/McDonald's%20Corp%20location%20by-%20M_Suhail%20via%20iStock.jpg)

In 2026, the beverage game is no longer just about a regular cola on the side. Consumers, especially younger ones, are chasing variety, energy boosts, and even a bit of personalization in what they drink. Energy drinks and dirty sodas have quietly become their own “occasion,” not just an add-on. Naturally, restaurant chains are adapting fast. For instance, Yum! Brands (YUM) has already pushed similar offerings through Taco Bell, signaling a broader industry shift.

Now, McDonald’s Corporation (MCD) is stepping into the ring. Known for its classic burgers and fries, the company is expanding into this fast-growing beverage lane with a fresh lineup – like Red Bull Dragonberry Energizer, Dirty Dr Pepper, and Mango Pineapple Refresher. Specialty sodas are expected to hit menus as early as next month, with energy drinks rolling out from August, priced competitively to take on players like Starbucks (SBUX) and Dutch Bros (BROS).

The strategy is to capture attention, attract younger consumers, and drive higher order values – staying relevant in a crowded quick-service space. But is this just a stylish menu upgrade, or will this beverage push be enough to refresh MCD stock and turn it into a buy right now?

About McDonald’s Stock

Chicago-based McDonald’s Corporation, founded in 1940, has quietly turned into the world’s most familiar fast-food name. Today, with more than 40,000 outlets across over 100 countries, it serves the same promise – quick, tasty, and reliable, whether it is burgers, fries, breakfast, or coffee.

With over 90% of its restaurants run by franchise partners, McDonald’s keeps things light while cash keeps flowing in. At the same time, it keeps evolving, adding digital ordering, delivery, and value meals to match changing tastes. It boasts a market capitalization of approximately $215.5 billion.

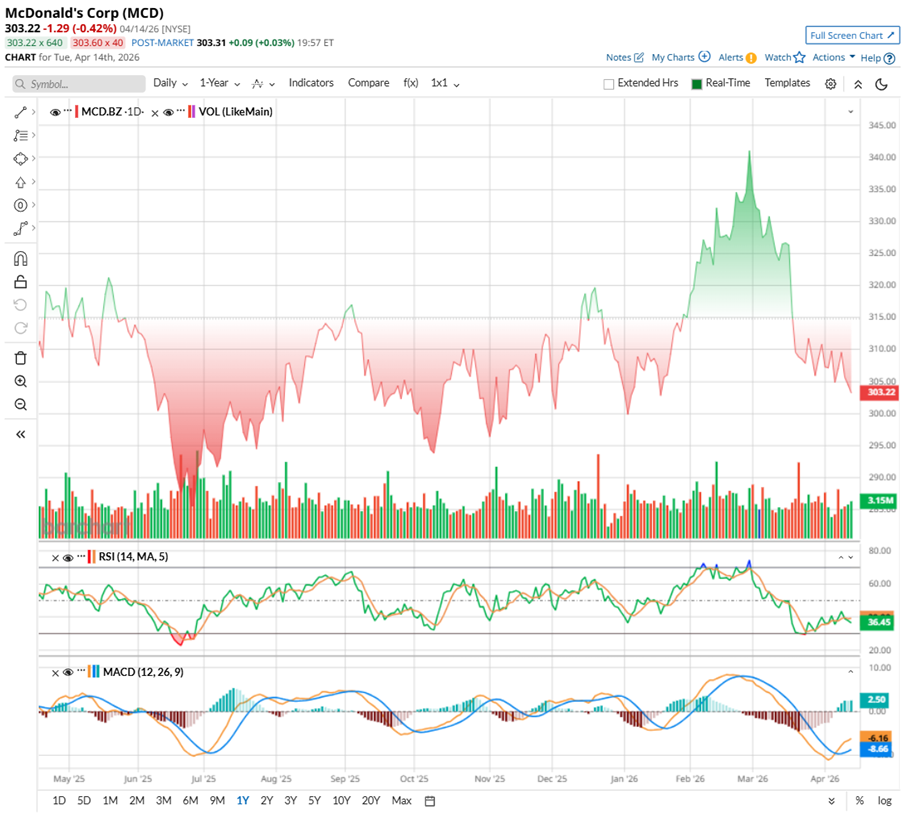

Shares of the fast-food giant have not exactly been sizzling in 2026, but it’s been more of a steady, low-heat phase. After touching a 52-week high of $341.75 in March, the stock has pulled back roughly 10.78%. Over the past month, MCD slipped 7.1% and is down marginally on a year-to-date (YTD) basis, reflecting a pause in momentum rather than a breakdown.

The drag comes from multiple angles. Investors are weighing softer consumer spending, growing resistance to further menu price hikes, and even structural shifts like GLP-1 weight-loss drugs that could gradually change eating patterns.

Yet, the tone is not entirely weak. Volumes have started to pick up again, signaling buying interest returning. Technically, the 14-day RSI has recovered to 39.08 from oversold levels in March, hinting that selling pressure is easing. Meanwhile, the MACD line has flipped above the signal line, a classic bullish sign, with positive histogram bars backing it up.

Valuation-wise, MCD appears reasonably priced rather than deeply discounted. The stock trades at around 23 times forward earnings and 7.5 times sales, both slightly below its five-year averages, indicating some moderation in pricing. However, it still commands a premium compared to sector peers. This reflects investors’ willingness to pay for McDonald’s consistency, global scale, and strong brand positioning. While it may not qualify as a value pick, it remains a dependable choice for those prioritizing stability.

And then comes MCD’s dividend payouts. The company has raised its dividend for 49 consecutive years, quietly building a reputation as one of the most reliable payers in the market and earning its “Dividend Aristocrats” tag. It’s the kind of stock that, along with the aim to grow, keeps serving a regular stream of income, no matter how the broader market appetite shifts.

Last month, the company paid a $1.86 per share quarterly dividend, which translates to $7.44 per share annually. It offers a 2.44% yield, well above State Street SPDR S&P 500 ETF Trust’s (SPY) 1.06% yield. With a payout ratio of 58.8%, there’s still room to grow, making it a steady income pick in uncertain markets.

A Snapshot of McDonald’s Q4 Report

McDonald’s closed 2025 on a strong note, showing that its business still has steady momentum. In the fourth quarter, the company pulled in about $7 billion in revenue, up 9.7% year-over-year (YOY), and ahead of what Wall Street was expecting. What stands out is that growth was not coming from just one area, but was spread across the board.

Company-operated restaurants brought in $2.54 billion, rising 10% YOY, while franchise-operated locations, the backbone of its model, generated $4.3 billion, up 9%. Even the smaller “other revenues” segment saw a sharp 35% jump to $162 million, adding an extra layer of support.

Further, demand looked healthy globally. Comparable sales grew 5.7%, driven by more customers visiting stores and spending slightly more. In the U.S., sales climbed 6.8%, helped by smart promotions and value meals. International markets also held firm, with strong contributions from key regions like the U.K., Germany, and Australia.

On the profitability side, adjusted EPS rose 10.2% YOY to $3.12, while operating income rose 10% to $3.15 billion. McDonald’s continues to generate solid cash, ending the year with $774 million in cash and equivalents and delivering $7.2 billion in free cash flow for 2025. That gives it enough flexibility to invest in growth while continuing to return value to shareholders, even with long-term debt at around $40 billion.

Looking ahead, the focus is clearly on expansion. After exceeding its 2025 targets, McDonald’s plans to open around 2,600 new restaurants globally in 2026. A large chunk of this growth will come from international markets, especially high-growth regions like China, while the U.S. and other mature markets will see steady additions.

This expansion keeps the company on track toward its goal of reaching 50,000 locations by 2027. To support this push, McDonald’s is planning capital spending between $3.7 billion and $3.9 billion, mainly focused on new stores and strengthening its core markets.

Analysts tracking the company expect its EPS to be $13.23, up 8.4% YOY for fiscal 2026, and then surge by another 9.2% annually to $14.44 in fiscal 2027.

What Do Analysts Expect for MCD Stock?

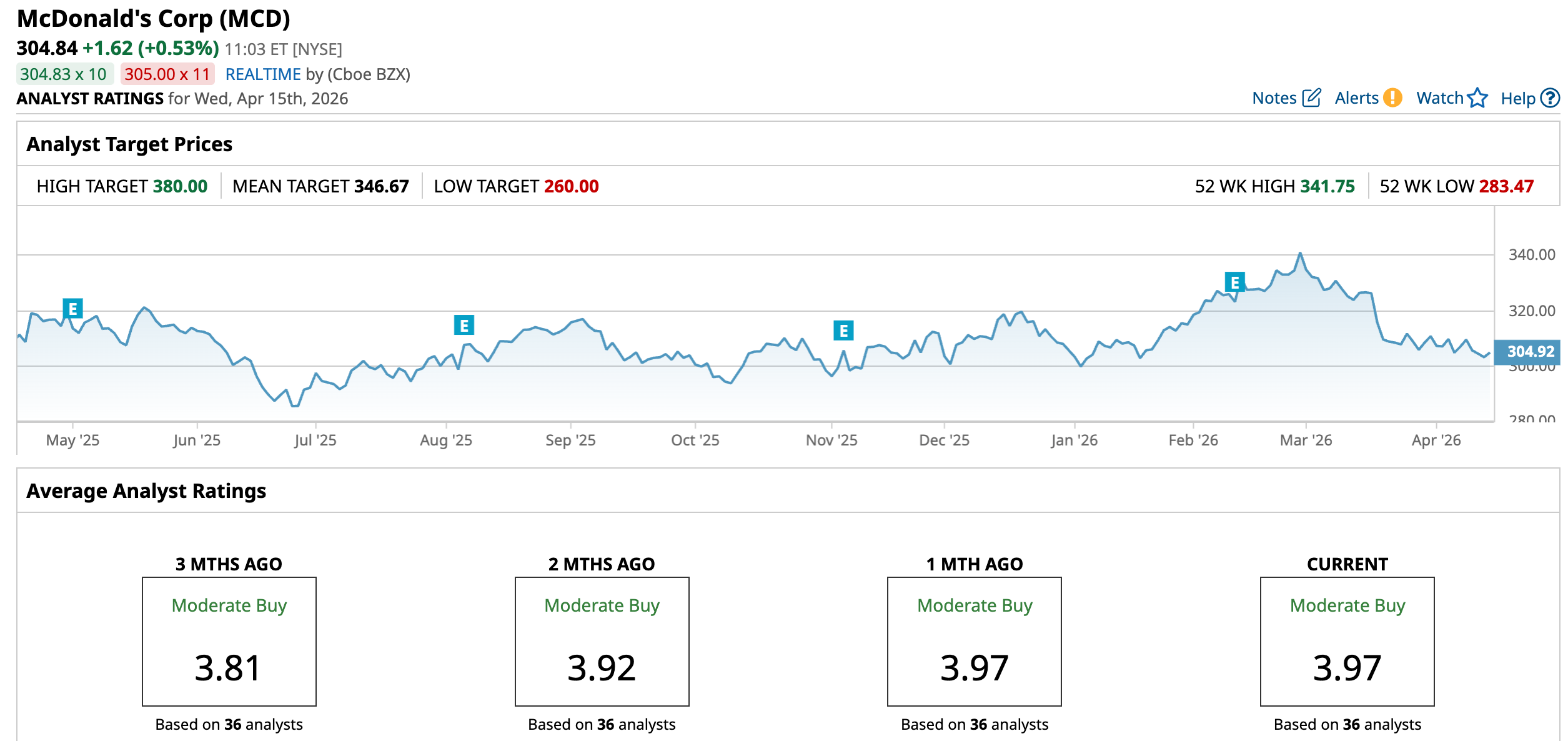

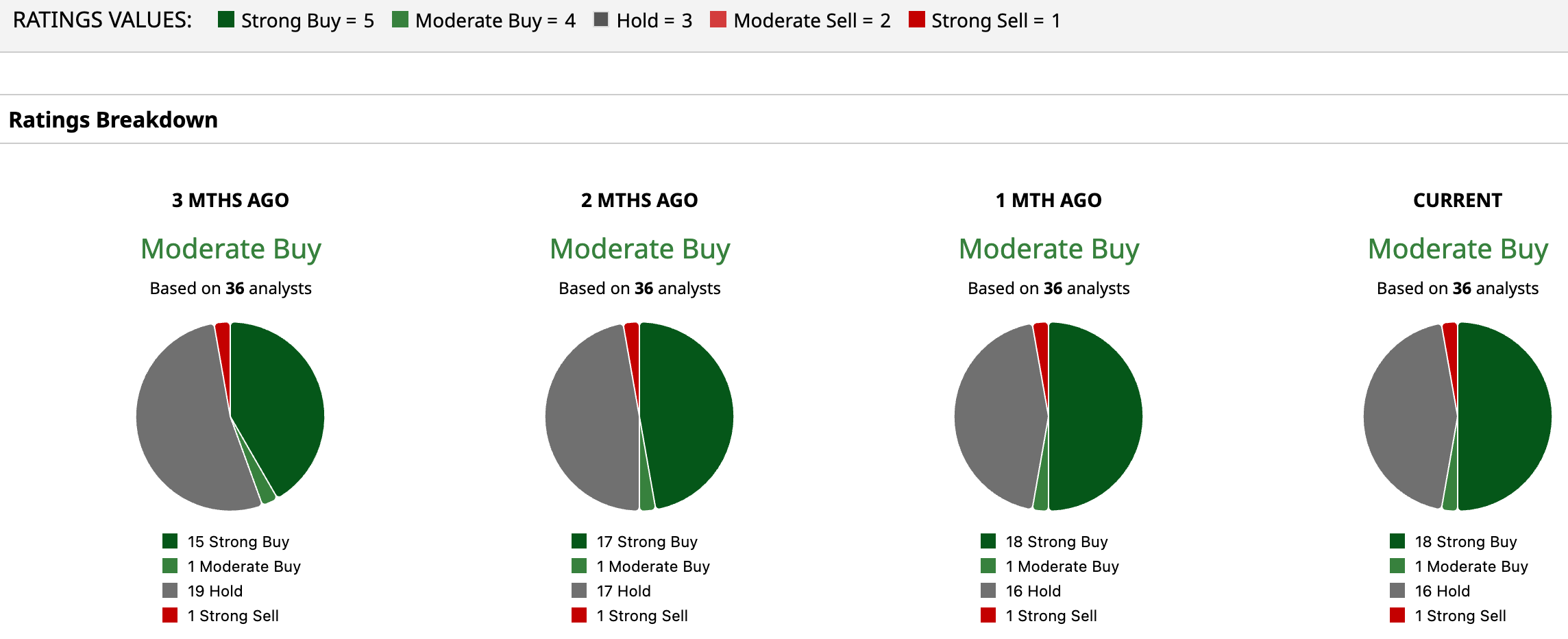

Overall, sentiment on MCD remains bullish, but with a dash of caution. The stock has a consensus rating of “Moderate Buy.” Out of 36 analysts, 18 recommend a “Strong Buy,” one advises a “Moderate Buy,” 16 are playing it safe with a “Hold” rating, and the remaining one has a “Strong Sell” rating.

Its average price target of $346.67 implies upside potential of 13.7%. The Street-high target of $380 suggest MCD stock could rise as much as 24.7% from here.

Final Thoughts on MCD Stock

McDonald’s is clearly trying to add a new growth layer without disturbing its core formula. The beverage expansion opens up a fresh revenue stream, with the potential to lift order values and attract a younger crowd, while the base business continues to deliver steady cash flows and reliable dividends.

What makes this move interesting is how it builds on tested ideas rather than a blind bet. From early pilots to scaled rollouts, the company is leaning into changing consumer habits where drinks are becoming a standalone choice. If executed well, this could quietly strengthen traffic across dayparts and add incremental growth without reinventing the entire menu.

The setup is not without friction – consumer spending remains uneven, pricing power has limits, and the stock still trades at a premium. So, while the long-term story stays intact, the question remains whether this new drinks strategy can meaningfully move the needle, or is it just a refreshing add-on that does not fully justify calling MCD a buy right now.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)