Jensen Huang has spent the past year telling investors that Nvidia (NVDA) is entering an “inference inflection”, with AI workloads expected to drive up to one trillion dollars of GPU demand by 2027. In fact, Nvidia’s data center revenue has already climbed more than 13 times since the launch of ChatGPT.

Those projections are showing up in the numbers. Fiscal 2026 revenue jumped 65% year-over-year (YOY) to 215.9 billion dollars, driven by data center chips that now account for most of Nvidia’s sales and generate over 100 billion dollars in annual operating cash flow. That cash is not only fueling buybacks and research spending but also giving Huang the flexibility to take meaningful stakes in other chip and infrastructure companies.

Now that Nvidia has reportedly committed about two billion dollars to Marvell Technology (MRVL), the strategy is becoming clearer. Instead of spreading capital across numerous bets, Huang is choosing a select group of companies that control critical points in the AI supply chain, from high‑speed data center infrastructure to optical technology.

For investors looking to follow a similar approach rather than only holding Nvidia, names like Marvell, Nebius Group N.V. (NBIS), and Lumentum Holdings (LITE) represent three distinct ways to invest in the same AI‑infrastructure cycle Nvidia is helping to build.

Marvell Technology

Marvell Technology has established itself as a key player in the fast‑growing AI and data infrastructure space. The company designs and develops advanced semiconductors that power data centers, cloud networks, and AI systems around the world.

Over the past year, Marvell’s stock has delivered impressive gains, rising 68% over the past 52 weeks and 24% year-to-date (YTD).

The stock trades at a forward P/E of 28.96 times, higher than the semiconductor sector average of 21.28 times, which signals investor confidence in Marvell’s growth story tied to AI demand.

In fiscal 2026, Marvell reported record results with $8.2 billion in net revenue, $2.67 billion in GAAP net income, and $2.47 billion in non‑GAAP profit. The fourth quarter alone produced $2.22 billion in revenue and $0.80 per share in non‑GAAP earnings, slightly ahead of estimates. The company expects about $2.4 billion ±5% in Q1 fiscal 2027 revenue, showing continued momentum.

Also, Marvell is advancing on the innovation front. Nvidia’s recent $2 billion investment deepens its partnership on AI infrastructure and silicon photonics, helping address demand for faster and more power‑efficient data connectivity. Marvell’s new Structera S 30260 CXL switch is another highlight, offering a solution to the AI “memory wall” by improving bandwidth and enabling more efficient memory sharing across servers. These advances strengthen Marvell’s position in the AI supply chain.

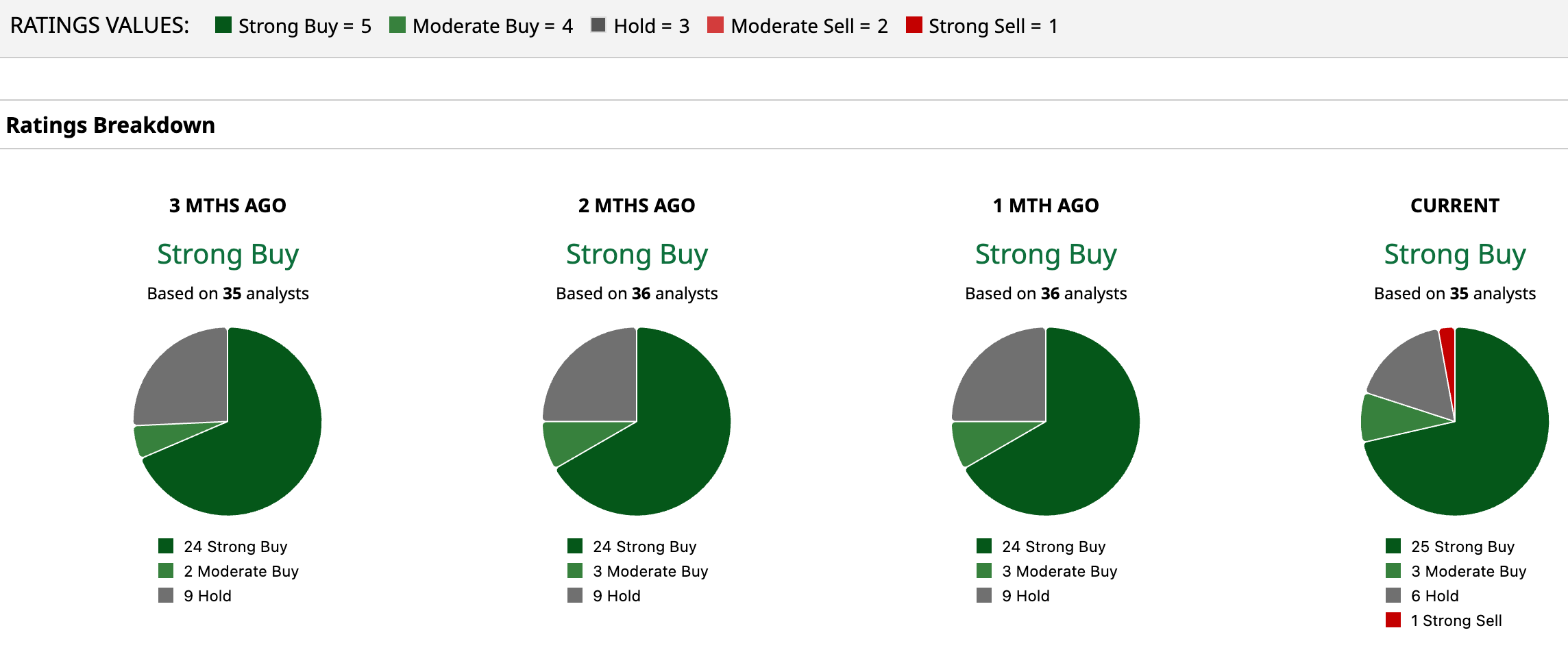

Analysts remain positive, with 35 on Wall Street giving MRVL a consensus “Strong Buy” rating and an average price target of $119.53, suggesting about 12.6% upside from current levels.

Nebius Group N.V.

Nebius has quickly become one of the most watched names in AI infrastructure, building advanced cloud, compute, and semiconductor technologies that power next‑generation artificial intelligence systems.

The stock has delivered huge gains, climbing 352% over the past 52 weeks and another 22.5% YTD, showing strong investor confidence in the company’s growth path.

Its financial performance backs that up. In Q4 2025, revenue jumped a whopping 547% YOY to $227.7 million, while full‑year sales rose 479% to $529.8 million. Also, the company posted $29 million in full‑year net income, a reversal from the previous year’s loss, signaling stronger cost control and scalability. Notably, its cost‑of‑revenue ratio fell from 60% to 30% in Q4, a sign that the business model is becoming more efficient as it scales.

Further, the company’s AI cloud arm continues to expand at a rapid pace. It announced plans to build a 310 MW AI factory in Finland, and is set to be one of Europe’s largest by 2027. Alongside that, the new Nebius AI Cloud 3.5 launch introduced serverless AI capabilities that make it easier for developers to run models and speed up production. These efforts highlight how Nebius is strengthening its position in the AI cloud ecosystem.

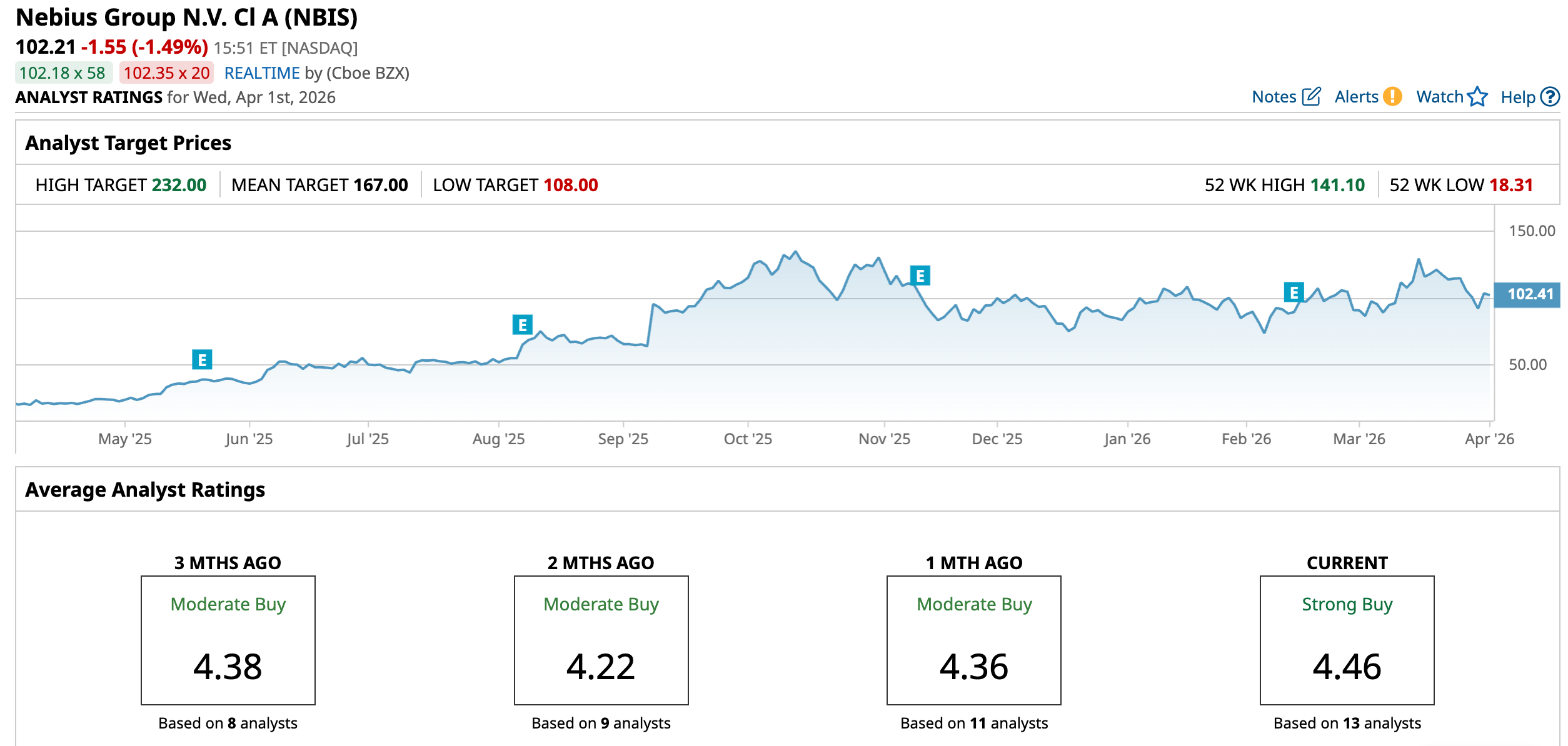

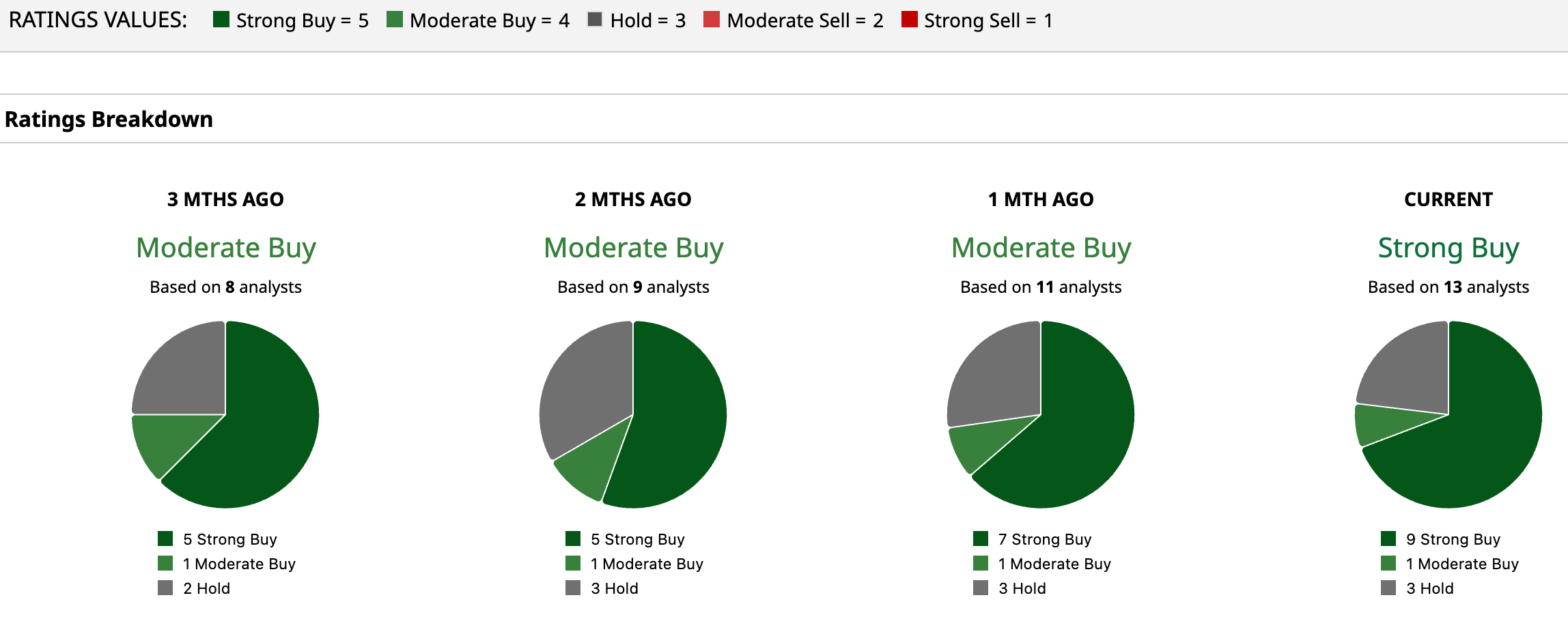

Analysts remain highly optimistic. Of 13 analysts covering NBIT, nine rate it as a “Strong Buy,” one goes with a “Moderate Buy,” and the remaining analyst rates it as a “Hold.” And an average price target of $167 suggests a 63.4% upside from current levels.

Lumentum Holdings

Lumentum has become one of the biggest winners in the AI hardware space, supplying the laser and photonics technology that supports modern data centers and optical networks.

The stock has been a standout performer, jumping 1,110% over the past 52 weeks and up another 108.7% YTD.

Valuations are steep, with a forward P/E of 110.95 times compared to the semiconductor sector average of about 21.28 times, showing the amount of optimism priced in toward future growth.

In its most recent results, the company reported $665.5 million in Q2 fiscal 2026 revenue, up sharply from $402.2 million a year earlier, with GAAP net income of $78.2 million. Non‑GAAP EPS came in at $1.67, and management forecasts Q3 revenue between $780 million and $830 million, with a non‑GAAP operating margin of up to 31%. This marks a strong improvement from 2025’s losses, supported by new product launches and stronger execution.

And, Lumentum is expanding its production footprint in the U.S. The company announced a new 240,000‑square‑foot laser manufacturing facility in Greensboro, North Carolina, that will produce advanced indium phosphide (InP) optical devices for major AI data centers. It also partnered with Marvell Technology to demonstrate optical circuit switching for next‑generation AI infrastructure, a technology that enables faster, more efficient data movement across large AI clusters.

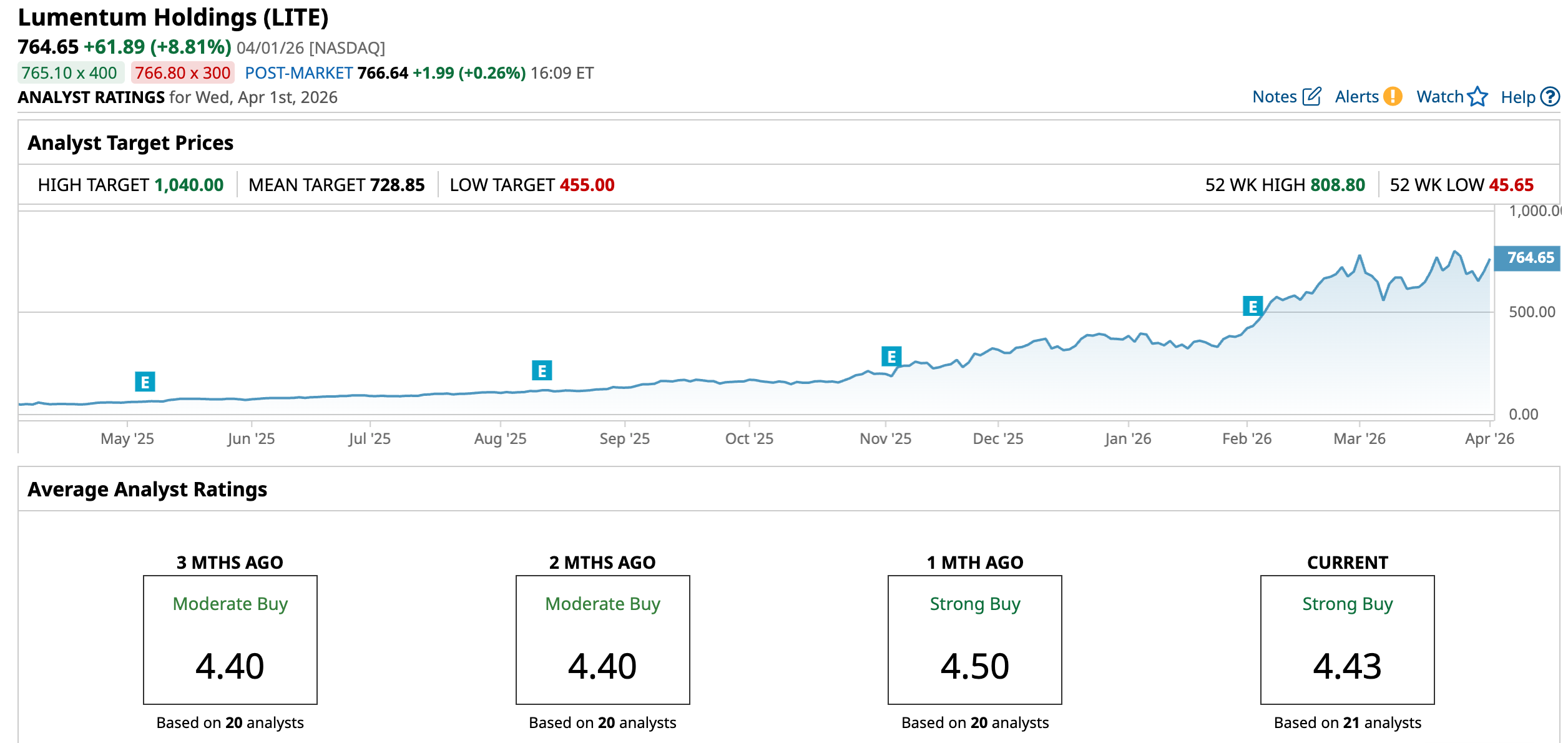

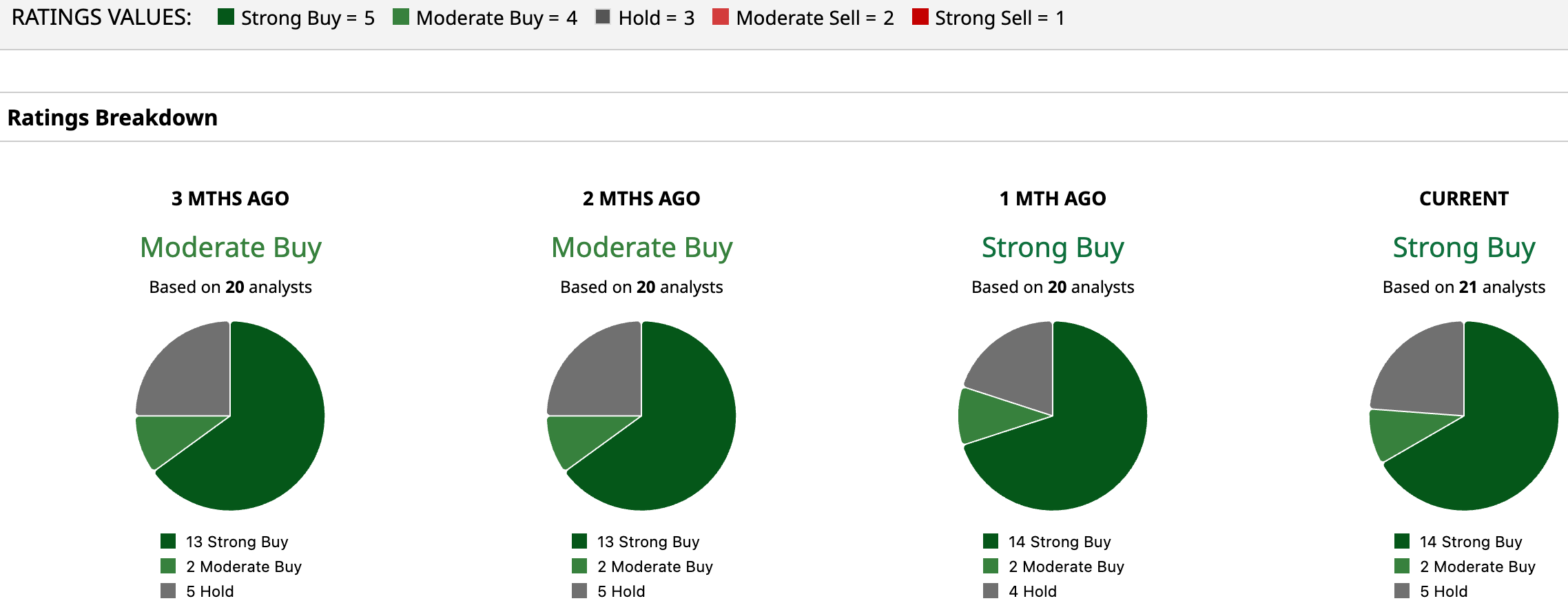

Analysts remain highly positive. Of 21 covering the stock, 14 have given a “Strong Buy," two have gone with a “Moderate Buy,” and the remaining five analysts rate the stock a “Hold.” Already surpassing the average price target is $728.85, the Wall Street-given high of $1,040 suggests a 36% climb from here.

Conclusion

If Jensen Huang’s investment trail is any indication, the AI infrastructure story is just getting started. Marvell, NBIS, and Lumentum each sit at critical junctions of that ecosystem, connecting the chips, memory, and optics that make large-scale AI possible. These are not speculative moonshots but companies already showing explosive growth and strategic relevance. Given their momentum, shares could still move higher through 2026 as AI deployment deepens and data center spending ramps up. While volatility is inevitable, the direction for these names, at least for now, still looks decisively up.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)