The past six months have been a windfall for MongoDB’s shareholders. The company’s stock price has jumped 71.7%, hitting $345.05 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is it too late to buy MDB? Find out in our full research report, it’s free.

Why Does MDB Stock Spark Debate?

Named after "humongous database," reflecting its ability to handle massive data loads, MongoDB (NASDAQ:MDB) provides a flexible document-based database platform that helps developers build, deploy, and maintain modern applications more efficiently.

Two Positive Attributes:

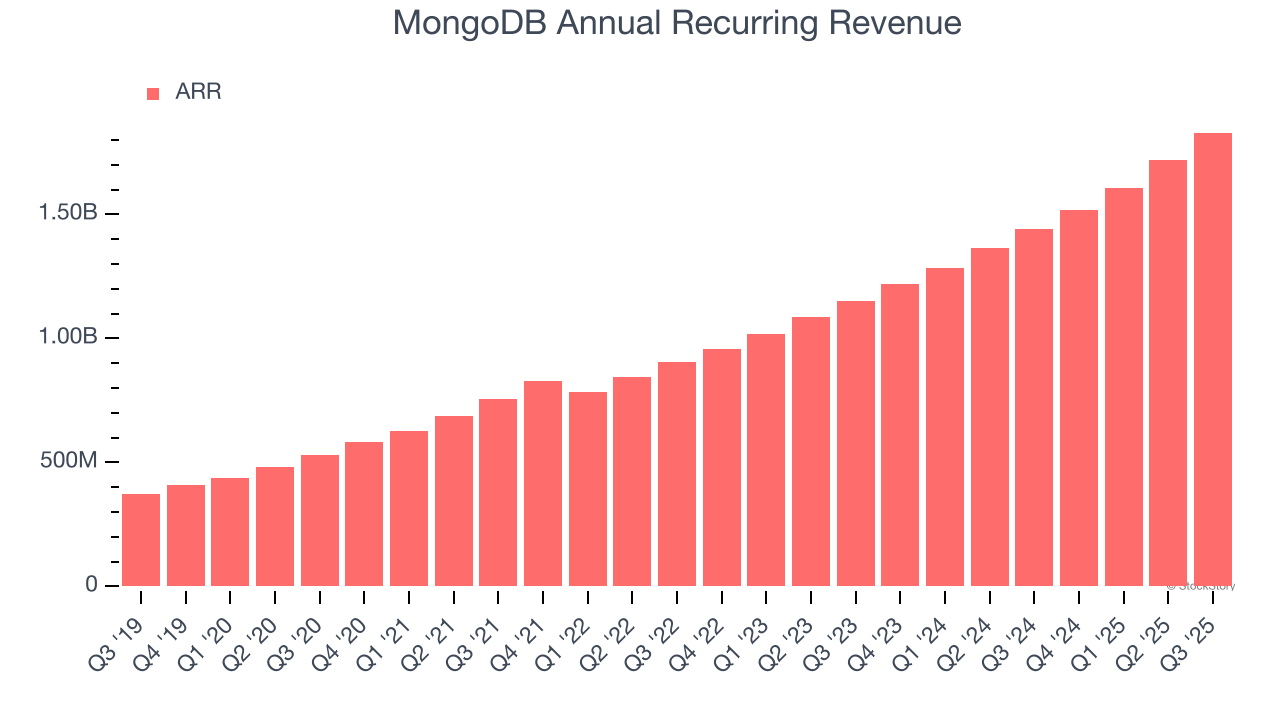

1. ARR Surges as Recurring Revenue Flows In

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

MongoDB’s ARR punched in at $1.83 billion in Q3, and over the last four quarters, its year-on-year growth averaged 25.6%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes MongoDB a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect MongoDB’s revenue to rise by 19.9%, close to its 33.7% annualized growth for the past five years. This projection is commendable and indicates the market is forecasting success for its products and services.

One Reason to be Careful:

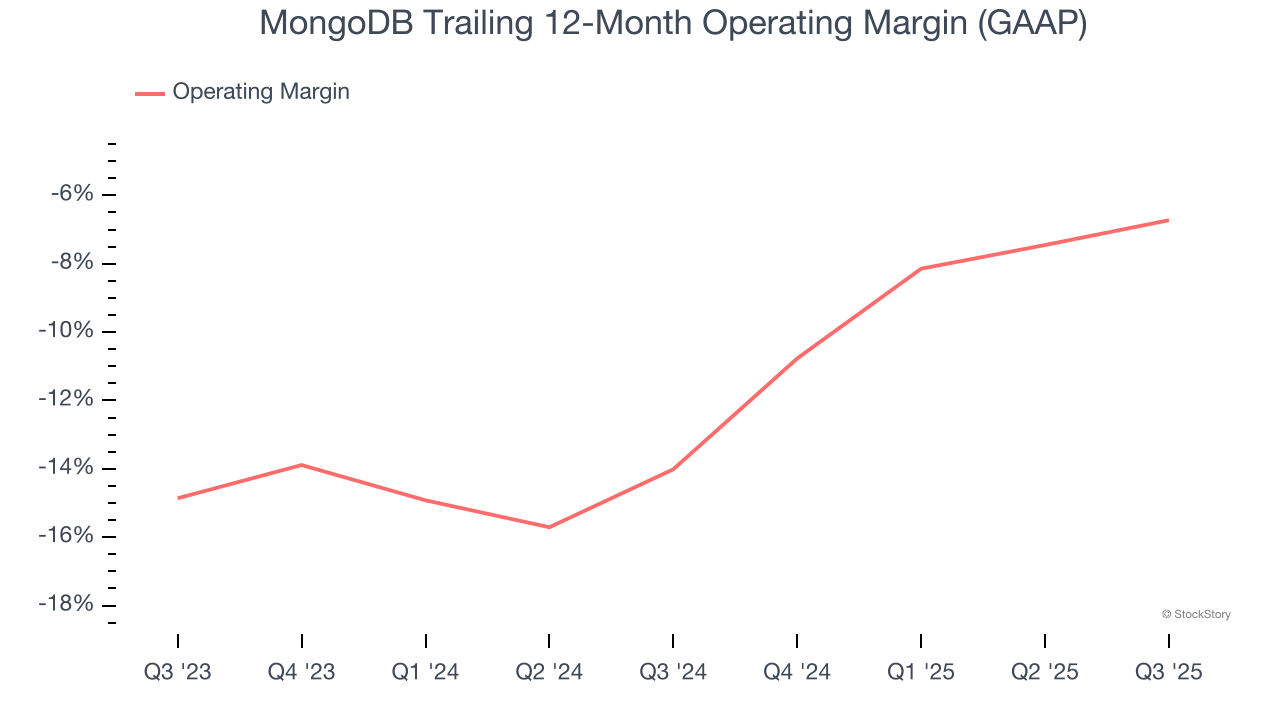

Operating Losses Sound the Alarms

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

MongoDB’s expensive cost structure has contributed to an average operating margin of negative 6.7% over the last year. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

Final Judgment

MongoDB’s positive characteristics outweigh the negatives, and with the recent rally, the stock trades at 9.6× forward price-to-sales (or $345.05 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than MongoDB

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)