Artificial intelligence (AI) has been doing more than powering chatbots and cloud software. It is also starting to reshape industries that still depend on freight, logistics, and long-haul trucking. That is one reason investors have been watching Ark Invest so closely lately, as Cathie Wood keeps leaning into AI names tied to real-world automation.

One of the latest moves was a sizable purchase of Kodiak AI (KDK), with Wood's Ark Autonomous Tech & Robotics ETF (ARKQ) adding about 230,000 shares. Kodiak is working on autonomous trucking and AI-driven logistics, a combination that could make it one of the more interesting early-stage bets in the automation race.

For investors looking for the next AI stock with long-term upside beyond the usual mega-cap names, Kodiak AI now deserves a closer look.

About Kodiak Stock

Based in Mountain View, Kodiak AI builds the “Kodiak Driver,” a self-driving system for long-haul trucks. The startup works mainly with commercial freight customers, developing fully driverless trucking routes and hardware.

Kodiak went public in late 2023 via a SPAC and remains pre-profit. The company has no consumer business as it sells “Driver-as-a-Service” (DaaS) to logistics partners, leveraging alliances, e.g., with Bosch and Nvidia (NVDA), to scale. Kodiak wants to be to big rigs what Waymo is to taxis, aiming for safer, cheaper freight transport in the years ahead.

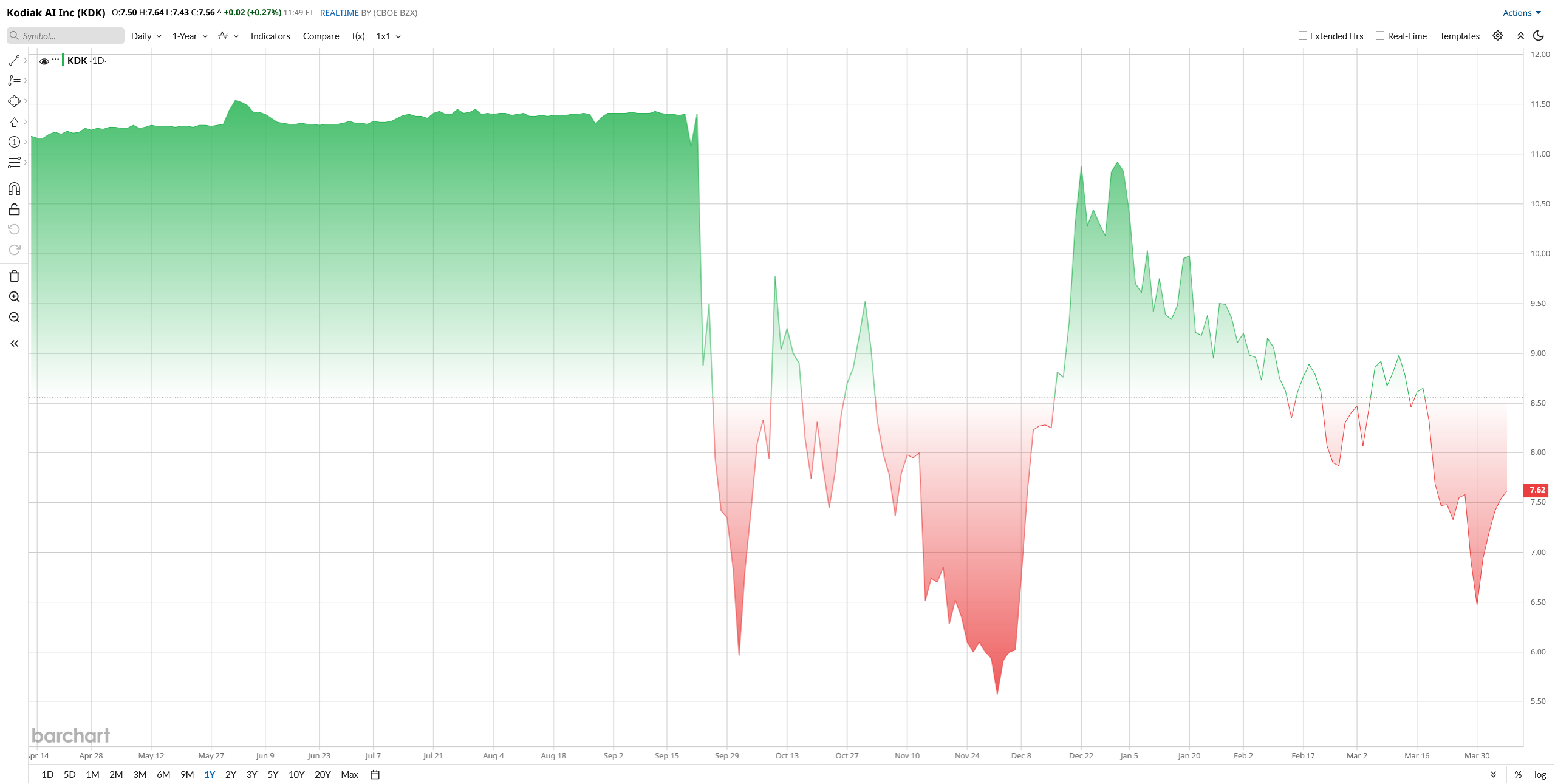

Valued at a small cap of $1.35 billion, the share price of Kodak has swung dramatically. After the IPO, KDK stock climbed into double digits, peaking a little over $11 per share in late 2025. However, by April 2026, it’s nearer $7.4, about a 32% drop year to date (YTD).

The fall comes amid investor jitters about high R&D costs, growing losses, and no steady revenue yet. Technically, the stock is in a downtrend. Barchart’s technical rating shows an 88% Sell signal for KDK, and traders see Kodiak’s chart as weak; it’s well below its recent moving averages and trendlines.

Along with other challenges, Kodiak also looks very expensive. Its price/sales ratio is around 173×, while the industry median is only 116×. Similarly, its EV/revenue is about 315× versus 113× for peers. It means investors are paying huge multiples, basically betting on explosive future growth. It’s worth noting the flip side: high multiples also imply that any stumble could hurt the stock badly, since expectations are so steep.

Cathie Wood’s Big Bet

On April 6, news broke that Cathie Wood’s ARKQ fund snapped up 230,000 shares of Kodiak AI. This is a multi-million-dollar stake at $7.5 per share, which is worth a total of $1.73 million

ARKQ usually focuses on advanced tech, so the buy is a clear vote of confidence in self-driving freight. Investors saw the move as validation. Wood’s team believes Kodiak’s autonomous trucks are the future of logistics. However, traders know ARK’s moves are long-term plays.

In effect, Wood’s purchase also shows her high conviction thesis that driverless trucking will dramatically cut costs in supply chains. In the near term, it doesn’t make Kodiak profitable overnight, but it does shine a brighter light on Kodiak’s tech at a time when many growth stocks are out of favour.

Revenue Growth Accelerates From a Small Base

Kodiak’s most recent quarter, which was Q4, showed notable progress. Revenue was $1.1 million, up 37% from Q3. Granted, that’s still a tiny number on a GAAP basis, but it’s accelerating. All the revenue comes from its logistics partners.

Net losses, however, were much larger, as Kodiak lost about $73.7 million in the quarter versus $14.4 million a year earlier. Non-GAAP EPS remains deep in the red. The company reported a negative free cash flow of $34 million in Q4. Importantly, Kodiak ended the quarter with about $120.7 million in cash and equivalents, so it has runway to expand.

CEO Don Burnette highlighted milestones on the earnings call. He called 2025 “a transformational year,” growing deployments from two to 20 trucks and securing key partnerships. Burnette noted Kodiak now has its own fully driverless routes: one with Martin Brower and another with a Fortune 500 fleet, Dallas-Houston. These pilots bring the total operational lanes to eight.

CFO Surajit Datta echoed optimism: “We grew revenue 37%… outperformed our guidance… and remain focused on achieving profitability and positive cash flow over time,” he said. He also explained Kodiak refinanced $30 million of debt, improving liquidity, and is scaling its asset-light model. Analysts expect revenue to creep up slowly through 2026, while losses should narrow as the driverless program expands.

What Do Analysts Think of KDK Stock?

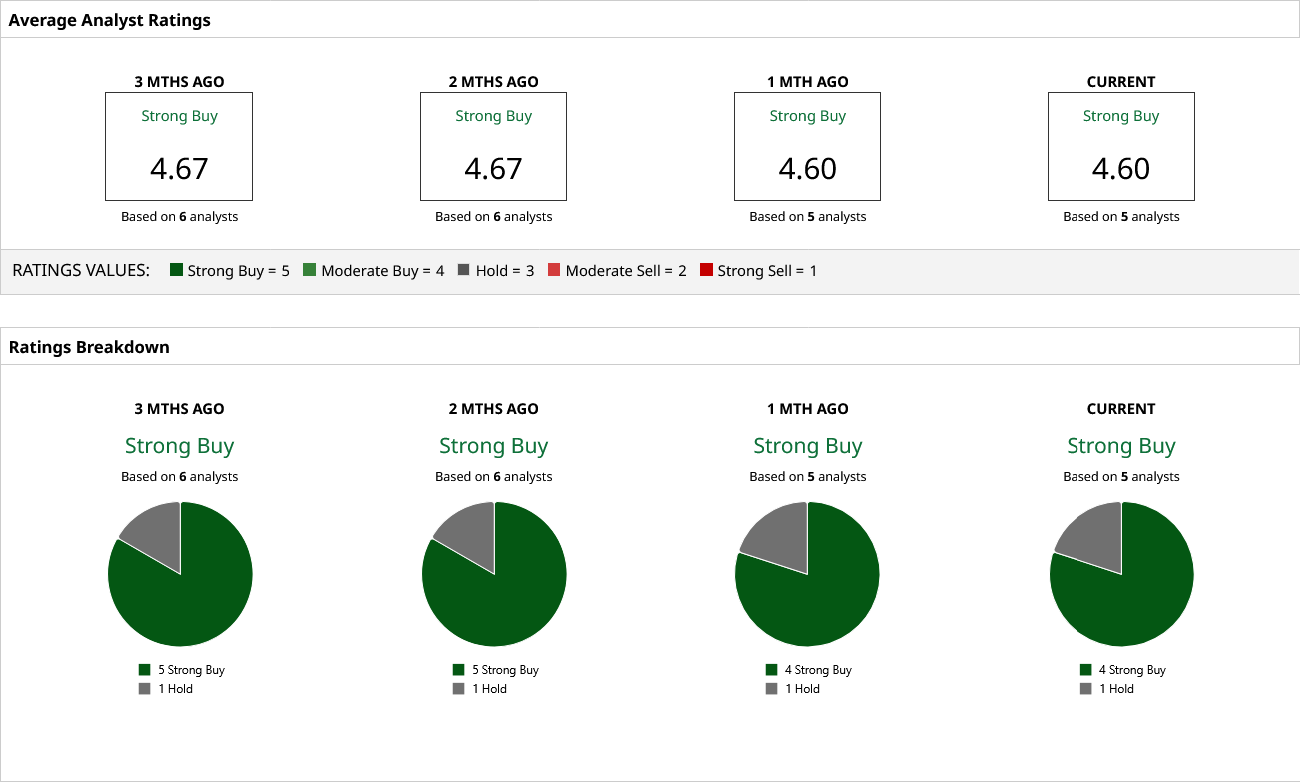

Wall Street's opinion on KDK stock is mostly optimistic. According to Barchart, the consensus rating is “Strong Buy,” reflecting four “Strong Buy” calls and one “Hold” out of five analysts in the past year. The average 12-month price target is $16.25, more than double the current stock price. The highest reported target is around $22, while the lowest is near $13.

Overall, analysts appear to be value-adding to the idea of robust growth, as their mean forecast suggests growth of more than 100%. Naturally, a lot of the latter will depend on whether Kodiak will be able to deliver on its ambitious roadmap. Kodiak and its competitors Pony.ai and WeRide are also still loss-making, but with some double-digit revenue growth and Tier-1 partners landing, which is the basis of those optimistic opinions. Yet it implies that any failure in execution would result in negative revisions.

To conclude, the Street has a juicy potential with huge risk: the consensus set by Kodiak is an investor in the success of the driverless rollout and not certain earnings in the near future.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)