/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

Wall Street has bounced back on the news of the ceasefire between the U.S. and Iran. While this might not signal the end of the war, so far, stocks are overjoyed at the prospect of the heated exchanges stopping, albeit expectedly for a short time. Against this backdrop, Wedbush analysts believe the “Magnificent Seven” stocks and tech names might see a “risk-on” environment. Analysts wrote that the geopolitical backdrop has created an oversold situation for the seven extraordinary names.

Magnificent Seven extraordinaire Amazon.com (AMZN) has also experienced a dip due to the current situation and investor concerns over its rising capital expenditures. But, with Wedbush’s vote of confidence, should you consider investing in the stock now?

About Amazon Stock

This leading global technology and retail company, whose established core businesses (online retail, cloud computing via Amazon Web Services, and logistics) remain highly entrenched and efficient, serves as the primary engine and funding source for a growing portfolio of new initiatives. Headquartered in Seattle, Washington, the company has a market capitalization of $2.38 trillion.

Coming to Amazon’s new initiatives, the company has aggressively pushed into AI and cloud infrastructure, rolling out custom silicon chips (Trainium and Inferentia) and AI-ready services on AWS to capture workloads from the generative AI boom. It is also building Project Kuiper (now called Amazon Leo), a low‑earth‑orbit satellite network. In addition, it is deepening its footprint in healthcare and bolstering its presence in lucrative regions (such as its huge investment announcement for India).

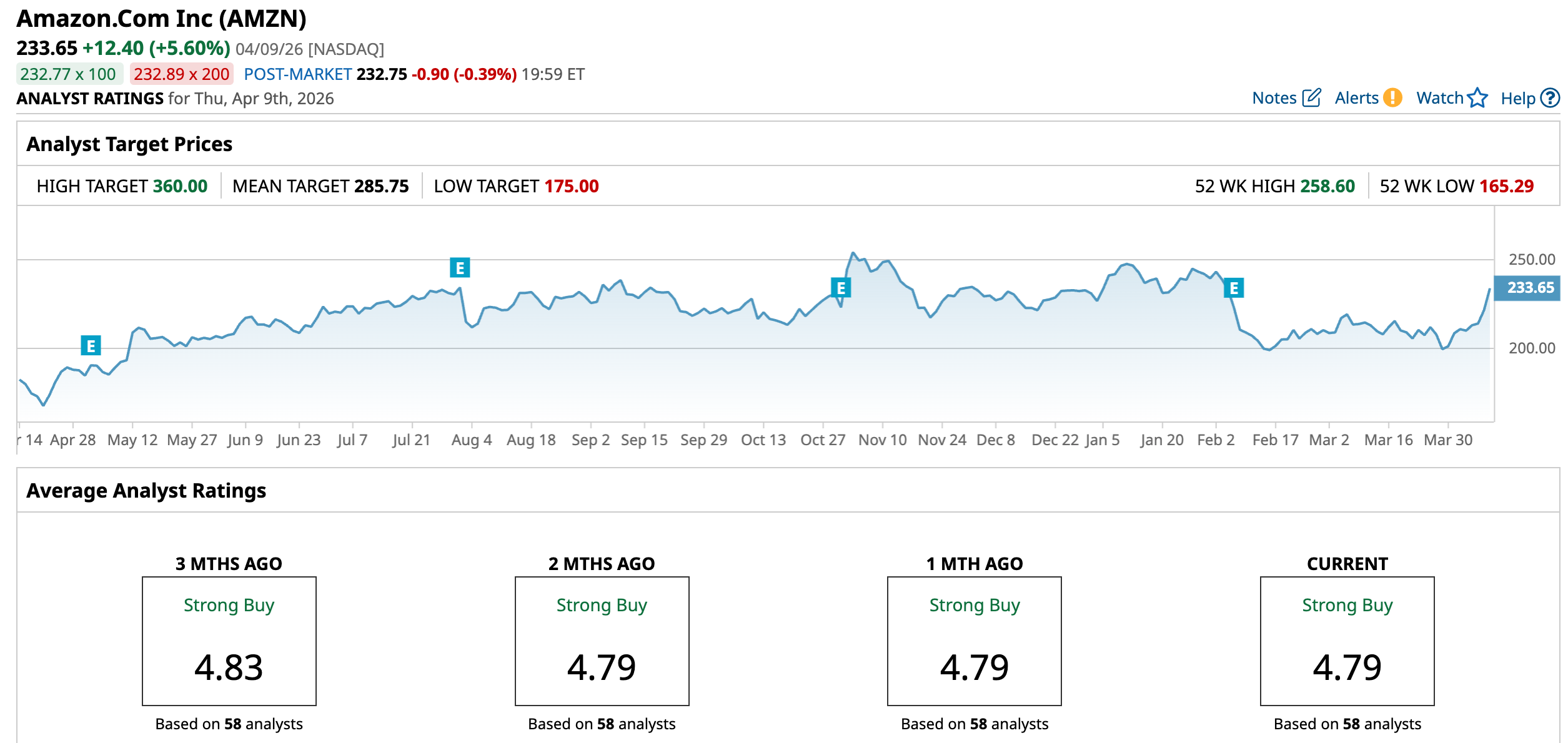

Over the past 52 weeks, Amazon’s stock has gained 22.26%. However, it has come under pressure recently as investors have been spooked by the company’s AI and cloud infrastructure spending. The shares are down 1.22% year-to-date (YTD). It had reached a 52-week high of $258.60 in Nov. 2025, but is down 9.65% from that level.

Amazon’s stock is currently trading a bit above its 50-day moving average. Its forward-adjusted price-to-earnings (non-GAAP) ratio of 27.60 times is higher than the industry average of 14.75 times.

Amazon Q4 Shows Strong AWS and Retail Growth Despite Heavy AI Spending

For the fourth quarter, Amazon’s total net sales increased by 13.6% year-over-year (YOY) to $213.39 billion, which was higher than the $211.46 billion that Wall Street analysts had expected. The North American segment reported net sales of $127.08 billion, up 9.9% from the prior-year period. Moreover, AWS net sales increased 23.6% YOY to $35.58 billion.

Amazon’s operating income increased by 17.8% to $24.98 billion. However, this was affected by the resolution of tax disputes associated with its store business in Italy, the settlement of a lawsuit, estimated severance costs, and asset impairments primarily related to physical stores. The company’s EPS climbed 4.8% YOY to $1.95, missing the $1.98 consensus estimate.

However, investors were concerned about Amazon’s plans to spend $200 billion in capex this year, with the majority of it going towards AI infrastructure, including data centers, chips, and networking equipment. CEO Andy Jassy has defended the company’s AI ambitions, stating that Amazon is “investing to be the meaningful leader.”

For the current year, Wall Street analysts expect Amazon’s EPS to be $7.78, indicating an 8.5% YOY increase, followed by a 19.8% growth to $9.32 in the following year.

Here’s What Analysts Think About Amazon’s Stock

Despite investor concerns about its heavy AI spending, Wall Street analysts have maintained a positive view of the retail and tech giant. Recently, analyst Deepak Mathivanan of Cantor Fitzgerald maintained an “Overweight” rating on the stock and raised the price target to $260 from $250.

Wells Fargo analysts also raised the price target on Amazon from $304 to $305, while maintaining an “Overweight” rating and named it as a “Top Internet Pick” for 2026. The analysts cited AWS revenue acceleration and a positive inflection in the company’s free cash flow as reasons for this optimism.

In addition, Citi analysts increased the price target on AMZN from $265 to $285 and kept a “Buy” rating, predicting 28% YOY revenue growth for AWS in the first quarter and 29% in 2026. This growth rate is expected to accelerate to 37% in 2027 as the partnerships between Amazon’s Anthropic and OpenAI kick in.

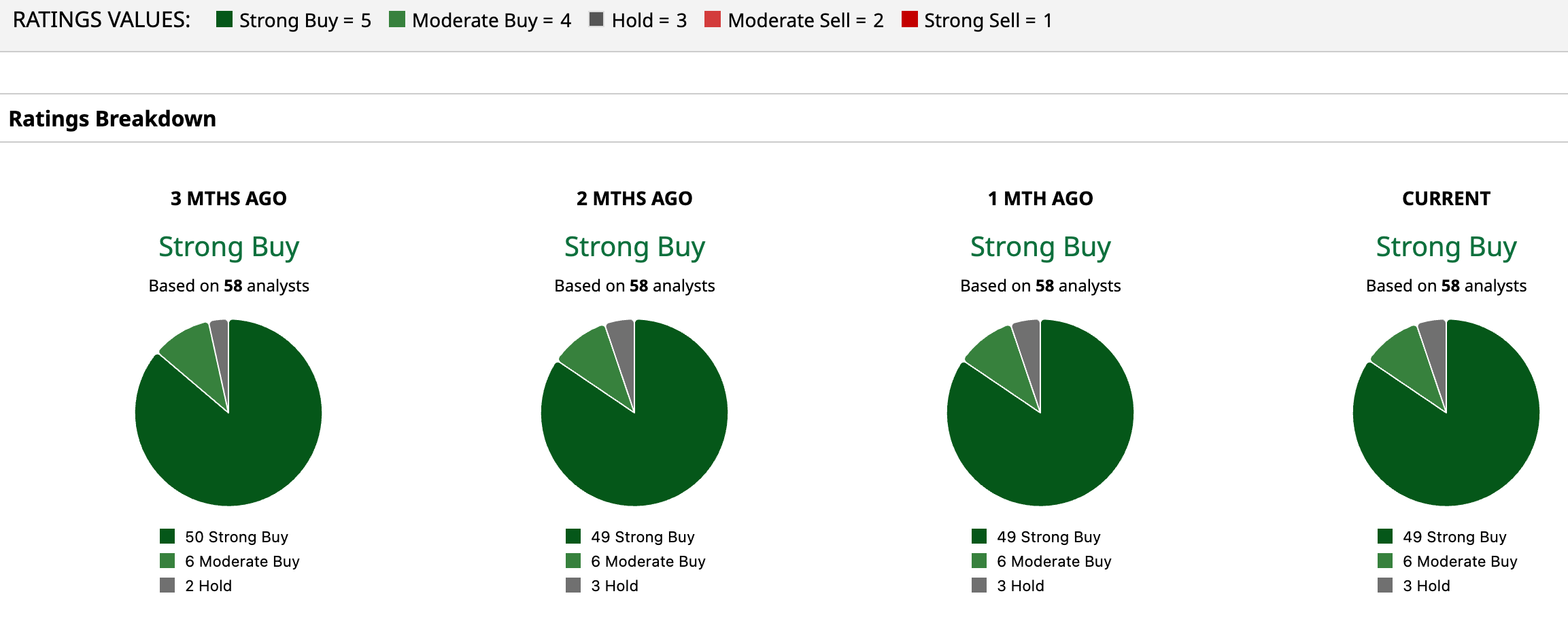

Amazon has been in the spotlight on Wall Street for some time now, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 58 analysts rating the stock, a majority of 49 analysts have given it a “Strong Buy” rating, six analysts suggest “Moderate Buy,” while three analysts are playing it safe with a “Hold” rating. The consensus price target of $285.75 represents 22.3% upside from current levels. The Street-high price target of $360 indicates a 54.1% upside.

Key Takeaways

While the step-up in Amazon’s capex has concerned investors, it might be supported by the step-up in its core retail and AWS business. The ceasefire news also brings a fresh surge of optimism to the market, and Amazon might be better positioned to take charge of the rally given its proven record as a market leader and analysts’ bullish sentiment. Therefore, Amazon’s stock might be a buy on its dip.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)