/The%20DocuSign%20headquarters%20by%20Tada%20Images%20via%20Shutterstock.jpg)

Investors are bailing on San Francisco-headquartered DocuSign (DOCU) on Friday after senior Citi analyst Tyler Radke turned bearish on the company.

As Radke downgraded DOCU to “Neutral” and trimmed his price target nearly in half, DocuSign's relative strength index (14-day) slipped into the mid-30s, indicating the bearish momentum may soon reach exhaustion.

DocuSign stock has been a major laggard in 2026, currently down nearly 40% versus its year-to-date high.

Why Citi Turned on DocuSign Stock

In a research note dated April 10, Radke cited a notable shift in the application layer software landscape. His primary concern is the fast-growing private AI companies’ revenue, which is now beginning to outpace conventional incumbents.

Nonetheless, the Citi analyst acknowledged that DocuSign is still a leader in digital agreements, but said it lacks “exciting 12-month catalysts” to justify a bullish view.

According to him, the evolution of AI agents is fundamentally reshaping workflows, potentially commoditizing eSignature services and disrupting the traditional seat-based licensing models that DOCU relies on.

Insiders Have Been Unloading DOCU Shares

The broader bear thesis on DocuSign shares is anchored by a combination of stagnant growth and valuation concerns.

Despite a recent earnings beat, the firm’s net income for the trailing 12 months came in down an alarming 70%, signaling it’s struggling to maintain the pandemic-era momentum.

Investors remain wary of significant insider selling as well, given that top executives have unloaded millions of company shares in early 2026.

Still, DOCU is trading at a forward price-to-earnings (P/E) multiple of nearly 27x, which looks stretched given that the company runs a major risk of AI disruption.

What’s the Consensus Rating on DocuSign?

Investors should note, however, that other Wall Street firms disagree with Citi on DOCU stock — betting the firm’s new Intelligent Agreement Management (IAM) platform positions it well to navigate tightening IT budgets and stiff competition from AI-native startups.

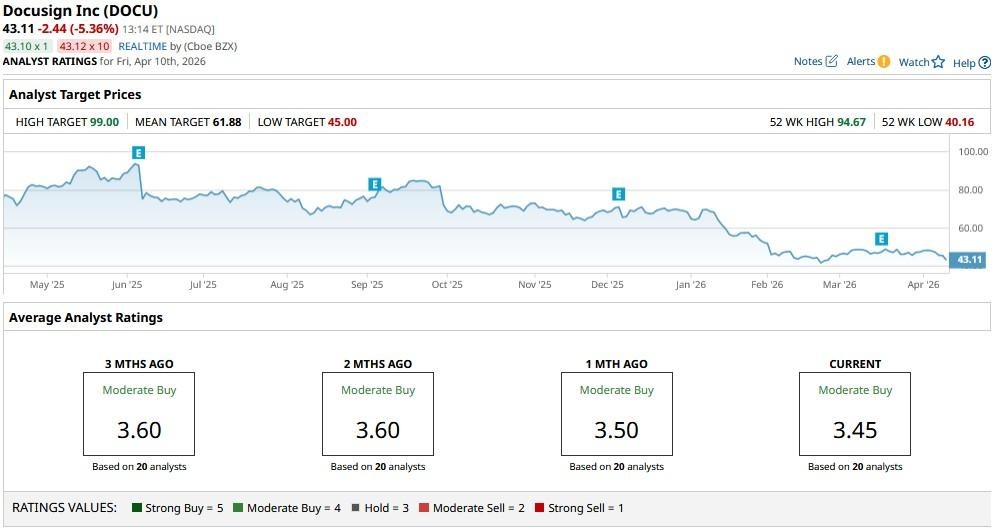

According to Barchart, the consensus rating on DocuSign is currently a “Moderate Buy,” with the mean price target of about $62 indicating potential upside of nearly 40% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)