportunity set for Kratos having never been stronger and continuing to increase. Kratos is positioned to achieve our previously communicated 2026 and 2027 financial targets, and similar to 2025, for 2026 we expect our business to accelerate throughout the year, with increasing Revenue volume and adjusted EBITDA margins, as several new programs, contracts, and initiatives begin, ramp, and expand.”

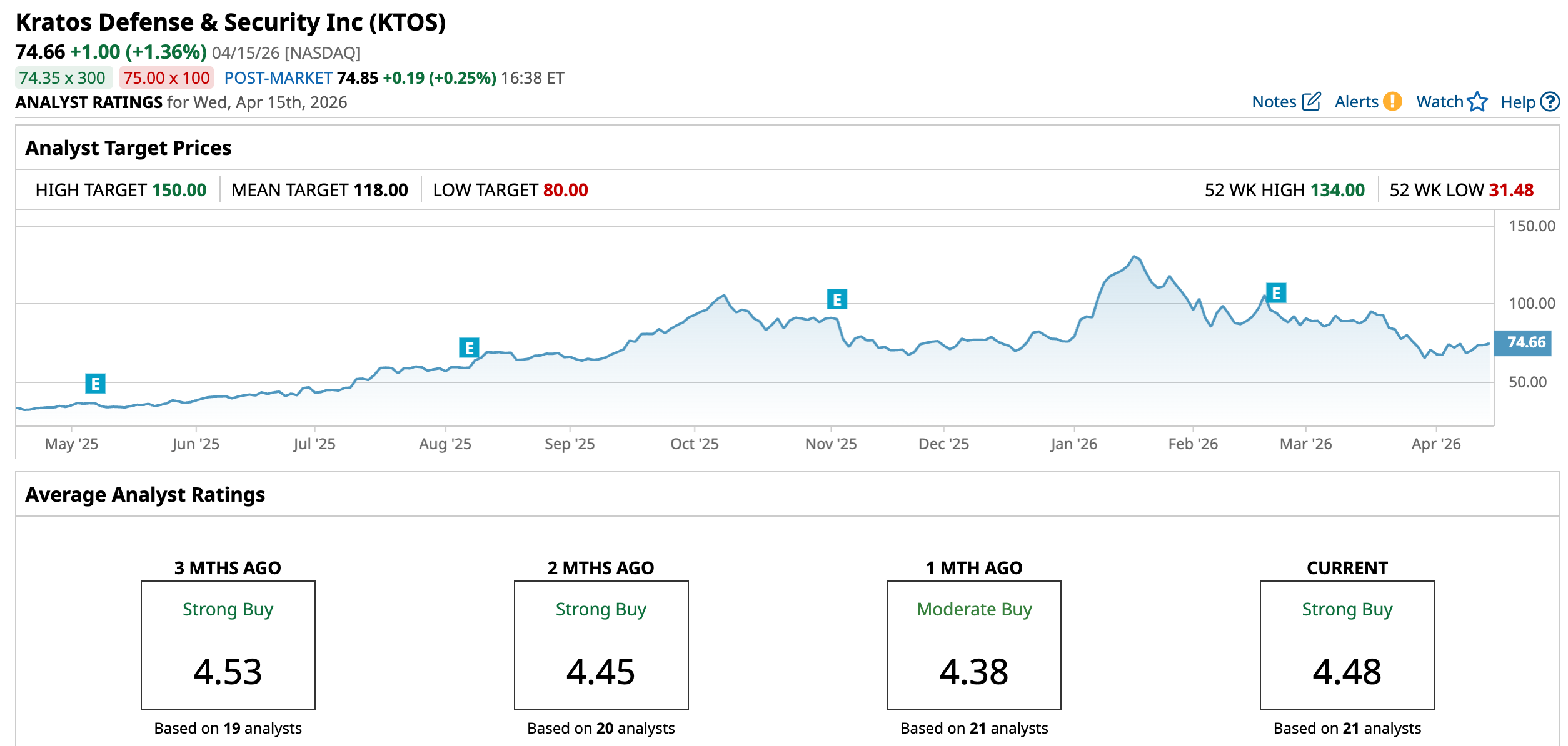

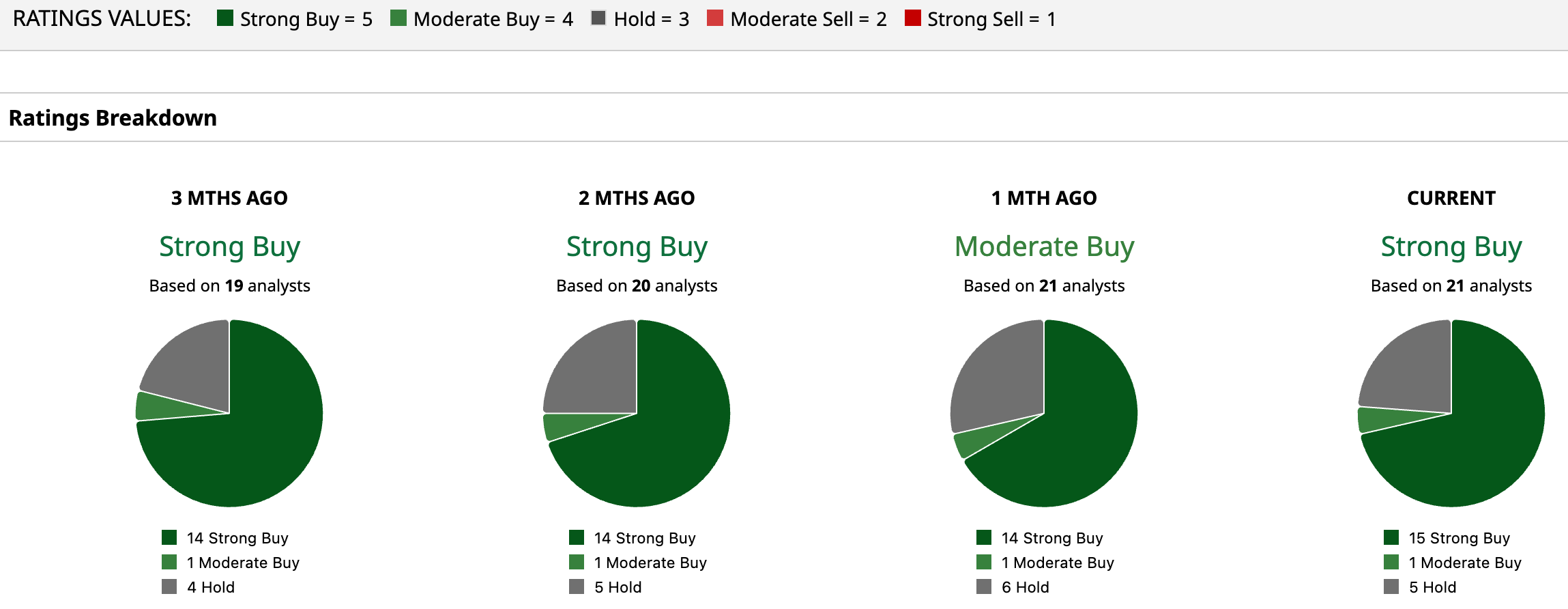

What Do Analysts Say About KTOS Stock?

Of the 21 analysts covering the KTOS stock, 15 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and five have a “Hold” rating. The mean target price of $118 implies 58% potential upside from current levels. Meanwhile, the high-end target of $150 implies as much as 101% possible growth from here. Kratos Defense & Security Solutions appears to be at a pivotal moment, with multiple catalysts supporting substantial upside and analyst bullishness. Add in favorable policy tailwinds and growing Pentagon emphasis on cost-effective, autonomous systems, and Kratos’ strategic relevance becomes even stronger for long-term investors.

On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)