/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

For decades, Arm Holdings plc (ARM) has been designing chip architectures and licensing them to the world’s biggest players, earning steady royalties without ever making chips itself. But now, the company is shifting gears.

It has begun developing its own physical silicon, introducing an AI-focused data center CPU tailored for agentic workloads, where CPUs act as the always-on coordinators alongside GPUs. This move signals a deeper push into vertical integration, aiming to capture more value from the artificial intelligence (AI) boom, even if it means stepping into the arena with its own customers.

Despite the strong run-up in ARM stock after the news, Morgan Stanley analyst Lee Simpson is taking a more cautious stance. He sees a few hurdles that could slow the rally and believes this shift will need time to show real results, leading him to downgrade the stock and adopt a more balanced outlook.

While Arm’s strategic shift is clear, near-term challenges remain, such as soft demand, DRAM constraints, and rising R&D costs before chip revenues scale. There is also a new tension that stepping into silicon risks straining relationships with existing partners. With growth visibility clouded and margins under pressure, the story looks less straightforward than before.

After the downgrade, ARM stock slid. So, is this a dip worth buying, or a signal to step aside?

About Arm Holdings Stock

Arm Holdings has chosen a path very different from typical chip companies. Founded in 1990 and headquartered in Cambridge, the U.K., the company did not chase factories or chip production. Instead, it focused on designing the architecture that powers chips – the invisible layer running inside billions of devices, from phones to advanced computing systems. That quiet, behind-the-scenes role made Arm Holdings a key building block of the digital world.

Its model is simple but powerful. Arm Holdings licenses its designs to a wide range of partners, who then build their own processors and pay fees and royalties. This allows the company to scale globally without the high costs of manufacturing. Over time, its reach has expanded beyond smartphones into data centers, automotive, and AI-driven applications.

Now, the story is shifting again. With the launch of its AGI-focused CPU, Arm Holdings is stepping closer to building its own silicon. It is a big move that signals a deeper push into AI infrastructure and a more direct role in shaping the future of computing. Its market capitalization currently stands at $152 billion.

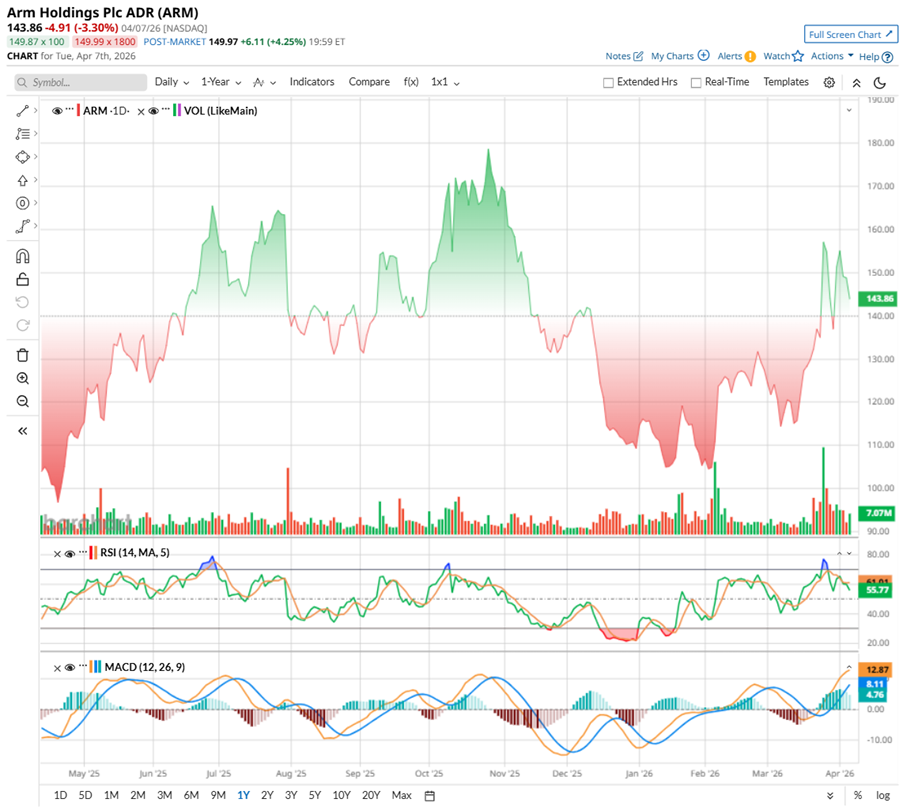

The growing attention around Arm Holdings is clearly playing out in its stock performance. And, the momentum has been steadily building. In just the past month, the stock moved up about 27.38%, supported by renewed interest after its latest chip announcement. Stepping back, the gains look even stronger – up 24.4% over the last three months - as investors lean into its expanding AI story.

And this is not just a short-term move. Over the past 52 weeks, shares have jumped 69.77%.

Nevertheless, the ride has not been completely smooth. This week, the stock faced some pressure after analysts’ downgrades, slipping 3.38% in the last five trading days.

Still, from a technical standpoint, the tone remains positive. The 14-day RSI sits 57.28, suggesting momentum is picking up without being overheated. Meanwhile, the MACD line has crossed above the signal line, with positive histogram bars, both pointing toward strengthening bullish momentum as confidence slowly rebuilds.

Valuation-wise, ARM stock looks expensive. The stock trades at about 31.18 times forward sales and around 81.63 times forward adjusted earnings. But investors seem willing to pay that price now. This is because Arm is no longer just a licensing company. It is getting more involved in AI through royalties, compute subsystems, and even its own chips. That bigger opportunity is slowly changing how the market looks at the stock.

Arm Holdings Beats Q3 Projections

Arm Holdings released its fiscal third quarter on Feb. 4, reporting revenue of $1.24 billion, up 26% year-over-year (YOY), marking its fourth straight billion-dollar quarter. What stood out was the balance. Royalty revenue climbed 27% annually to $737 million, while licensing and other revenue rose 25% to $505 million, showing growth was not tied to just one segment. Non-GAAP EPS came in at $0.43, up 10.3% and ahead of expectations.

ARM is no longer just about smartphones. Growth was driven by rising adoption of Armv9, stronger traction for Arm Compute Subsystems (CSS), and increasing use of Arm-based chips in data centers. The company has already signed 21 CSS licenses, well ahead of plan, while management expects its share among top hyperscalers to approach 50%. In a world where AI infrastructure is expanding fast, CPUs are back in focus, and Arm Holdings is quietly positioning itself right at the center of that shift.

Financially, the company looks steady. Cash and equivalents stood at $2.8 billion as of Dec. 31, 2025, and trailing twelve-month free cash flow reached $893 million. That kind of balance sheet gives the firm room to invest as it leans into its next phase.

Looking ahead, management is guiding for another strong quarter. For fiscal Q4 2026, Arm Holdings expects revenue of around $1.47 billion, plus or minus $50 million, along with non-GAAP EPS of about $0.58, plus or minus $0.04. The outlook reflects confidence – not just in current demand, but in where the business is headed.

And that future is getting bigger. With its newly announced AGI-focused CPU, Arm is stepping deeper into silicon, aiming to build a meaningful revenue stream over time. The company is targeting up to $15 billion in annual revenue from this segment within five years – a bold ambition that explains why excitement around the stock has picked up. The road ahead may take time, but for now, the story is clearly gaining pace.

Arm Holdings is anticipated to release its Q4 earnings report next month. Analysts tracking the company expect revenue to hit $1.47 billion, while EPS is forecasted to be around $0.38. Fiscal 2026 EPS is anticipated to decline 20% YOY to $0.85. However, looking further ahead to fiscal 2027, EPS is projected to surge by 40% annually to $1.19.

What Do Analysts Expect for Arm Holdings Stock?

Arm Holdings is drawing attention amid the recent chip news, but Morgan Stanley sees the path ahead getting tougher. Analyst Lee Simpson agrees that Arm’s move into selling its own CPUs is “strategically sound,” opening new growth beyond its royalty model. Still, he believes the excitement may be running ahead of reality.

He downgraded the stock to “Equal-Weight” from “Overweight” and set a price target to $150, suggesting that while Arm remains key to the AI shift, real financial gains from “agentic” AI could take time.

He pointed to several near-term risks. Rising R&D and engineering costs are likely to weigh on margins before chip revenues meaningfully scale.

Also, he flags caution about the ongoing DRAM chip shortages across the industry. As prices rise and supply stays tight, electronics companies may struggle to produce enough devices, which could quietly reduce the royalties Arm Holdings earns from its designs.

Finally, there are the concerns about Arm Holdings’ legal battle with Qualcomm (QCOM). A recent ruling could limit Arm’s ability to increase royalty rates, and a possible second round of litigation adds further uncertainty. Meanwhile, the company’s move into making its own CPUs could put it in competition with its own customers. While big players like Nvidia (NVDA) and Apple (AAPL) might stick due to long-term deals, others may try to depend less on Arm.

Overall, Simpson believes the long-term story is strong, but the transition comes with execution, competitive, and market risks.

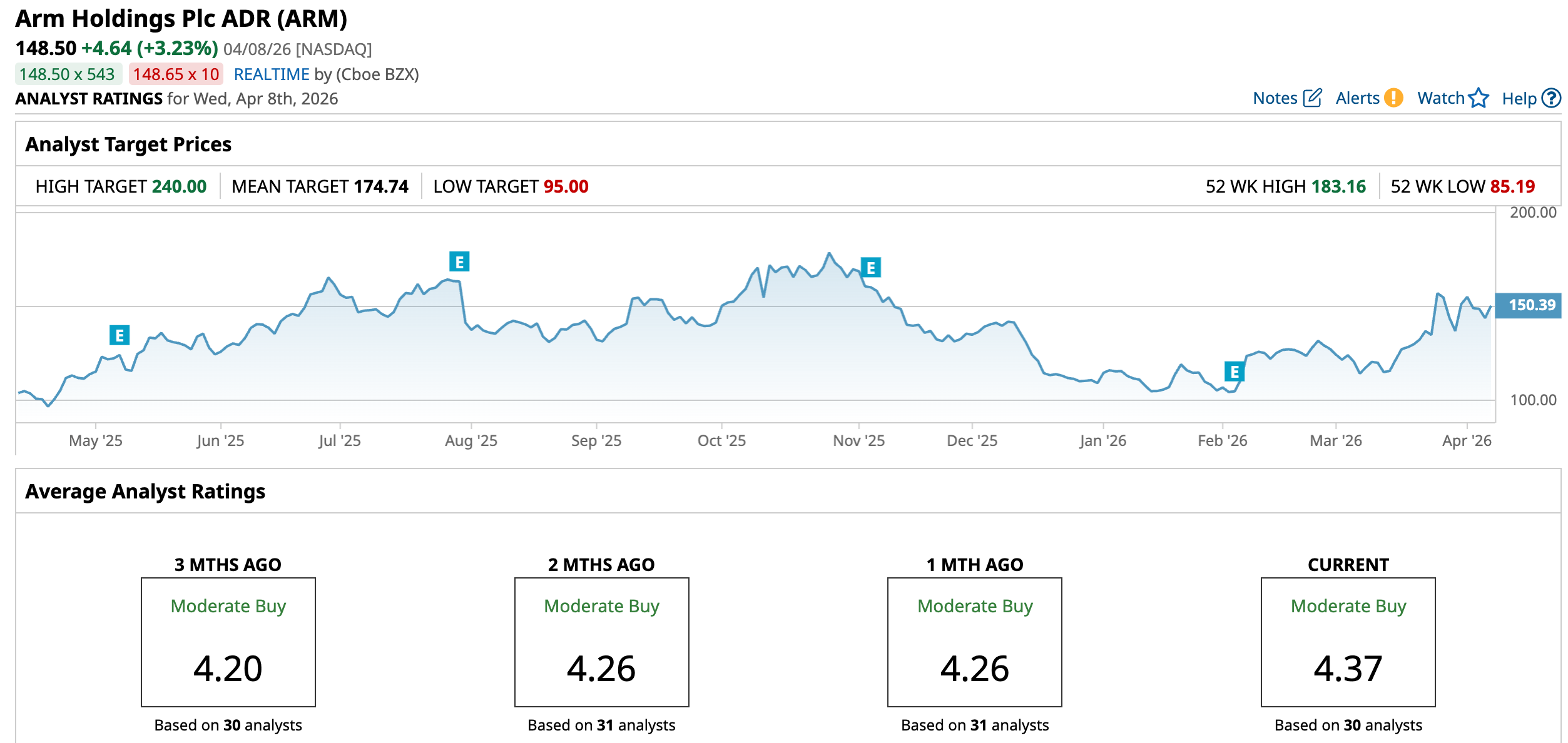

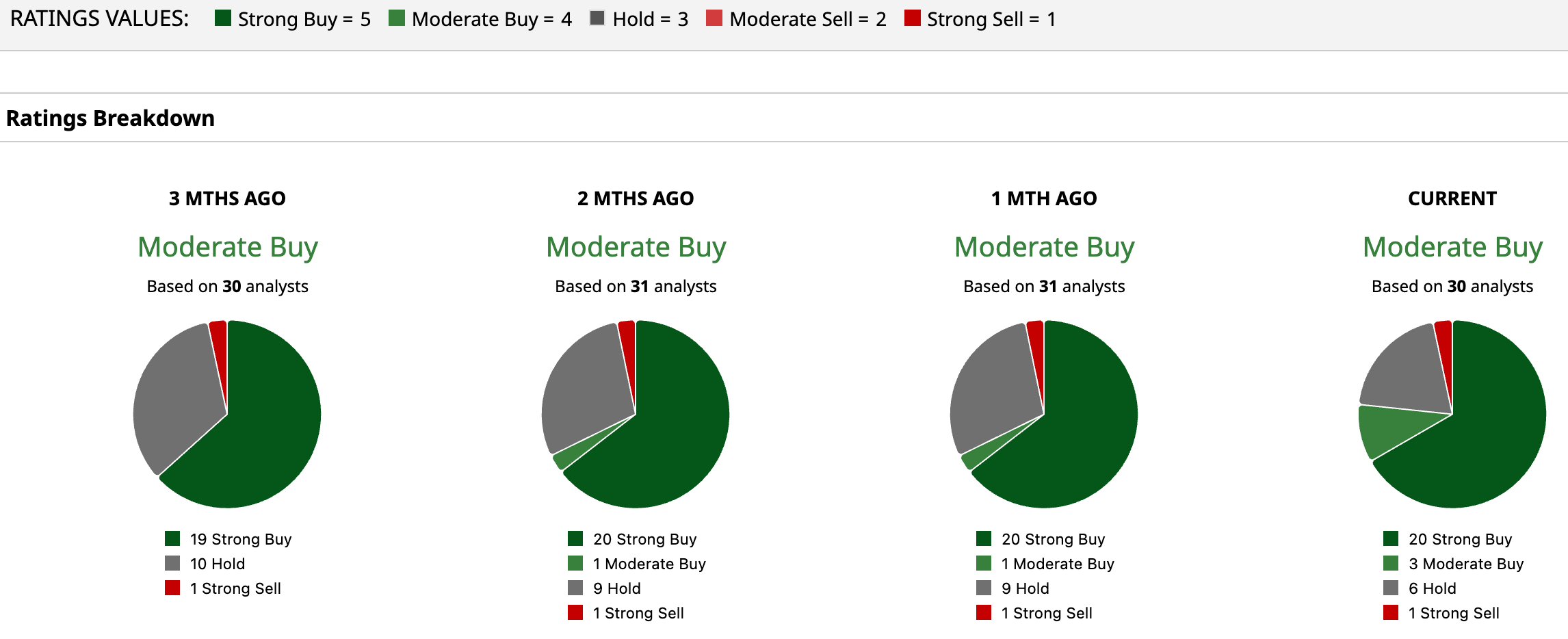

Additionally, Wall Street is bullish on ARM, but with a dash of caution, and giving a consensus “Moderate Buy” rating. Of the 30 analysts rating the stock, a majority of 20 analysts have recommended a “Strong Buy,” three advise a “Moderate Buy,” six analysts have a “Hold” rating, and the remaining one is outright skeptical, suggesting a “Strong Sell.”

Meanwhile, the stock has a mean price target of $174.74, which suggests an upside potential of 17.67% from current price levels. Meanwhile, the Street-high target of $240 implies ARM could rise as much as 61.62%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)