/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

When Artemis II successfully carried astronauts around the Moon, it did not simply mark a return to deep space after decades. It reignited the market’s fascination with the business of space. Slated as the first crewed lunar flyby in over five decades, the mission is a critical test of life-support systems and deep-space capabilities that could shape humanity’s return to the Moon and, eventually, the path to Mars.

According to Bank of America’s (BAC) analyst Ronald Epstein, this is not just a scientific milestone, but an economic signal. Behind the scenes, an entire industrial web is at work, from legacy giants like Lockheed Martin (LMT) and Boeing (BA) to a new wave of agile players. Yet, the road ahead is not without friction. High costs, execution risks, and the urgent push toward reusability are redefining the sustainability of this space race – especially with China accelerating its own lunar ambitions.

But according to the analyst, investor enthusiasm is increasingly tilting toward emerging space and defense tech players, and companies like Rocket Lab Corporation (RKLB) and AeroVironment (AVAV) are gaining traction. Both stocks have delivered solid returns over the past year.

This momentum is being fueled by rising demand for next-generation capabilities, ranging from launch services to drones and autonomous systems, alongside supportive geopolitical tailwinds, reinforcing their position as key growth drivers in an increasingly strategic and fast-evolving space and defense landscape.

For investors looking skyward, this may be the moment to snag these stocks while the runway for growth is still expanding.

Stock #1: Rocket Lab

Rocket Lab, founded in 2006 and headquartered in Long Beach, California, has evolved into a full-scale, end-to-end space company serving both commercial and government clients. It designs, builds, and launches rockets while also offering spacecraft and broader space systems, making it a one-stop shop for space missions.

At the core of its operations is the Electron rocket, a lightweight launch vehicle widely used to deploy small satellites into low Earth orbit. With over 250 satellites launched and more than 1,700 already in orbit carrying its technology, Electron has built a strong reputation for reliability and frequent launches.

Rocket Lab is now aiming bigger with Neutron, its upcoming medium-lift rocket designed for large constellations and deep space missions, capable of delivering a payload of 13,000 kgs. Alongside launch services, the company also focuses on satellite manufacturing and mission management, expanding its reach across the space value chain. With a market cap of about $38.6 billion, Rocket Lab is positioning itself as a key player in the growing space economy.

RKLB stock has seen a lot of ups and downs recently. It got a boost after the U.S.-Iran ceasefire eased market worries, helping aerospace stocks move higher as overall sentiment improved. Better outlook for aviation and stable trade routes also supported the trend.

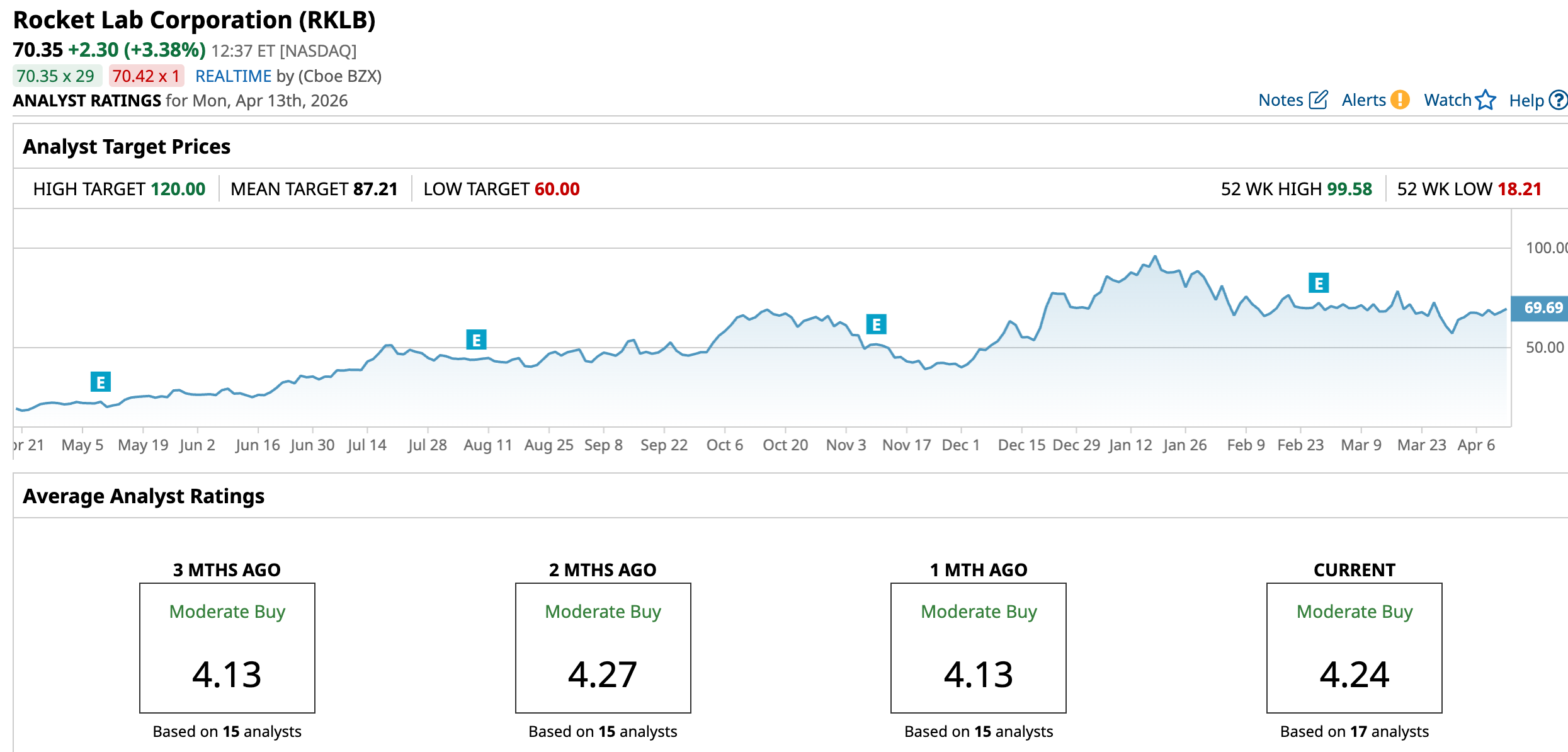

The stock had hit a high of $99.58 in January, but is now about 29% below that level, and in 2026, RKLB is up only marginally at 0.06%. Still, looking at the bigger picture, the stock has delivered strong gains of 255.58% over the past 52 weeks.

This rise has been backed by solid business growth, increasing revenue, and a strong backlog. The company is also benefiting from rising defense demand and expanding through acquisitions. Even with some recent pullback, the overall story still looks positive.

Rocket Lab continues to build strong momentum, with its financial results showing steady growth across the board. In Q4 2025, the company reported revenue of $179.7 million, up 35.7% year-over-year (YOY), though it posted a loss of -$0.09 per share. For fiscal 2025, Rocket Lab delivered record revenue of $602 million, marking a solid 38% annual increase.

Operationally, 2025 was a milestone year. The company completed 21 launches across its Electron and HASTE vehicles, achieving a 100% success rate. At the same time, it made meaningful progress on its next-generation Neutron rocket, reaching key development milestones. Also, Rocket Lab secured its largest contract to date – an $816 million award from the U.S. Space Development Agency to design and manufacture 18 satellites. In addition, it successfully launched two spacecraft for NASA and the University of California, Berkeley, for the ESCAPADE Mars mission, showcasing its deep-space capabilities.

The company ended the year with a record backlog of $1.85 billion, up 73% YOY, providing strong revenue visibility. And, it is expanding its space systems segment through acquisitions like Optical Support and Precision Components. With this momentum and a strong pipeline, management expects a solid start to 2026, supported by continued demand across launch and space systems.

Looking ahead to Q1, management expects revenue to come in between $185 million and $200 million, with both the Space Systems and Launch segments set to grow annually. However, margins are likely to ease a bit, with non-GAAP gross margins projected in the 39% to 41% range, compared to 44.3% in Q4.

Meanwhile, Wall Street analysts tracking the company anticipate losses to be about -$0.07 per share in Q1, while revenue is projected to be around $190.8 million. Looking further ahead to fiscal 2026, confidence builds further. Losses are anticipated to narrow by 52.6% annually to -$0.18 per share, and further shrink by 44.4% YOY to -$0.10 per share.

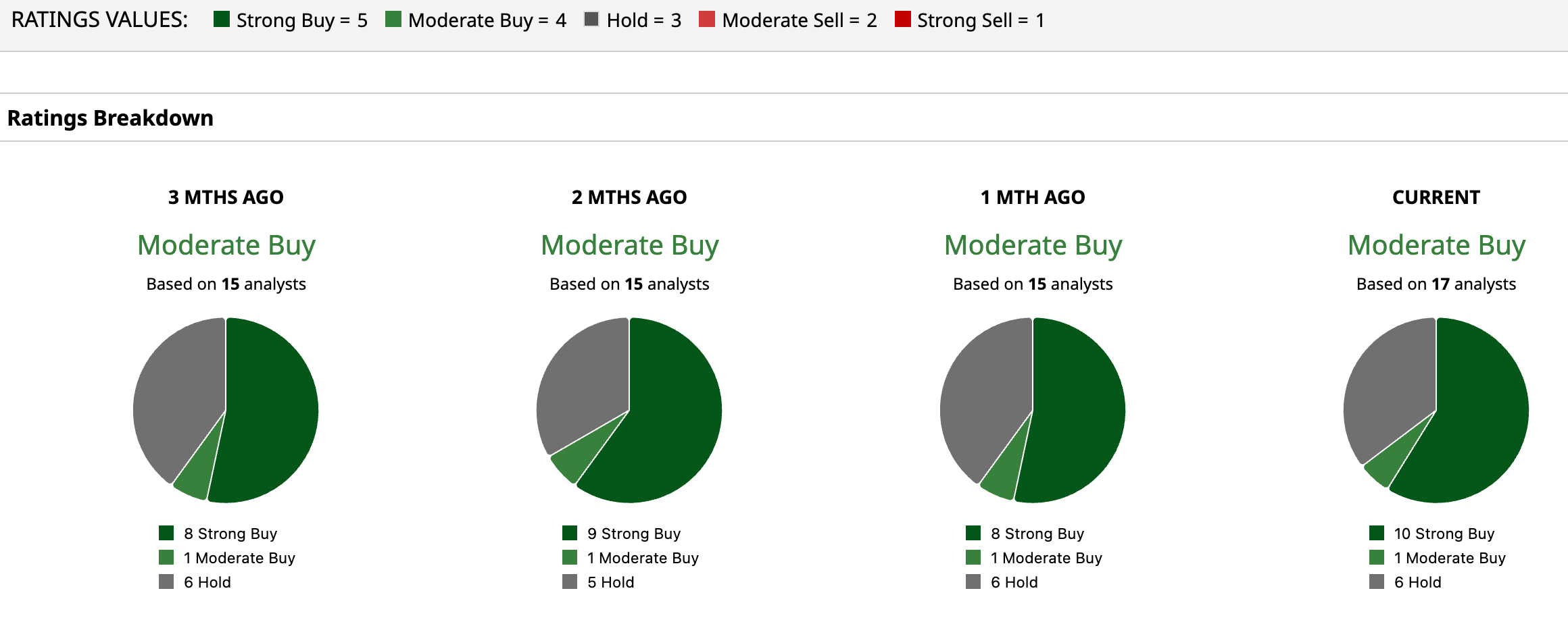

Overall, analysts are upbeat on RKLB, with a “Moderate Buy” consensus. Of the 17 analysts tracking the stock, 10 have a “Strong Buy,” one advises a “Moderate Buy,” and the remaining six are on the sidelines with a “Hold” rating.

RKLB has an average price target of $87.21, implying roughly 24% upside potential from current levels. On the bullish end, the Street-high target of $120 points to even sharper gains of 70.6%.

Stock #2: AeroVironment

Founded in 1971 and based in Arlington, Virginia, AeroVironment is a defense technology company focused on autonomous and robotic systems for military and government clients. Its portfolio spans unmanned aircraft systems (drones), loitering munitions, counter-drone and directed energy solutions, as well as space, cyber, and communication systems. The company also develops advanced robotic platforms, positioning itself at the center of modern defense innovation. AeroVironment has a market capitalization of about $9 billion.

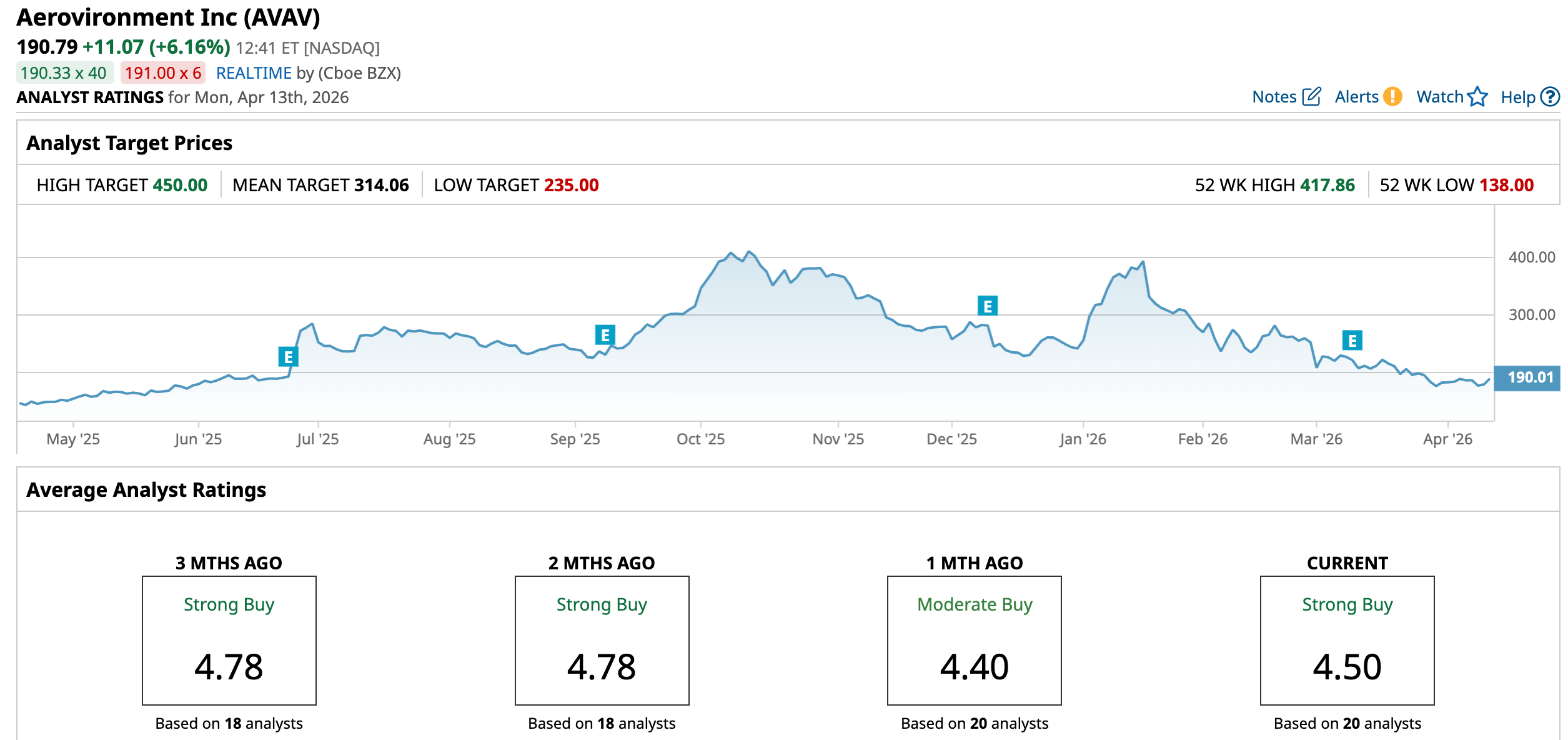

AeroVironment’s stock has had a volatile run in 2026, moving more sideways than trending up. It started strong, climbing close to its all-time high of $417.86 in October, but then saw a sharp pullback, dropping 54.3% from that peak. The stock briefly bounced during a defense-sector rally in March, moving into the mid-$200s, but now sits below $200.

There have been sharp swings along the way. On March 2, for instance, shares jumped to around $303, only to fall back to nearly $196 by the end of the same session. Overall, AVAV is down about 21.6% year-to-date (YTD), largely due to the cancellation of the SCAR contract with the U.S. Space Force.

Still, the bigger picture shows some strength. Over the past 52 weeks, AVAV stock is up roughly 29.6%, supported by strong drone demand and contract wins, even as recent uncertainty and profit-taking have weighed on momentum.

AVAV stock may look expensive at first glance, priced around 60.40 times forward adjusted earnings, well above its peers and historical average. But digging a little deeper, its price-to-sales ratio of 4.76 times sits below past historical median, hinting that the premium may be partly justified by its growth story.

AeroVironment delivered a mixed Q3 earnings report for fiscal 2026 on March 10, generating a revenue of $408.04 million, up 143.3% YOY, while non-GAAP EPS rose 113.3% annually to $0.64. On the surface, the quarter looked disappointing, as both top and bottom lines came in below expectations. But the headline miss does not fully capture what’s going on underneath.

The shortfall was largely due to timing issues in revenue recognition and some adjustments in its Space segment. Despite that, demand for AeroVironment’s solutions remains strong. Order flow stayed healthy, and the funded backlog continued to grow. Management is also staying disciplined, ramping up manufacturing ahead of demand and pushing commercialization efforts to improve margins and speed up delivery.

A key boost came from the BlueHalo acquisition, which added $85.1 million in product revenue and $91.4 million in service revenue this quarter. Segment-wise, Autonomous Systems (AxS) revenue amounted to $278.7 million, while Space, Cyber, and Directed Energy (SCDE) revenue came in at $129.3 million. Funded backlog, as of Jan. 31, 2026, climbed to $1.1 billion, up significantly from $726.6 million as of April 30, 2025.

Nevertheless, cash flow remains a concern. Operating cash outflow widened to $173.9 million for the nine-month period, compared to just $1 million a year ago. Still, with about $290 million in cash and relatively low short-term debt, liquidity is not a near-term issue.

The numbers set the company up for a potentially record Q4 and a strong start to fiscal 2027. For fiscal 2026, management expects revenue of between $1.85 billion and $1.95 billion, while non-GAAP EPS is anticipated to be between $2.75 and $3.10.

Wall Street monitoring AeroVironment anticipates its revenue for fiscal 2026 to be $1.9 billion, while EPS is projected to be $2.94. Looking further ahead to fiscal 2027, profit is expected to surge 26.9% annually to $3.73 per share.

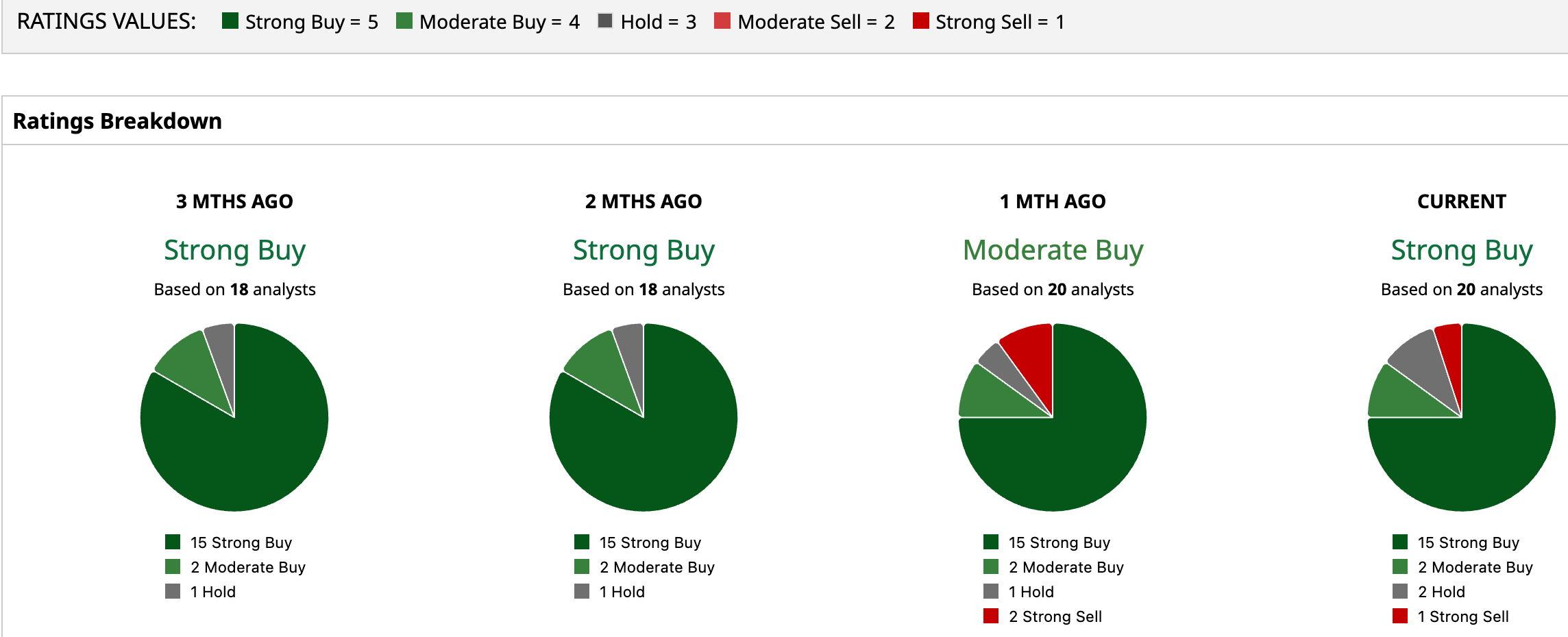

Analysts are confident, with AVAV stock having an overall “Strong Buy” rating. Of the 20 analysts tracking the stock, 15 recommend a “Strong Buy,” two have a “Moderate Buy,” two are cautious with a “Hold” rating, while the remaining one analyst takes a bearish stance, advising a “Strong Sell.”

AVAV’s average target of $314.06 suggests an upside potential of 64.6% from the current price levels. The Street’s highest $450 price target hints the stock could rally as much as 135.9%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)