Insider buying and selling can offer a useful glimpse into how executives view their own companies. While one trade does not make a trend, a big sale from a top insider often gets investors’ attention, especially when the stock has already had a strong run.

That is precisely what happened with Marvell Technology (MRVL). According to a recent filing, EVP and Chief Legal Officer Mark Casper sold 17,854 shares for about $1.89 million, cutting his stake by roughly 46%. It was one of the week’s biggest insider transactions, but the market barely blinked. MRVL shares were essentially flat in the following session.

The sale does not automatically mean trouble ahead, but it does raise an obvious question for shareholders. After a sharp insider sale, is MRVL still a stock worth holding, or is it time to think about trimming exposure?

Marvell Doubling Down on AI and Infrastructure Growth

Marvell Technology designs chips that power networks, data centers, 5G infrastructure, and storage devices. In the past couple of months, the company made several strategic moves to bolster its AI/5G roadmap. For instance, in January 2026, it announced a deal to acquire XConn Technologies, a startup with advanced PCIe and CXL switch chips. CEO Matt Murphy said this “adds proven PCIe and CXL switch products” and talent to Marvell’s team, furthering its AI connectivity strategy.

Also, Marvell is buying Celestial AI for its breakthrough optical interconnect technology. This optical fabric is aimed at ultra-low latency AI networks.

Taken together, plus the huge Nvidia (NVDA) investment announcement, Marvell is clearly doubling down on AI data center infrastructure. Marvell now claims broad-scale partnerships for 5G and AI, which should translate into more design wins and revenue over time.

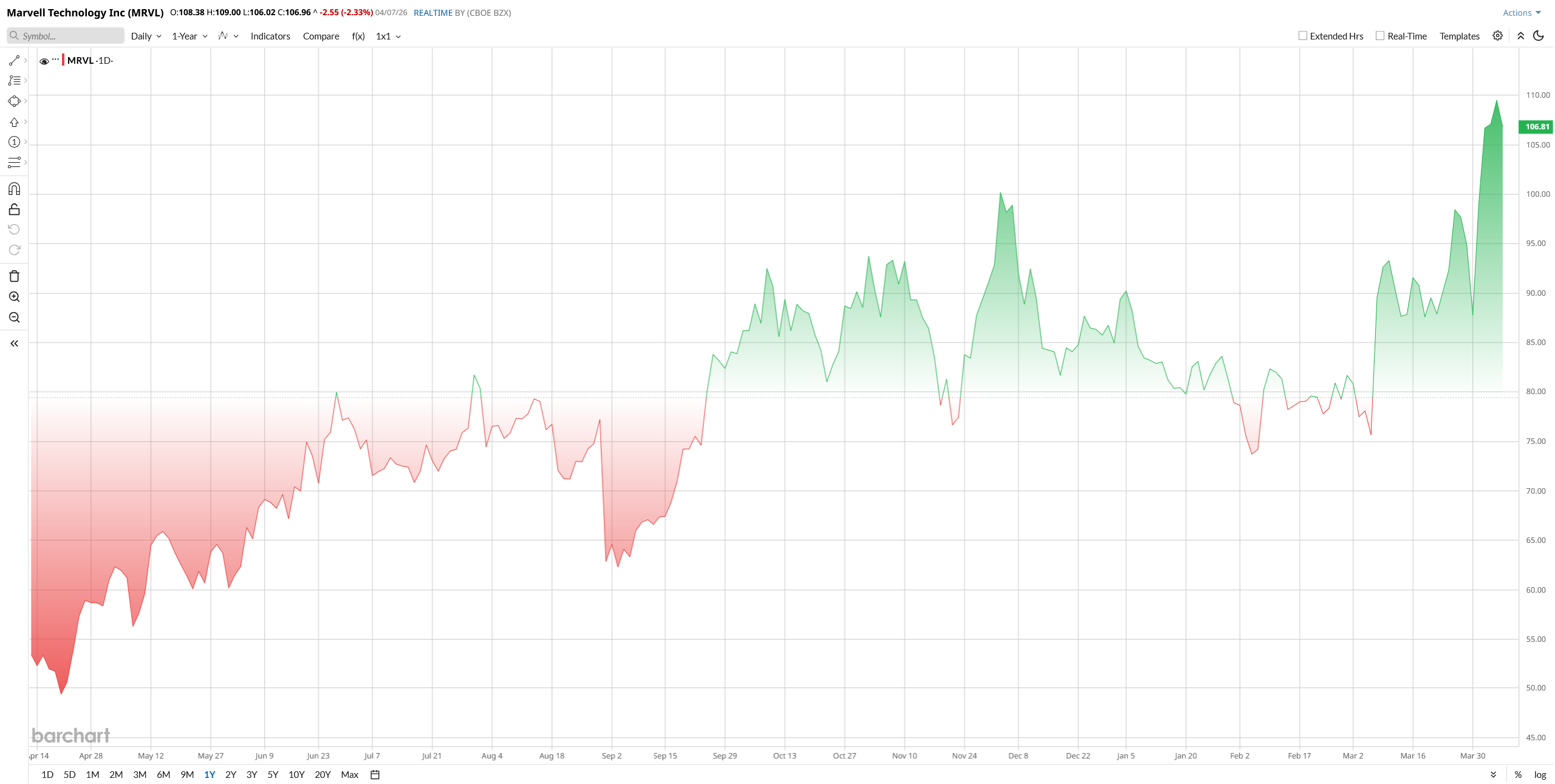

MRVL stock has enjoyed a strong run over the year. The shares rallied on AI and Nvidia partnership news, hitting a 52-week high of about $102 in early 2026. Over 12 months, MRVL has more than doubled, and year-to-date (YTD) the stock has gained more than 24%, much above the broader market index.

Technically, Marvell “rallied past its 20-day moving average” in late March, a bullish breakout indicator. Also, it’s trading comfortably above its 50-day and 200-day moving averages.

Marvell isn’t trading like a frothy tech stock. Its valuation is roughly in line with peers. The forward P/E is in the mid-30s, slightly below the semiconductor industry median of around 38×. Similarly, Marvell’s EV/EBITDA sits near 21× trailing twelve months, just under the 22× industry median. On those metrics, MRVL appears fairly valued, neither deeply discounted nor extremely rich compared to fellow chipmakers.

Marvell Beats Q4 Earnings Estimate

Marvell Technology delivered a strong Q4 quarterly performance, highlighting the company’s growing exposure to AI-driven demand. For Q4, revenue came in at $2.22 billion, up 22% year-over-year (YoY). The data center segment remained the primary growth engine, generating about $1.7 billion in revenue, while communications and storage contributed roughly $567 million, both showing solid double-digit gains.

Profitability also improved. Non-GAAP gross margin reached about 58%, supporting earnings growth. Net income reached $396.1 million, and adjusted earnings came in at $0.80 per share, marking a 33% increase from the prior year.

Notably, the company surpassed both top- and bottom-line analysts' estimates by healthy margins in this quarter.

The balance sheet also showed strong progress. The company generated $373.7 million in operating cash flow, translating into approximately $259 million in free cash flow after capital expenditures. Marvell ended the quarter with $2.7 billion in cash, reinforcing its balance sheet strength.

Looking ahead, management expects continued momentum. Marvell guided for Q1 FY2027 revenue of around $2.4 billion, with adjusted EPS close to $0.79. The company also sees strong growth continuing into 2027, supported by rising AI-related demand and increasing data center investments.

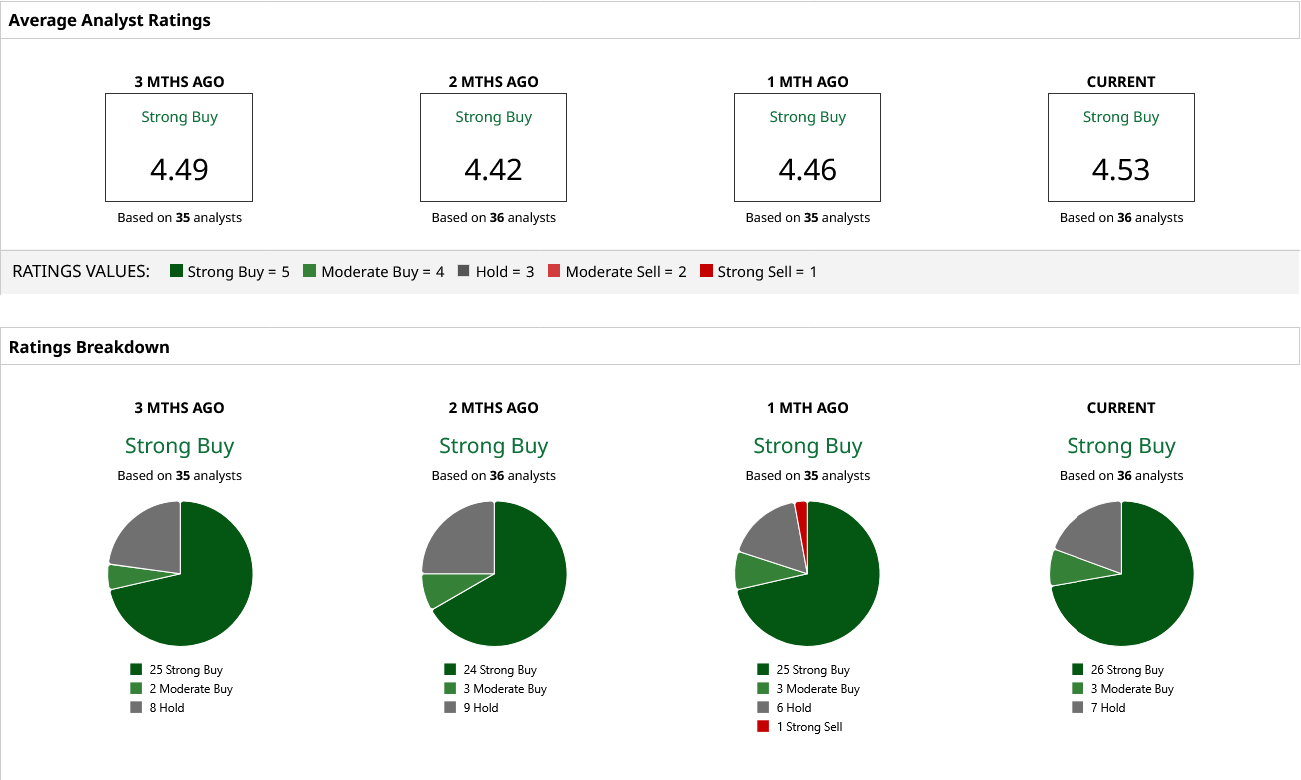

Wall Street's Take on MRVL Stock

Wall Street remains largely positive on MRVL stock. The consensus “Strong Buy” rating and $120.59 mean target price imply about 20% upside from current levels.

Separately, Morgan Stanley cut its target to $95 from $112 and kept an “Equal Weight” rating, noting that Marvell’s demand is solid but high expectations are already baked in.

On the bullish side, Goldman Sachs bumped its MRVL target to $100 from $90, maintaining a “Neutral” view. GS analyst James Schneider said Marvell’s strong Q1 outlook and data center ramp justified a higher target.

Likewise, RBC Capital reiterated its “Outperform” rating and a $115 target after the Nvidia news. RBC said the Nvidia investment “validates Marvell’s connectivity leadership and custom silicon capabilities”.

Lastly, Bank of America lifted its target to $125, specifically citing the Nvidia partnership’s benefits. Stifel kept a “Buy” with a $120 target, and KeyBanc reaffirmed “Overweight” at a $130 target.

Given this, most analysts still find MRVL’s long-term growth story intact, despite one insider’s recent share sale.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)