Caught Between Beijing and the Strait: What Is Moving Soybeans

The soybean market is currently highly sensitive to developments on two interconnected geopolitical fronts: U.S.-China trade relations and the ongoing conflict involving Iran and the Strait of Hormuz.

Chicago soybean futures slumped as much as 3.5% on March 16 when President Trump threatened to delay a highly anticipated summit with Chinese President Xi Jinping unless Beijing helped unblock the Strait of Hormuz. This headline crystallized the market's core vulnerability: China is the single largest buyer of U.S. soybeans, and any deterioration in that commercial relationship is immediately reflected in price. As of early April, U.S. Treasury Secretary Bessent and Chinese counterparts met in Paris to prepare for a potential Trump-Xi meeting, with China signaling openness to buying more U.S. agricultural goods. That development offered a degree of relief, though headlines on whether the summit proceeds remain a live market catalyst.

On the supply side, geopolitical escalations in the Middle East and shipping closures on the Strait of Hormuz have fueled gains in the global edible oils complex since late February, providing spillover support to soy oil, which now accounts for 51.9% of the crush margin at Illinois facilities. Surging fertilizer prices linked to the Iran war have also added uncertainty to 2026 planting decisions, with analysts noting that early survey responses submitted before the conflict's full impact on input costs may not fully reflect farmer intentions by the time planting begins.

On the demand side, export headwinds remain a persistent drag. As of March 12, total U.S. soybean export commitments for the 2025/26 marketing year stood at 36.79 million metric tons, representing only 86% of the USDA's current annual estimate and lagging the five-year average pace of 94% for this date. Year-over-year export commitments are running 19% below last year, reflecting the ongoing challenge of competing with a massive Brazilian crop. The USDA left Brazil's 2025/26 crop unchanged at 180 million metric tons in the March WASDE, with harvest running behind last year's pace due to rain delays.

The domestic crush story, however, offers genuine support. Strong processing margins in the Eastern Corn Belt have driven the uptick in soymeal values over the past four months, and USDA raised 2025/26 crush estimates to 2.575 billion bushels in the March WASDE. Meanwhile, the USDA's March 31 Prospective Plantings report came in below trade expectations for soybeans at 84.7 million acres, versus the average analyst estimate of 85.5 million acres, which provided a near-term supportive jolt to futures prices.

What the Market Has Done

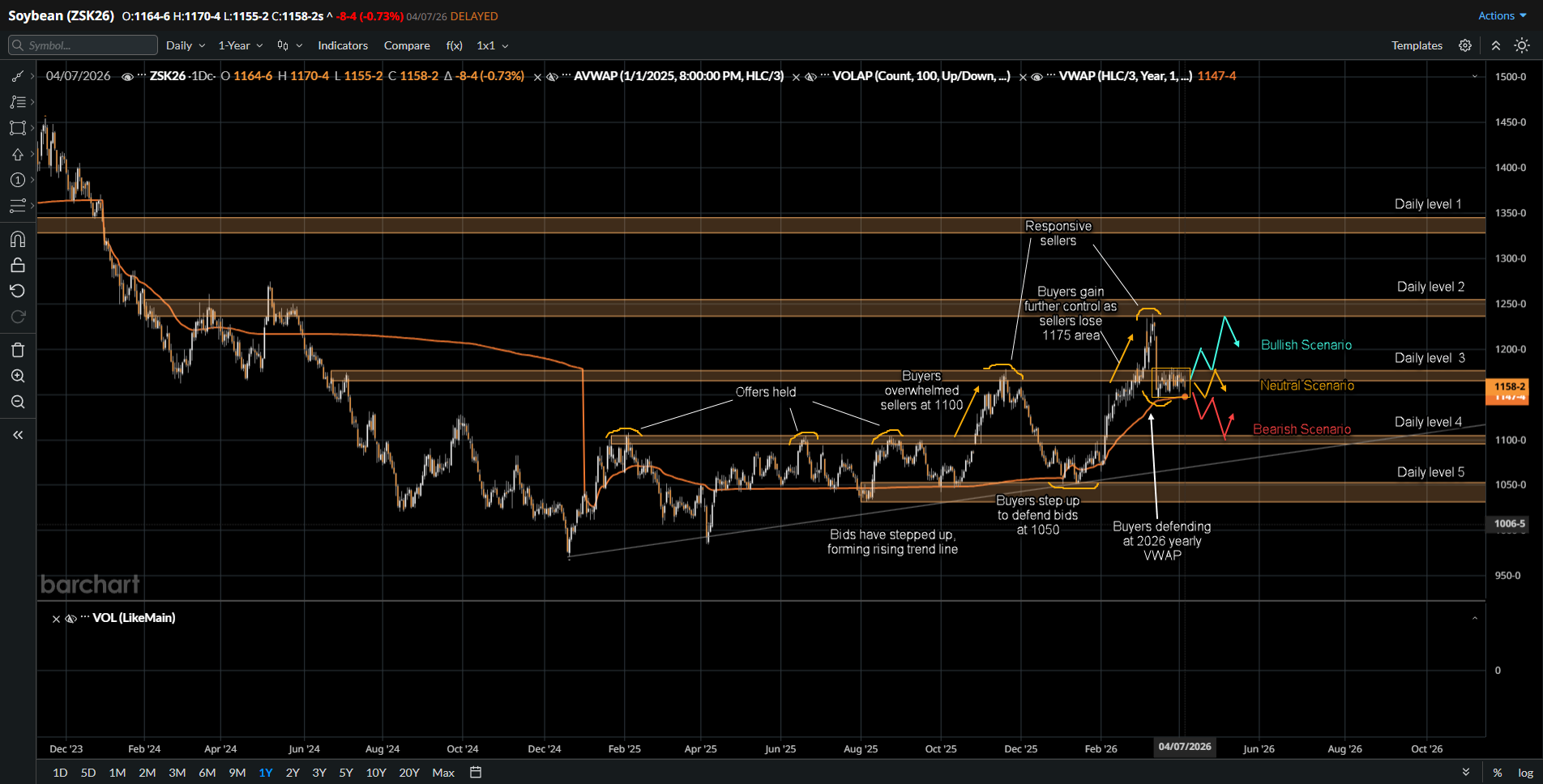

- Since the start of 2025, the market has been structurally supported to the upside, with buyers consistently responding and stepping up bids after each rotation lower. The most recent rotation down in January found strong buying support at 1053 (Daily Level 5), establishing a clear base from which the market rebuilt.

- In February, price grinded higher, eventually reaching 1171 (Daily Level 3) where sellers attempted to defend. Buyers ultimately overwhelmed that resistance, and price expanded higher into March, reaching the 1240 area (Daily Level 2).

- At 1240, sellers responded aggressively. On March 16, May soybeans closed at 1155-1, down 70 cents on the session, one of the largest single-day declines of the year. The catalyst was President Trump's statement that a summit with Chinese President Xi Jinping could be delayed if Beijing did not help unblock the Strait of Hormuz, which brought China demand risk sharply back into focus for the market.

- Following that selloff, price rotated back below 1240 and has since settled in the vicinity of the 2026 VWAP near 1147.

- In the past few weeks, the market has been trading in a tight range between 1240 and 1147, with neither buyers nor sellers able to establish clear control as the market waits for a macro catalyst.

What to Expect in the Coming Weeks

The key level to watch is the 1179 area (Daily Level 3).

Bullish Scenario

- If buyers are able to break and accept above the current tight range, expect the market to move up to repair the March 16 single prints and low volume areas, and subsequently advance toward 1229 (Daily Level 2), where sellers are expected to respond.

- The possible macro trigger for this scenario would be confirmation that the Trump-Xi summit proceeds as planned, with China committing to increased purchases of U.S. agricultural goods. A formal de-escalation in the Strait of Hormuz or a positive shift in EPA biofuel blending mandates could provide additional fuel to push price through the range highs.

Neutral Scenario

- If no new macro catalyst materializes, the market is likely to remain in two-way rotation within the tight range between 1240 and 1147, as buyers and sellers continue to test each other's resolve without resolution.

- This scenario becomes more probable if U.S.-China dialogue remains in a holding pattern and if the USDA's May WASDE offers no significant revisions to the soybean supply and demand balance sheet.

Bearish Scenario

- If buyers are not able to hold bids at the 1147 area (2026 VWAP), expect a move down to 1100 (Daily Level 4), where buyers are expected to respond.

- The possible macro trigger here would be a breakdown in the U.S.-China trade talks, a confirmation that the Trump-Xi summit has been postponed indefinitely, or a sharper-than-expected acceleration in Brazilian harvest pace that relieves tightness and allows China to continue sourcing away from U.S. supplies.

Conclusion

Soybean futures sit at a technically and fundamentally significant juncture. The structure of the market since early 2025 has been decidedly bullish, with buyers absorbing each rotation lower and driving price higher over time. However, the aggressive seller response at 1240 and the subsequent tight consolidation against the 2026 VWAP reflect a market that has reached a genuine inflection point. Macro fundamentals remain a double-edged sword: the biofuel demand story and a below-expected Prospective Plantings print are supportive, while lagging export commitments running 19% below last year and the fragile U.S.-China diplomatic backdrop introduce meaningful downside risk. Whether this market breaks higher to repair the March 16 damage or cracks below VWAP support will likely be determined by what happens in the coming weeks between Washington and Beijing. If you are trading or watching this market, the 1179 level is where the battle begins.

If you are looking for evergreen technical content and robust market updates, our blog series on Barchart is the essential resource for your workflow. Combine professional-grade insights with a high-performance futures trading platform to ensure every decision is backed by data-driven confidence. Ready to elevate your execution? Open an Account now.

Disclaimer:

This article is provided for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis presented reflects the author’s market observations and opinions at the time of writing and is not a recommendation to buy or sell any futures contract, security, or financial instrument. Futures trading involves significant risk and is not suitable for all market participants. Losses may exceed initial margin deposits, and market conditions can change rapidly.

Any scenarios, levels, or market expectations discussed are hypothetical in nature and are intended solely to illustrate potential market behavior. They do not represent actual trading results and should not be interpreted as guarantees of future performance. Past performance, market behavior, or historical price action are not indicative of future outcomes.

Readers are solely responsible for their own trading decisions and risk management. Always conduct independent research, consider your financial situation and risk tolerance, and consult with a qualified financial professional, if necessary, before engaging in futures or derivatives trading.

/Broadcom%20Inc%20logo%20on%20phone%20and%20site-by%20Majahid%20Mottakin%20via%20Shutterstock.jpg)

/CPU%20Chip.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)