Billionaire investor Bill Ackman recently took to the social media platform X. He announced that the Federal National Mortgage Corporation (FNMA) (Fannie Mae) and the Federal Home Loan Mortgage Corporation (FMCC) (Freddie Mac) are “stupidly cheap,” and “could be a 10X, and it could happen soon” amid the war in Middle East.

Ackman’s investment machine, Pershing Square Holdings (PSHZF), has just under 10% of the outstanding shares of both Fannie Mae and Freddie Mac, 115.57 million shares of Fannie to be precise. It must be noted that this fact was disclosed in a 13D filing in November 2013, and not in a 13F filing.

On top of that, investor Michael Burry of the “Big Short” fame backed Ackman’s vote of confidence. Fannie Mae’s stock increased by 51.2% intraday on March 30 as a result of this news.

About Fannie Mae Stock

Fannie Mae is a financial solutions provider for residential mortgages in the U.S., operating as a shareholder-owned company under a United States Congressional charter. The company operates in two broad categories: Single-Family and Multi-Family. It offers services like mortgage acquisitions and securitizations, as well as credit risk and loss management.

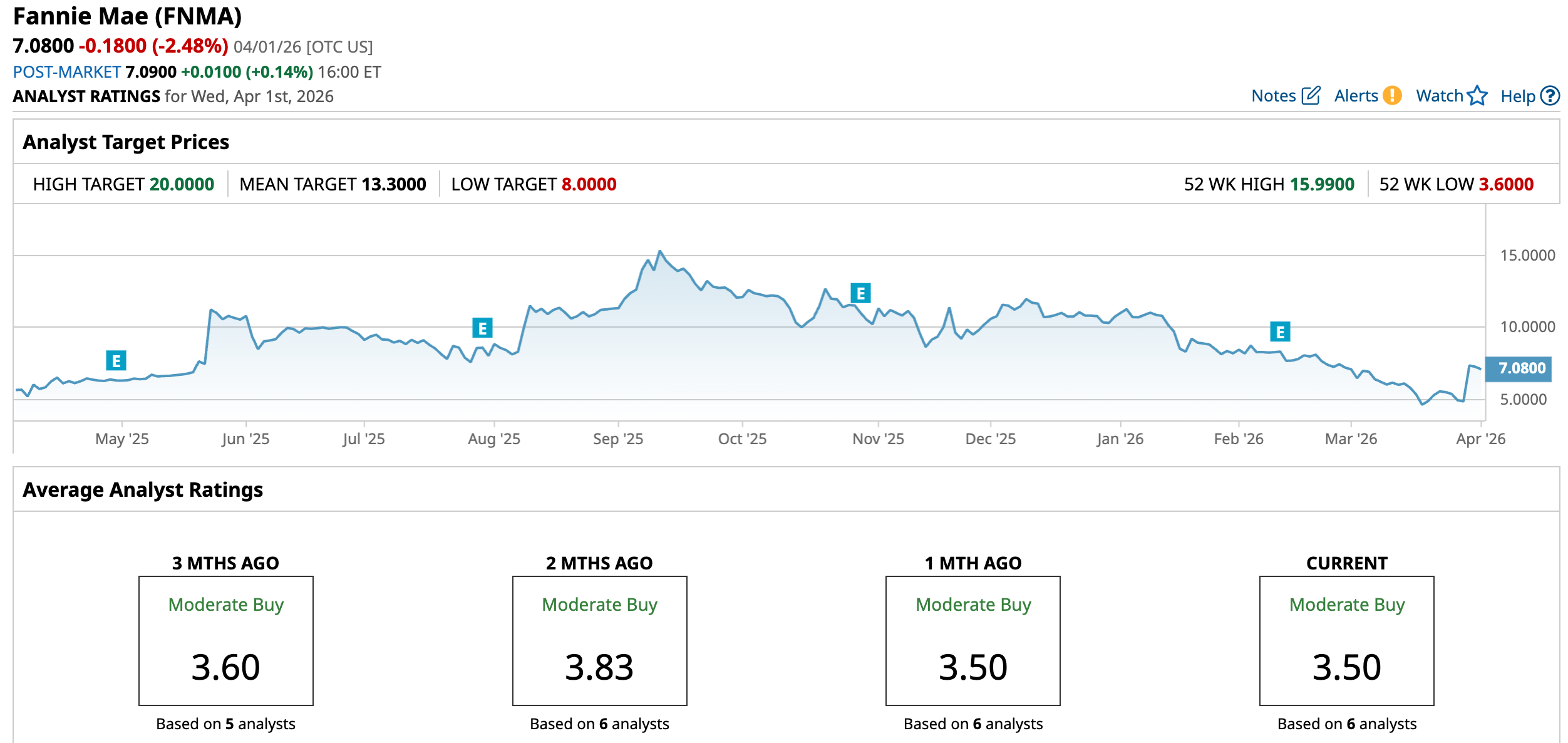

Fannie Mae basically purchases mortgages from lenders and sells them to investors in mortgage-backed securities (MBS). The government-sponsored enterprise (GSE) was first chartered back in 1938, during the “Great Depression,” to ensure a steady supply of mortgage funds. The company has a market capitalization of $8.41 billion.

Fannie Mae’s stock has not recovered much since its crash during the 2008 financial crisis. More recently, mortgage rates have climbed amid war jitters, cooling the housing market and creating volatility in Fannie Mae’s stock price. Over the past 52 weeks, the stock has gained a modest 7.27%, while it is down 34% year-to-date (YTD).

After the rally driven by Ackman’s positive sentiment on Fannie Mae, its 14-day relative strength index (RSI) also climbed to 56.95, indicating strong bullish momentum and gaining conviction. On a forward-adjusted basis, the stock trades at a price-to-sales ratio of 1.43 times, below the industry average of 2.72 times.

Fannie Mae’s IPO Aspirations Are Cooling Down

Fannie Mae and Freddie Mac were placed under a U.S. government conservatorship to bail them out of the 2008 financial crisis. This put the companies under the control of the Federal Housing Finance Agency (FHFA).

However, in the latter half of last year, there was heightened optimism that they would emerge from the conservatorship under the second Trump administration. Hopes of an additional IPO beyond the current OTC Markets listing led Fannie Mae’s stock to a 52-week high ($15.99) in September 2025.

Currently, the stock is down 55.7% from that level, as those privatization aspirations have largely cooled down, and the first quarter has come and gone without any updates on that. Wedbush analyst Henry Coffey believes that if there is any discussion of Fannie Mae, it will be until after the midterms and “on the issue of lowering mortgage cost for residential borrowers.”

Fannie Mae’s Lukewarm Q4 Results

For the fourth quarter of 2025, Fannie Mae’s net revenues remained flat year-over-year (YOY) at $7.33 billion. The top line results were primarily driven by guaranty fees on the company’s $4.10 trillion guaranty book of business.

In the single-family business, conventional acquisition volume increased to $96.80 billion, driven by a $19.20 billion increase in refinance acquisition volume. The segment’s conventional guaranty book decreased from $3.59 trillion in Q3 2025 to $3.58 trillion in Q4 2025. Net revenues from this business were $6.09 billion, remaining flat YOY.

Multifamily acquisition volume also increased from $18.70 billion in the third quarter to $25.80 billion in Q4, while multifamily's book of business grew to $534.70 billion as of Dec. 31, implying a $13.40 billion increase from Sept. 30.

Both single-family and multi-family businesses experienced increases in serious delinquency rates compared to the third quarter. Fannie Mae’s net income dropped by 9% from the prior-year period to $3.53 billion. The single-family business earned a net income of $2.68 billion, down 13% YOY, while the multifamily segment’s net income increased by 10% YOY to $850 million.

Wall Street analysts are moderately optimistic about Fannie Mae’s future earnings. They expect the company’s EPS (on a diluted basis) to increase by 1.61% YOY to $0.63 for the first quarter of 2026. For the current fiscal year, EPS is projected to surge 4.5% annually to $2.55, followed by a 5.1% growth to $2.68 in the next fiscal year.

What Do Analysts Think About Fannie Mae’s Stock?

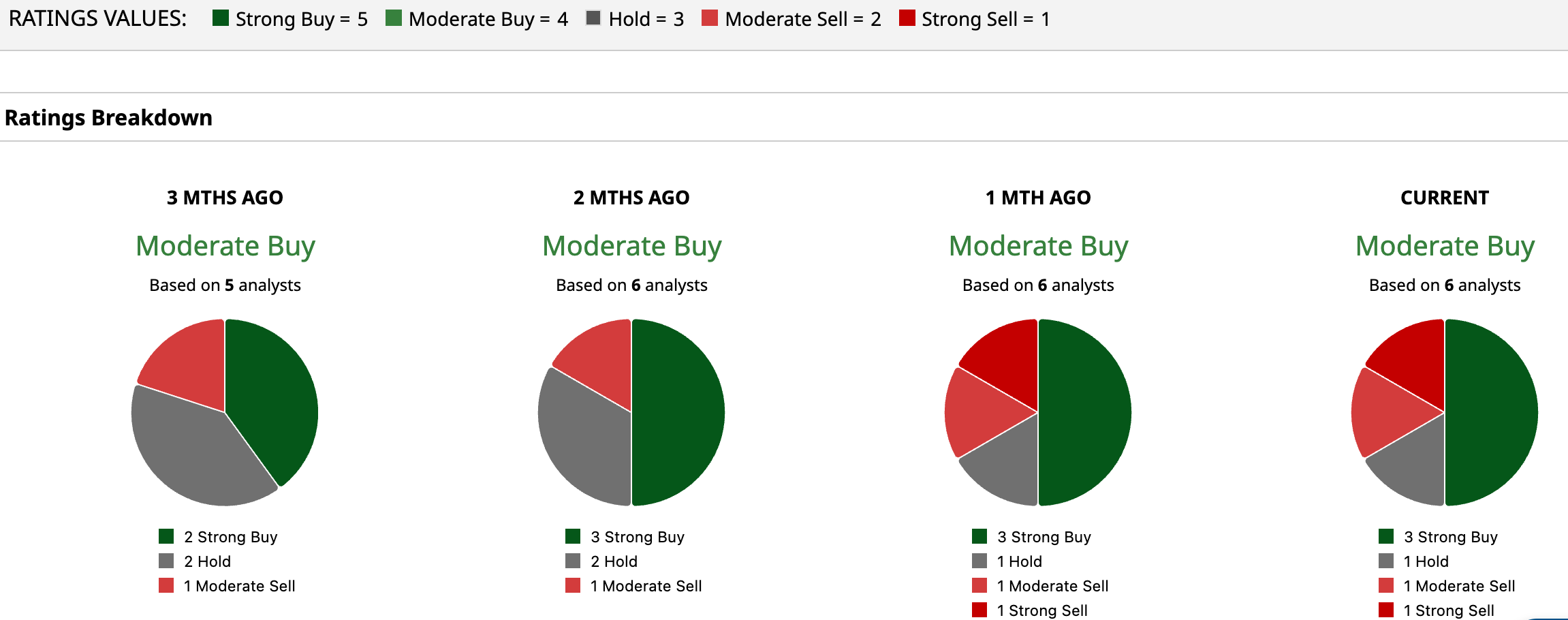

There is a lack of frequent analyst coverage of Fannie Mac’s stock, primarily because of its unique status as a GSE and its long-term conservatorship. This implies that the stock’s dynamics are mainly driven by political decisions, such as policy changes, rather than traditional financial metrics.

However, Wall Street analysts have taken a soundly bullish stance on Fannie Mae, with a consensus “Moderate Buy” rating overall. Of the six analysts rating the stock, three analysts gave a “Strong Buy” rating, one recommended “Hold,” one “Moderate Sell,” and one analyst gave a “Strong Sell” rating. The consensus price target of $13.30 represents an 87.9% upside from current levels, while the Street-high price target of $20 implies a 182.5% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)