/RTX%20Corp%20website%20on%20phone%20and%20logo-by%20T_Schneider%20via%20Shutterstock.jpg)

RTX Corp. (RTX), parent of defense companies Raytheon, Collins, Pratt & Whitney, may have reached a short-term peak. But shorting out-of-the-money (OTM) puts may be a good play. Investors can make a 1.5% yield over the next month at a 10% lower exercise price. This article will discuss that play.

RTX stock closed at $196.21 last week, off its recent peak of $212.16 on March 2, but up from a recent trough of $187.15 on March 30. It may be jumping around with every move in the Iran war.

As a result, option premiums are very high. I pointed this out in my Barchart article three weeks ago on March 9, “Defense Stocks Like RTX Corp Look Attractive to Value Investors and OTM Option Plays.”

Shorting RTX Covered Calls

I suggested shorting covered calls expiring April 10 when RTX was at $209.28. The $220.00 call options premium was $4.18 per call contract. So, an investor would have yielded 2.0% (i.e., $4.18/$209.28 = 0.01997 or 0.02).

As of last week, the $220 call price had slid to 18 cents, so a watchful investor can close this contract out by entering an order to “Buy to Close.”

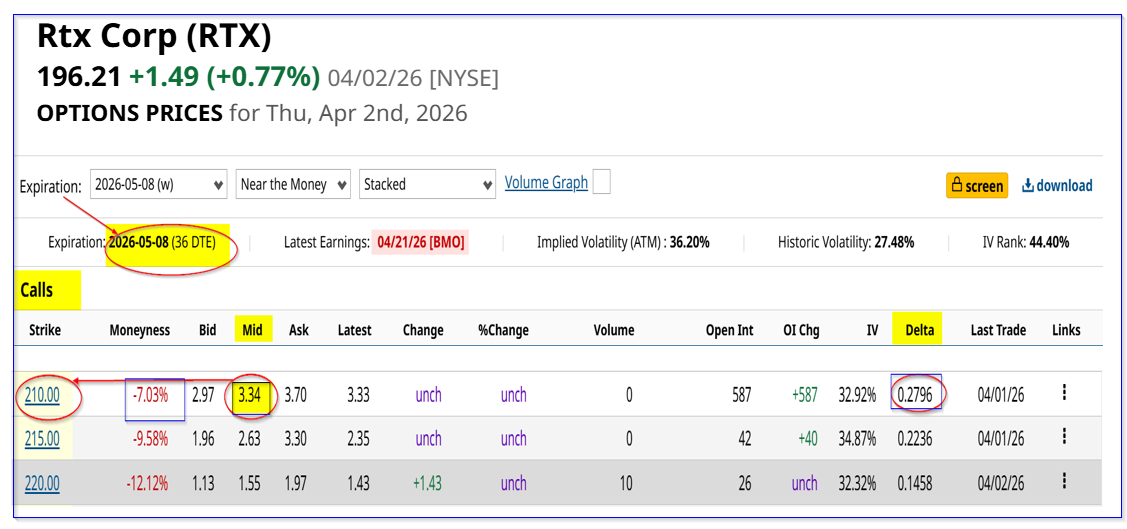

It might make sense to do a new covered call play. For example, the May 8 expiry period shows that the $220.00 strike price call has a midpoint premium of $1.55. So, the covered call yield is less than 1.0%:

$1.55 / $196.21 = -.00789 = 0.8% yield

Lowering the covered call strike price to $210, 7% higher than last week's close, raises the yield to 1.70% (i.e., $3.34/$196.21):

However, I suggest that investors wait before doing this covered call play. A more interesting, and potentially safer play is to sell out-of-the-money (OTM) puts.

Shorting OTM RTX Puts

I discussed this play in my last Barchart article on March 9. I discussed shorting $195.00 strike price puts expiring April 10 for $3.47. That yielded 1.78% immediately (i.e., $3.47/$195.00).

Now that RTX has fallen to $196, the put premium is only slightly lower at $2.92. So, it makes sense to roll this trade over to May 8. That means buying back the April 10 expiry put contract and entering a new “Sell to Open” put for expiry on May 8.

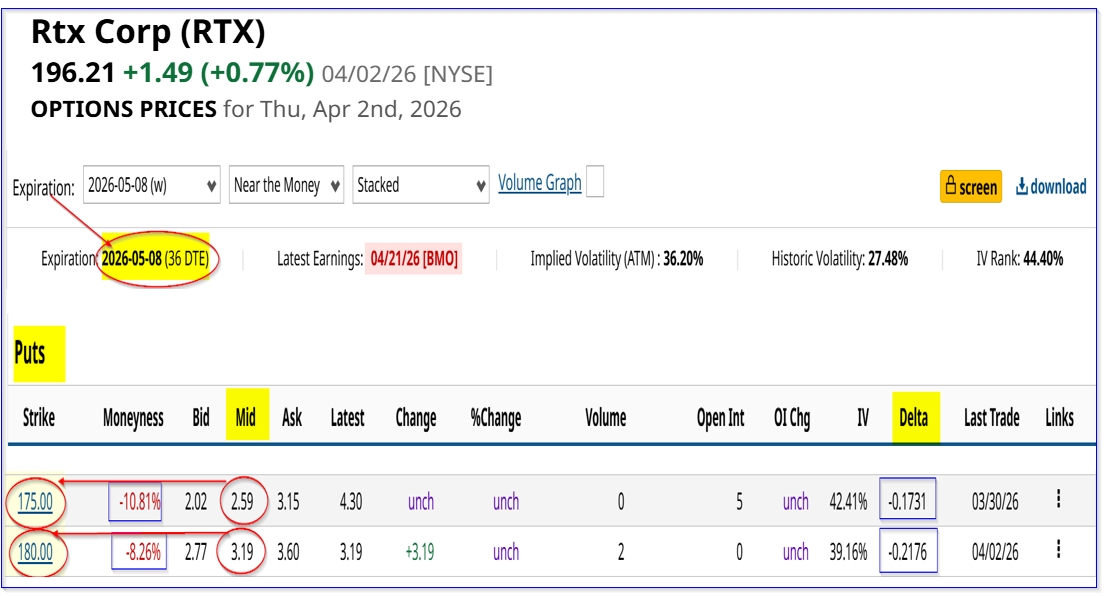

For example, the $175.00 put option strike price expiring May 8 has a midpoint premium of $2.59. This strike price is 10.8% lower than last week's close.

The mid-point premium provides an immediate yield of almost 1.5% (i.e., $2.59/$175.00).

This is a worthwhile play since RTX would have to fall to $172.41 (i.e., $175.00 - $2.59) before an investor's buy-in at $175.00 would result in an unrealized loss. That is 12% lower than last week's close.

The point is that this provides an attractive potential buy-in point for new investors in RTX Corp. Moreover, the investor could repeat this trade each month and then accumulate monthly short-put income.

For less risk-averse investors, shorting the $180 put contract provides a higher yield: $3.19 / $180.00 = 0.177 = 1.77%. The breakeven point is $176.81 is still $20 lower, or -10% below last week's close.

Short-Put Yields vs. Short-Call Yields

As a result, this trade is very attractive to value investors, given the higher monthly yields compared to short call plays.

For example, I showed above that a one-month 7% OTM covered call has a 1.70% yield, whereas an 8% OTM put has a 1.77% short-put yield.

That is why I suggest shorting an OTM put now and then, if RTX stock rises from here, doing a new covered call OTM short call RTX play.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.