/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Global GPU demand is exploding as artificial intelligence shifts from niche experiments to everyday infrastructure, with GPU as a service projected to surpass $50 billion by decade’s end. This growth is forcing data centers to rethink how compute, memory, and networking are stitched together so AI workloads can scale efficiently instead of getting choked by bottlenecks. The real challenge is designing connective technology that lets every piece of silicon in the rack work as one coherent system.

Nvidia’s (NVDA) new $2 billion partnership with Marvell Technology (MRVL) drops right into that transition, and Wedbush says the real focus is NVLink Fusion, not just another AI hardware deal. NVLink Fusion is Nvidia’s new rack-scale interconnect technology. It lets companies build their own custom AI systems that plug straight into Nvidia’s GPU ecosystem without any major complications.

Under the deal, Marvell will design custom processing chips and high-speed networking that work directly with NVLink Fusion. Marvell’s CXL switches and 260-lane PCIe 6.0 switches become natural anchors for NVLink Fusion fabrics.

This interconnect technology is being framed as the fabric that could quietly determine whose AI architectures scale best as GPU clouds, custom accelerators, and advanced memory systems spread across data centers. The key question now is how far NVLink Fusion can go in reshaping that shared roadmap.

How NVLink Fusion Fits Nvidia

Nvidia is a $4.27 trillion semiconductor and AI computing company based in Santa Clara, California, designing chips and platforms for data centers, gaming, and industry.

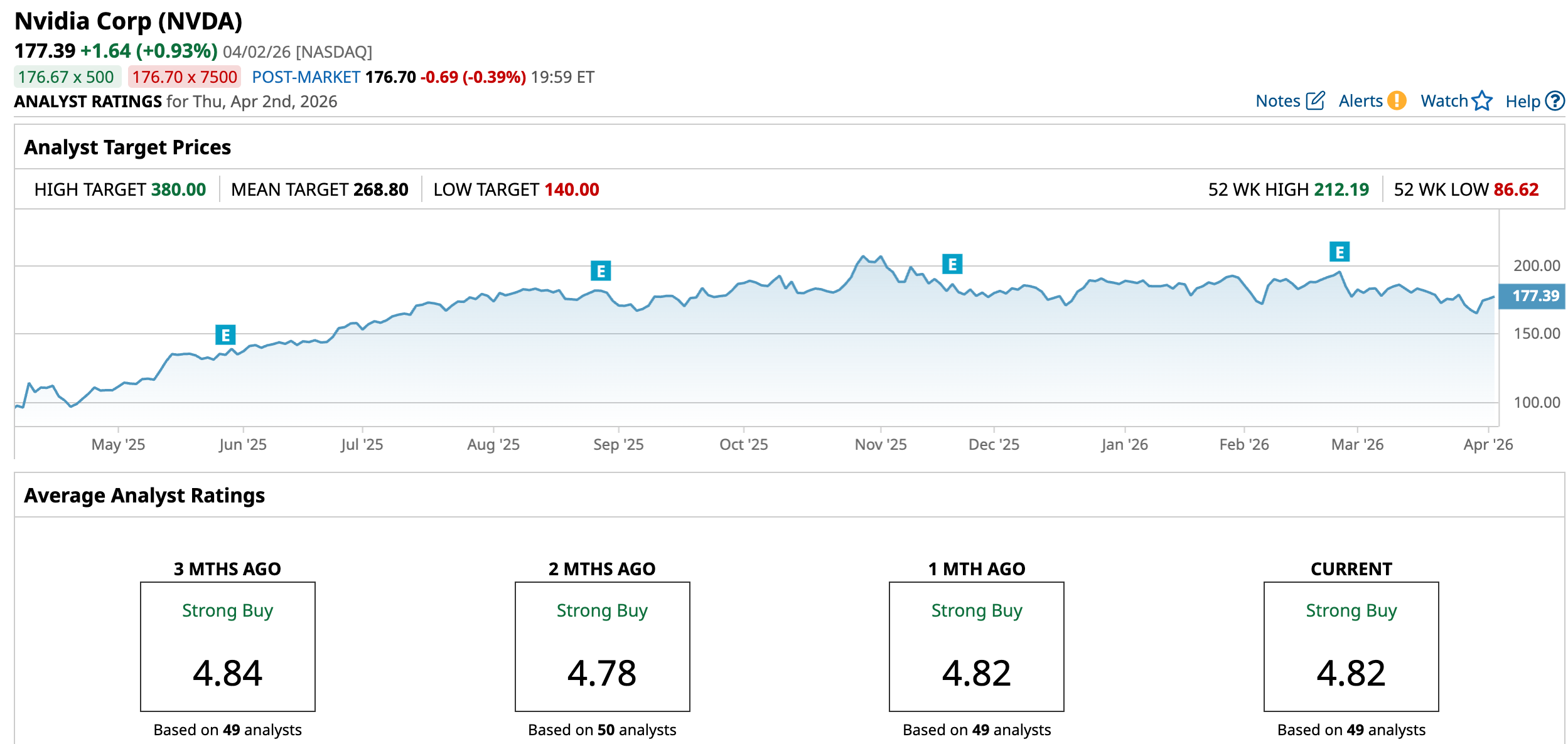

The stock is trading at $177.39 as of April 2, down 4.88% year-to-date (YTD) but up 60.65% over the past 52 weeks.

This valuation embeds a trailing 12‑month price-to-earnings ratio of 38.16 times and a price‑to‑sales ratio of 19.83 times, versus sector medians of 22.27 times and 3.19 times, suggesting a steep premium.

The company just doubled down on the energy industry through a partnership with SLB, expanding its AI reach into complex industrial and subsurface modeling. This also now sits alongside a separate $20 billion catalyst tied to its Groq asset deal.

NVDA’s latest reported quarter, which ended Jan. 26, delivered earnings of $1.57 per share versus a $1.45 consensus, an 8.28% upside surprise that shows demand is still outrunning expectations. This period saw sales of $68.13 billion with 19.51% year‑over‑year (YOY)growth.

That pattern sets the stage for the next report on May 27, 2026, where the current quarter’s average earnings estimate sits at $1.68, more than double the prior year’s $0.77, implying an expected YOY growth rate of 118.18%.

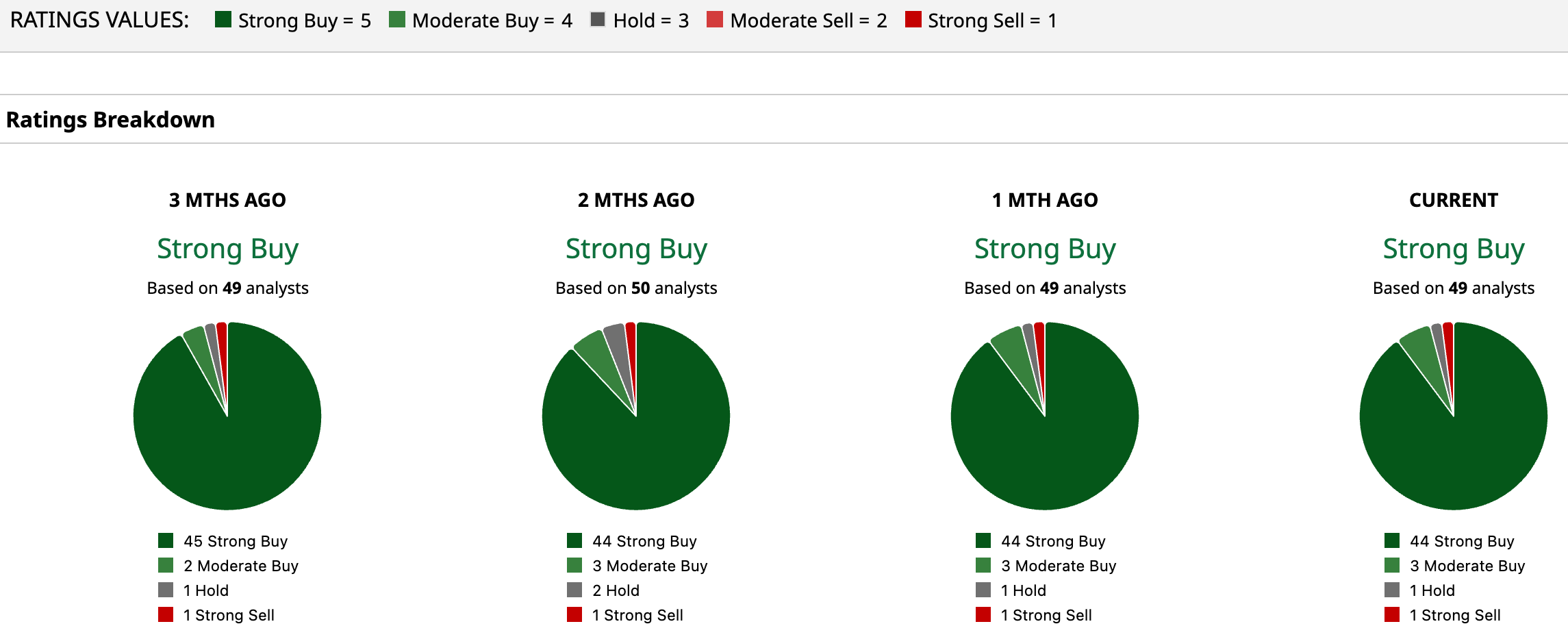

Nvidia carries a consensus “Strong Buy” rating from 49 analysts. It also has an average price target of $268.80, implying roughly 51.5% upside from the current price.

How NVLink Fusion Fits Marvell Technology

From its base in Wilmington, Delaware, Marvell Technology designs custom data center, networking, and storage semiconductors that target AI, cloud, and carrier infrastructure.

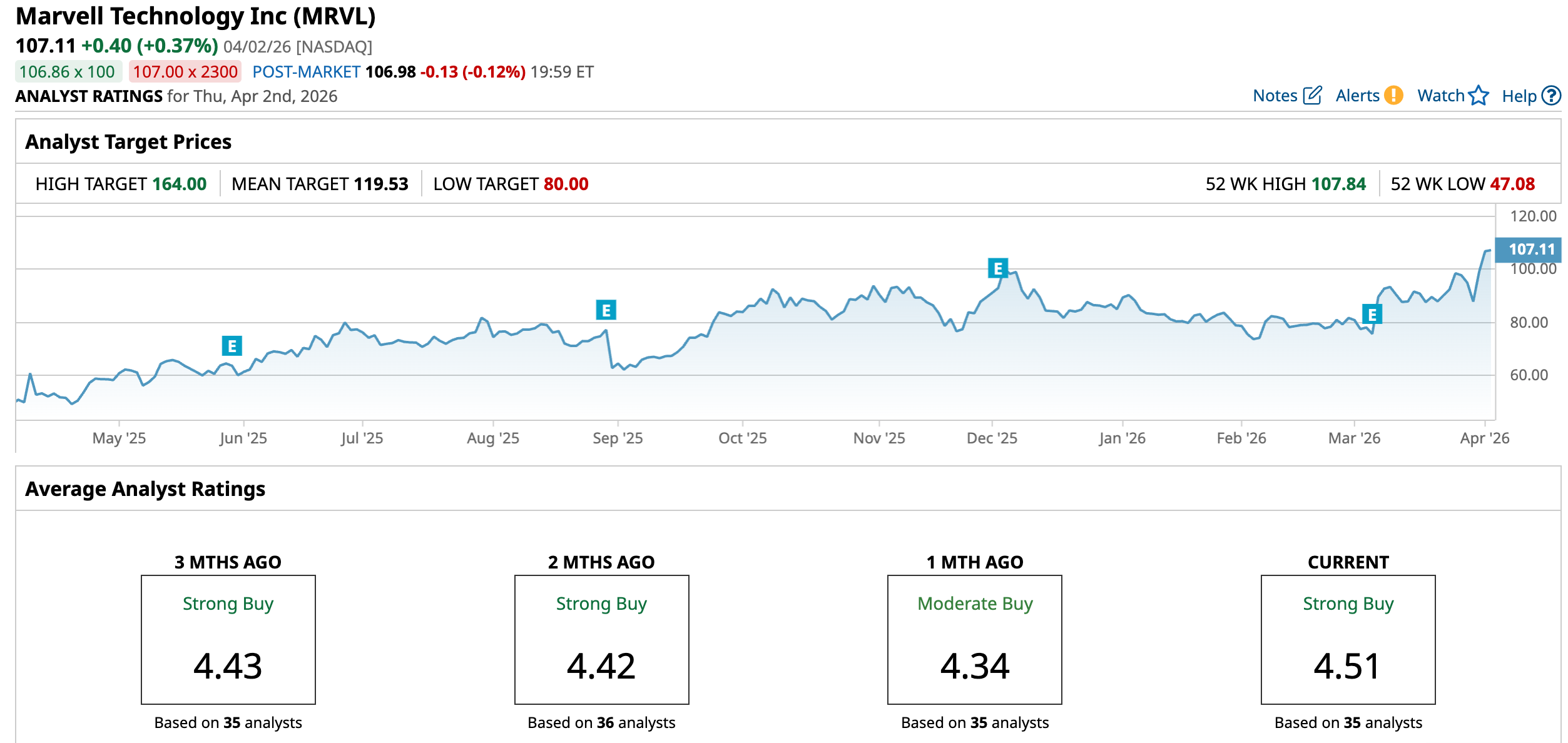

MRVL trades at $107.11 as of April 2, up 26% YTD and 69.4% over the past 52 weeks.

This valuation reflects a forward price-to-earnings of 32.66 times and a PEG ratio of 0.67 times, versus sector medians of 21.41 times and 1.30 times, suggesting investors are paying a growth‑adjusted discount.

Marvell launched a next‑generation CXL switch designed to enable memory pooling and help customers break through the AI “memory wall.” This, alongside the industry’s first 260‑lane PCIe 6.0 switch, is aimed at scale‑up AI data center infrastructure that needs massive on‑package connectivity.

This setup matters directly for Nvidia’s $2 billion investment and the NVLink Fusion narrative, because those CXL and PCIe 6.0 platforms are natural anchors for the kind of semi‑custom, high‑bandwidth fabrics Nvidia wants surrounding its GPUs.

Marvell’s latest reported quarter, which ended Jan. 2026, delivered earnings of $0.66 per share versus a $0.62 estimate, a 6.45% surprise. Also, it produced sales of $2.22 billion with 6.95% growth, while net income was $396.1 million, down 79.17%.

That sets up the next earnings release on June 4, where the current quarter’s average EPS estimate is $0.61 versus $0.47 a year ago, implying 29.79% growth.

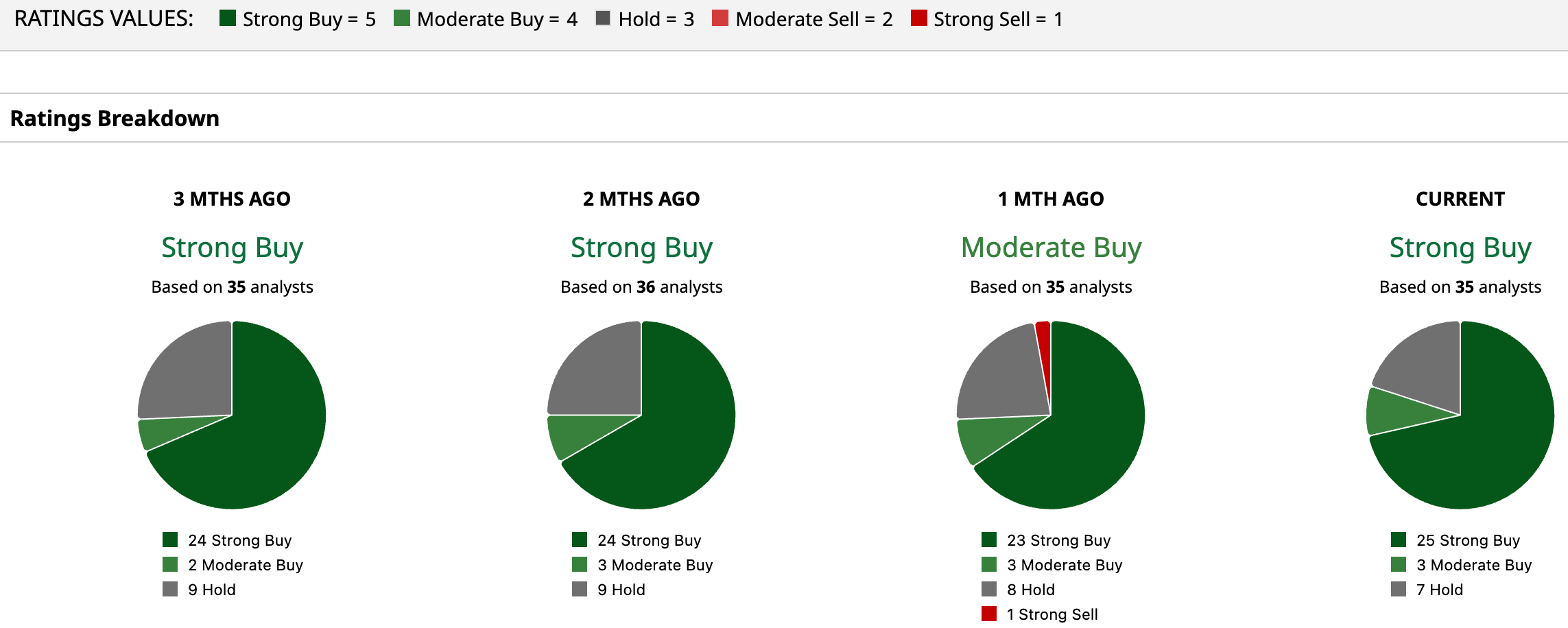

MRVL holds a consensus “Strong Buy” rating from 35 analysts with an average target of $119.53, indicating roughly 11.6% upside from here.

Conclusion

At the end of the day, the key technology behind Nvidia’s $2 billion deal with Marvell is NVLink Fusion, the fabric meant to wire the next generation of AI infrastructure together. This makes Nvidia the architect of the interconnect and puts Marvell in the sweet spot of custom silicon, memory, and switching that plug straight into that ecosystem. NVDA and MRVL both carry rich growth expectations already, yet the direction still looks optimistic as long as AI data center spending and demand for faster, smarter connectivity keep climbing.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)