/Palo%20Alto%20Networks%20Inc%20HQ%20sign-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

In a world now running on data, where artificial intelligence (AI) models write code, answer questions, and power entire businesses, cybersecurity has quietly become the backbone holding it all together. That is where Palo Alto Networks (PANW) steps in. What began as a firewall company has evolved into a full-stack security giant, protecting cloud networks, enterprises, and increasingly, AI-driven infrastructure. As data grows rapidly and cyber threats become more advanced, Palo Alto has kept pace, evolving into a key player and a core holding in the cybersecurity space.

Naturally, as AI leaders like OpenAI with ChatGPT and Anthropic with Claude rise, some worry they could disrupt traditional cybersecurity by detecting threats on their own. It’s a fear similar to how AI coding tools shook the software space. But Benchmark analyst Yi Fu Lee believes these concerns are overblown and not a real threat.

In fact, as he recently initiated coverage on PANW stock, he struck a confident tone. He sees a clear path for the company’s next-gen security revenue to more than double in the coming years. Even more interesting, his projections don’t fully factor in AI and quantum security upside yet.

Although PANW stock has slipped back to yearly lows amid AI disruption fears and slowing organic growth, analysts remain confident. The bull case is far from broken and still very much in play. So, let’s take a closer look at the cybersecurity stock.

About Palo Alto Stock

Based in Santa Clara, California, Palo Alto Networks has grown into one of the biggest names in cybersecurity, with a market capitalization of $133.2 billion. It has expanded into a full platform that helps companies protect their networks, cloud systems, and data. Today, the company offers AI-driven security tools, real-time threat detection, and cloud protection, helping businesses manage risks across hybrid environments. Its platform approach brings multiple security solutions together, making things simpler and more efficient.

Backed by Unit 42 threat intelligence and used by over 70,000 customers worldwide, Palo Alto is focused on helping companies move toward Zero Trust security. With its Precision AI and strong innovation push, it continues to play a key role in securing the digital world.

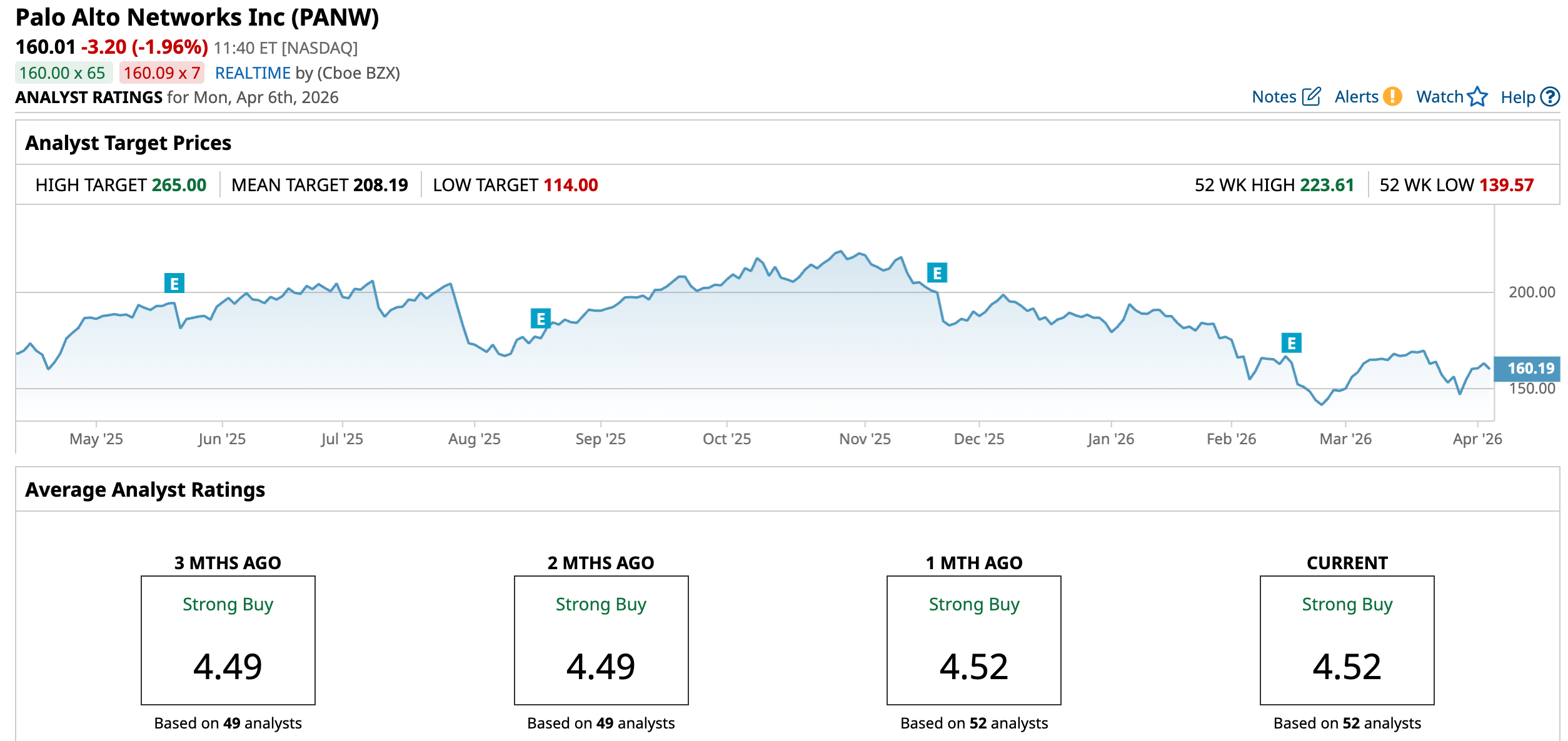

The mood around PANW stock has been a bit of a rollercoaster lately. As the AI conversation moved from optimism to concern, investors began questioning how much disruption lies ahead, even for strong players. That shift pushed PANW down nearly 27% from its 52-week high of $223.61, with the stock hitting a low of $139.57 in late February.

Zooming out, the stock is down 4.46% over the past year and has fallen 12.9% on a year-to-date (YTD) basis. But the recent trend tells a slightly different story. Over the past five days, PANW has climbed 4.4%. A major confidence boost came when CEO Nikesh Arora bought $10 million worth of shares, signaling confidence in the company’s strength.

Technically, the 14-day RSI has bounced back from February’s oversold levels to 49.4, suggesting momentum has improved. However, the MACD oscillator is flashing caution. The MACD line has slipped below the signal line, and the histogram remains in negative territory, indicating weakening momentum and a possible near-term downside risk.

Valuation-wise, PANW still looks on the expensive side, trading at around 44.2 times non-GAAP forward adjusted earnings and 11.7 times sales, both higher than sector averages. That said, the stock is actually cheaper than its own historical levels, suggesting some cooling off despite the premium tag.

A Closer Look at Palo Alto Networks’ Better-Than-Expected Q2 Numbers

Palo Alto Networks reported its fiscal second-quarter results on Feb. 17 for the quarter ended Jan. 31, and it felt like a company balancing between steady execution today, while building something for a much bigger tomorrow. The company generated a revenue of $2.6 billion, up nearly 15% year-over-year (YOY), just edging past expectations. Most of this growth came from its subscription and services business, which continues to be the backbone of its platform strategy.

Profitability also held firm, with non-GAAP operating margins expanding from 28.4% last year to 30.3%, while non-GAAP EPS jumped over 27.2% annually to $1.03, comfortably beating estimates.

Meanwhile, its next-generation security ARR surged 33% YOY to $6.3 billion, while remaining performance obligations (RPO) climbed 23% annually to $16 billion – clear signs that future revenue pipelines remain strong.

Additionally, the company remains in a strong financial position. As of Jan. 31, it held $4.54 billion in cash and cash equivalents and short-term investments. It also generated $3.75 billion in adjusted free cash flow, highlighting its ability to bring in solid cash even while investing for growth.

And Palo Alto Networks is investing aggressively. In February, moved into identity security with the acquisition of CyberArk, aiming to secure everything from human users to machine and AI-driven identities. And, the firm is preparing to acquire Koi, doubling down on the evolving endpoint landscape where AI agents are becoming new attack surfaces.

Looking ahead, management remains confident. Revenue for Q3 is expected to be between $2.941 billion and $2.945 billion, representing an annual growth between 28% and 29%, while non-GAAP EPS is anticipated to be somewhere between $0.78 and $0.80. Next-gen Security ARR for Q3 is estimated to range between $7.94 billion and $7.96 billion, up by around 56% annually.

For fiscal 2026, Next-Gen Security ARR is expected to be between $8.52 billion and $8.62 billion, growing over 50% annually. Revenue is projected between $11.28 billion and $11.31 billion, with RPO rising to around $20.2 billion to $20.3 billion. However, all the expansion comes at a cost, as the company lowered its fiscal 2026 EPS forecast to $3.65 to $3.70.

Analysts, meanwhile, expect EPS around $2.14, up 30.5% YOY for fiscal 2026, and then rise by another 7% annually to $2.29 in fiscal 2027.

What Do Analysts Expect for Palo Alto Networks Stock?

Benchmark’s Yi Fu Lee believes that Palo Alto is not just another cybersecurity stock, but a company that can grow steadily over the long run. He gave it a “Buy” rating and set a $200 price target, showing strong confidence despite recent concerns around the stock.

What’s driving this optimism is Palo Alto’s Next-Gen Security (NGS) business, which he believes offers strong visibility for growth. Lee expects NGS ARR to more than double, from about $8.6 billion by fiscal 2026 to nearly $20 billion by 2030.

Even more compelling, he highlights that NGS is already expanding rapidly, growing 32.4% YOY to $6.33 billion, holding its ground even against high-growth peers. And importantly, his projections do not fully factor in emerging tailwinds like AI and quantum security. In the analyst’s view, the runway is long, execution is strong, and the upside may still be underestimated.

Overall, sentiment on PANW remains firmly bullish, with the stock’s consensus rating at “Strong Buy.” Out of 52 analysts, 38 recommend a “Strong Buy,” three have a “Moderate Buy,” and the remaining 11 are giving it a “Hold” rating.

Its average price target of $208.19 implies upside potential of 30%. Meanwhile, the Street-high target of $265 suggests PANW stock could rise as much as 65.6% from the current price levels.

Final Thoughts on PANW

The talk around AI replacing cybersecurity has not really changed the bigger picture for Palo Alto Networks. While concerns have grown, especially after reports around advanced models from Anthropic, the reality is more balanced. Yes, AI may take on some security tasks, but it also creates new risks that need stronger protection.

Palo Alto’s platformization strategy – bringing multiple security tools into one unified system – still gives it an edge, along with a steady pipeline and expansion into newer areas. Even with some AI players in the spotlight, the need for dedicated cybersecurity platforms remains strong.

That is why some analysts remain positive. The bull case for PANW is not going away, and it’s simply adjusting to a changing tech landscape.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)