/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)

Micron Technology (MU) has found itself caught in a familiar market pattern — a knee-jerk reaction to a change in the way we think about a particular type of technology. In this case, the recent introduction of TurboQuant from Alphabet (GOOGL) — a program that promises to cut memory usage in half — is presenting AI efficiency fears.

While this may initially be seen as a negative for memory and storage-related companies as a whole, if we take a step back and think about it for a moment, I believe this is yet another example of the markets overreacting to change. One report from Bank of America analyst Vivek Arya recently aimed to ease concerns by pointing out that AI capital expenditures are actually driving memory usage, “not efficiency measures.”

This kind of panic is not a new trend, either. Investors witnessed something similar in early 2025 after news of DeepSeek emerged. The initial fear of reduced spending and efficiency gave way to even more spending later.

About Micron Stock

Based in Boise, Idaho, Micron is one of the world's leading memory and storage companies. With a market capitalization of roughly $363 billion, Micron is of critical importance in the semiconductor business, especially in DRAM and NAND, which are vital in AI and data-center infrastructure.

The price of MU stock has declined significantly of late. Shares are down 28% from the 52-week high of $471.34, and in the last five days alone, MU is down by 15%. Such a significant fall in price is likely to shift market sentiment, and in comparison to the market’s general movement, it is more of a beta-driven fall than anything else.

From a valuation perspective, however, things are starting to look interesting again. With record profitability and expanding margins, this is no longer the cyclical memory business that investors used to discount so heavily. Gross margins came in above 74% in the most recent quarter, a level that would have seemed unreasonable even a few years ago. While MU stock may not be "cheap" in absolute terms, it's becoming reasonable in relation to earnings and structural positioning in AI.

Micron also offers a dividend, which was recently raised by 30% to a quarterly rate of $0.15 per share.

Micron Beats on Earnings

Micron's latest fiscal second-quarter 2026 results were simply exceptional. Not only was top-line growth tremendous with revenue of $23.86 billion — almost triple sales of $8.05 billion in the same period last year — but bottom-line growth was equally impressive. GAAP EPS came in at $12.07, up from $1.41 in the year-ago period, while non-GAAP EPS was $12.20, up from $1.56. This was not an EPS beat, but a step function in EPS.

Operating cash flow came in at $11.9 billion, and free cash flow was $6.9 billion. In every aspect of its business, Micron is doing extremely well. In cloud memory, for example, revenue was $7.7 billion. In the data-center segment, revenue more than doubled to almost $5.7 billion. In every segment, operating margins were in the 60% to 70% range. Looking forward, management is also guiding for another round of significant records in fiscal Q3.

The takeaway from this report is that memory is now a strategic asset in AI infrastructure. And this is structural, not cyclical. There seem to be no signs of weakening memory demand due to efficiency gains. In fact, the opposite may be true as models get bigger and more complex — memory requirements could increase despite efficiency gains.

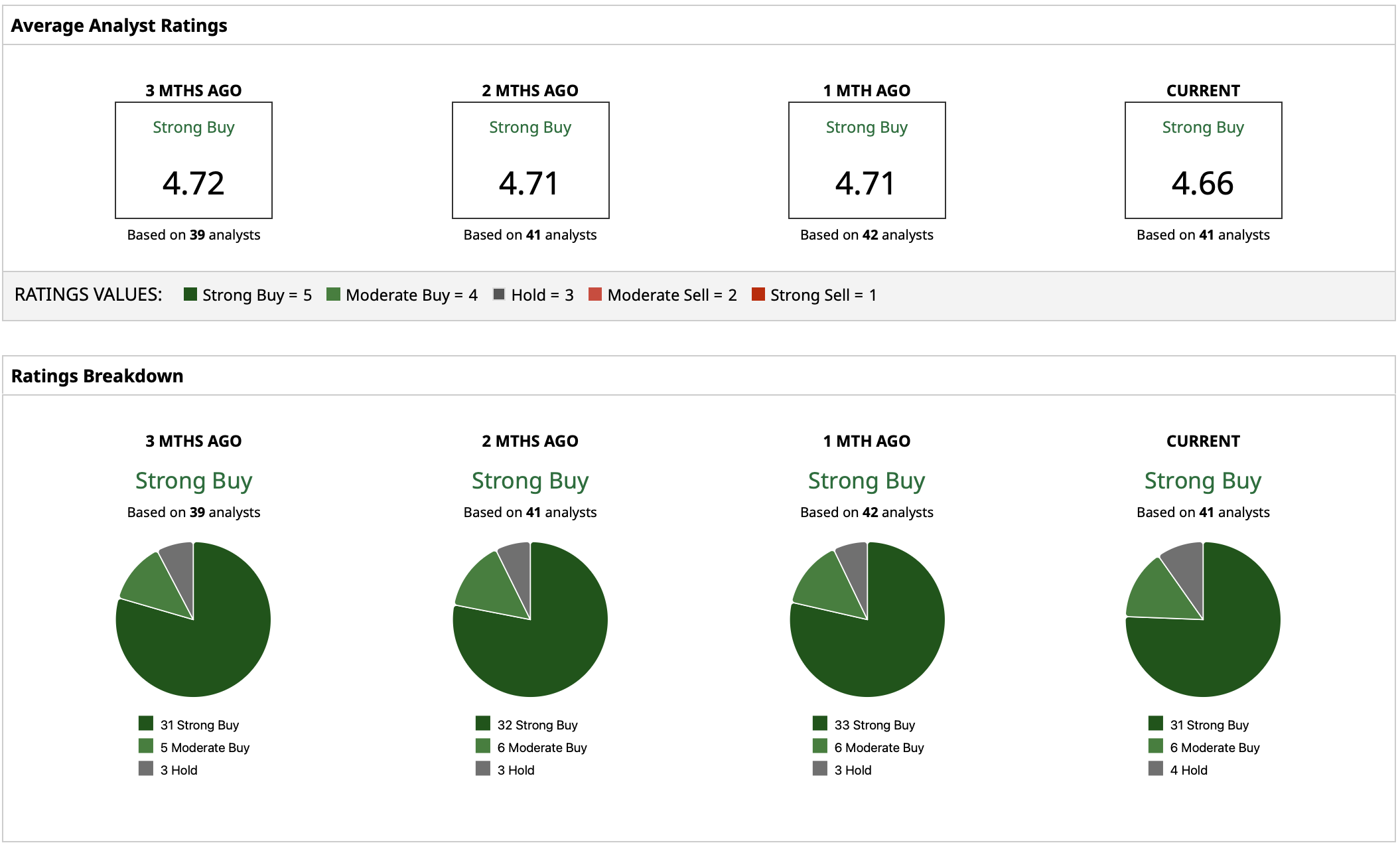

What Do Analysts Expect for Micron Stock?

Wall Street analysts are firmly bullish on MU stock with a “Strong Buy” consensus rating. The stock enjoys high support, and analysts are citing both near-term earnings growth and long-term memory demand fueled by AI. The recent pullback in MU stock hasn’t altered this opinion, and actually may have improved it.

The mean price target for Micron stock is $494.81, representing potential upside of around 46% from current levels. The high target is $750, illustrating the range of outcomes for memory and AI infrastructure scaling. Meanwhile, the low target of $140 may reflect a bit of caution around the cyclical nature of memory, a common theme in memory stocks.

On the date of publication, Yiannis Zourmpanos had a position in: MU . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)