Uranium (UXJ26) and energy have been a much-discussed theme over the past year or so, mainly due to the extreme energy requirements of modern data centers and AI workloads. For the past month, though, the news was dominated by uranium in a specific part of the world: Iran. Iran holds over 450 kg of highly enriched uranium (HEU), according to some estimates. Donald Trump is considering acquiring this stockpile, either through diplomacy or through brute force.

There are multiple reasons why investors should look at uranium differently than maybe a couple of years ago. Now, institutional investors are taking a keen interest in the silvery-grey metal, even as a standalone asset class. This institutional participation helps remove supply from the market and protects against downside risk. Moreover, the U.S. government has committed $2.7 billion over the next 10 years to broaden the country’s uranium enrichment capabilities. As a result, the radioactive material is now considered a strategic resource, just like lithium and rare earth minerals.

The above factors support uranium producers’ bull thesis in addition to the already well-known artificial intelligence-related bull scenario. As a result, uranium stocks deserve a more in-depth look, and one of those stocks is Cameco Corporation (CCJ).

About Cameco Stock

Cameco Corporation is a global enterprise with its headquarters situated in Saskatoon, Canada, which concentrates on the production of uranium for government and commercial entities. The company’s main clientele is in the energy sector, which includes electricity generation companies as well as nuclear power utilities.

CCJ stock has delivered returns of 170% over the past year. This is a significant outperformance against the Global X Uranium ETF (URA), which has returned 117% during the same period. CCJ continues to follow uranium prices, so if investors are bullish on uranium demand and price, the stock offers a high-risk, high-reward exposure to the same.

The stock is currently trading at a forward PE of 97.2x, well above the energy sector’s median forward PE of 14.63x. This looks overvalued until one looks at the stock’s own five-year average of 82.6. The stock has always traded at this premium, but considering how important uranium has become right now, a 17.7% premium to historic valuations is reasonable. Moreover, CCJ is also trading at a forward EV/EBITDA of 34.75, almost half the five-year average of 60.55x.

The company’s earnings growth rate isn’t too bad either. Wall Street expects the firm to grow its EPS by 63.57% in 2027 and 25.7% in 2028. CCJ has also significantly improved its profitability over the past few years, with net margins of 16.93% compared to the five-year average of 5.76%. This is simply a company with improved operations in a niche with government backing and strong demand. It can continue to trade at a high valuation, considering the current geopolitical environment as well as demand from AI.

Cameco Beats Earnings Expectations

Cameco Corporation reported its Q4 2025 results on Feb. 13. Net earnings rose $418 million for the year and $64 million for the quarter compared to Q4 2024. Adjusted net earnings increased $60 million for the quarter and $335 million for the year. Full-year adjusted EBITDA grew by around $398 million to reach $1.9 billion. This growth was mainly driven by Westinghouse’s annual revenue from the Dukovany construction project and higher uranium prices. The company ended the quarter with $1.2 billion in cash and short-term investments and $1.0 billion in total debt.

The ongoing quarter contained a positive development for the company when it secured an agreement with India to supply 22 million pounds of uranium over the course of the next nine years. The contract is valued at $2.6 billion. The deal shows Cameco isn’t just instrumental to the United States’ nuclear ambitions but is a vendor of choice for other countries as well. More than earnings, this status powers the company’s bull thesis and also explains the relatively high valuation.

What Are Analysts Saying About CCJ Stock?

On March 27, UBS analyst George Eadie reiterated his “Hold” rating on CCJ stock. He also raised his price target on the shares from $100.66 to $111.44. Immediately after the earnings report, four different analysts raised their target prices on the stock. The highest price target of $133 was assigned by Katie Lachapelle of Canaccord Genuity on March 2, so there is considerable bullish sentiment since the Feb. 13 earnings call.

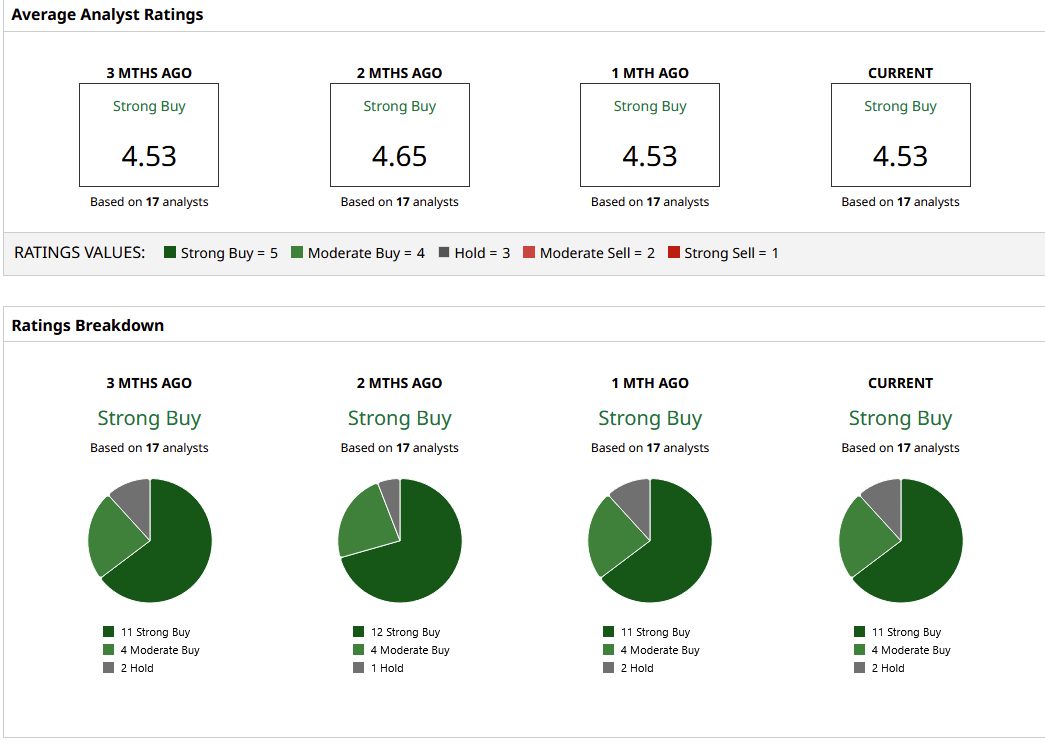

There are 17 analysts who currently cover CCJ stock on Wall Street, with 11 of them assigning a “Strong Buy” rating to the stock. There are no “Sell” or “Strong Sell” ratings. The mean target price of $125.88 offers 11.4% upside from here on, whereas if the most bullish thesis were to play out, investors could net gains of 29%.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)