/Meta%20by%20creativeneko%20via%20Shutterstock.jpg)

Shares of Meta Platforms (WPM) have come under sharp pressure, falling almost 12% over the past five trading sessions. The abrupt pullback is being driven by growing investor concerns around Meta’s escalating artificial intelligence (AI) spending. While these investments are aimed at strengthening Meta’s long-term positioning in generative AI and recommendations, they are also raising near-term fears of margin compression and uncertain return timelines.

Plus, a rising legal overhang tied to social media addiction lawsuits is beginning to weigh on the stock. Recent trial developments have increased the risk of broader liability exposure, as courts scrutinize the impact of Meta’s platforms on younger users, potentially opening the door to costly settlements and prolonged regulatory pressure.

Against this backdrop of surging AI-driven costs and mounting legal risks, the recent decline reflects a rapid repricing of expectations. With valuation multiples compressing and the stock trading well below its peaks, is it an attractive entry point now?

About Meta Stock

Meta Platforms is a technology conglomerate headquartered in Menlo Park, California, best known for owning and operating some of the world’s most influential social media and communication platforms, including Facebook, Instagram, WhatsApp, Messenger and Threads. Originally founded as Facebook in 2004, the company rebranded to Meta in 2021 to reflect its strategic pivot toward immersive technologies such as virtual reality, augmented reality, and the metaverse.

In addition to its flagship apps, Meta develops hardware and AI-driven products through divisions like Reality Labs, spanning VR headsets and smart glasses. Meta’s market cap stands at $1.3 trillion, ranking it among the largest technology companies globally.

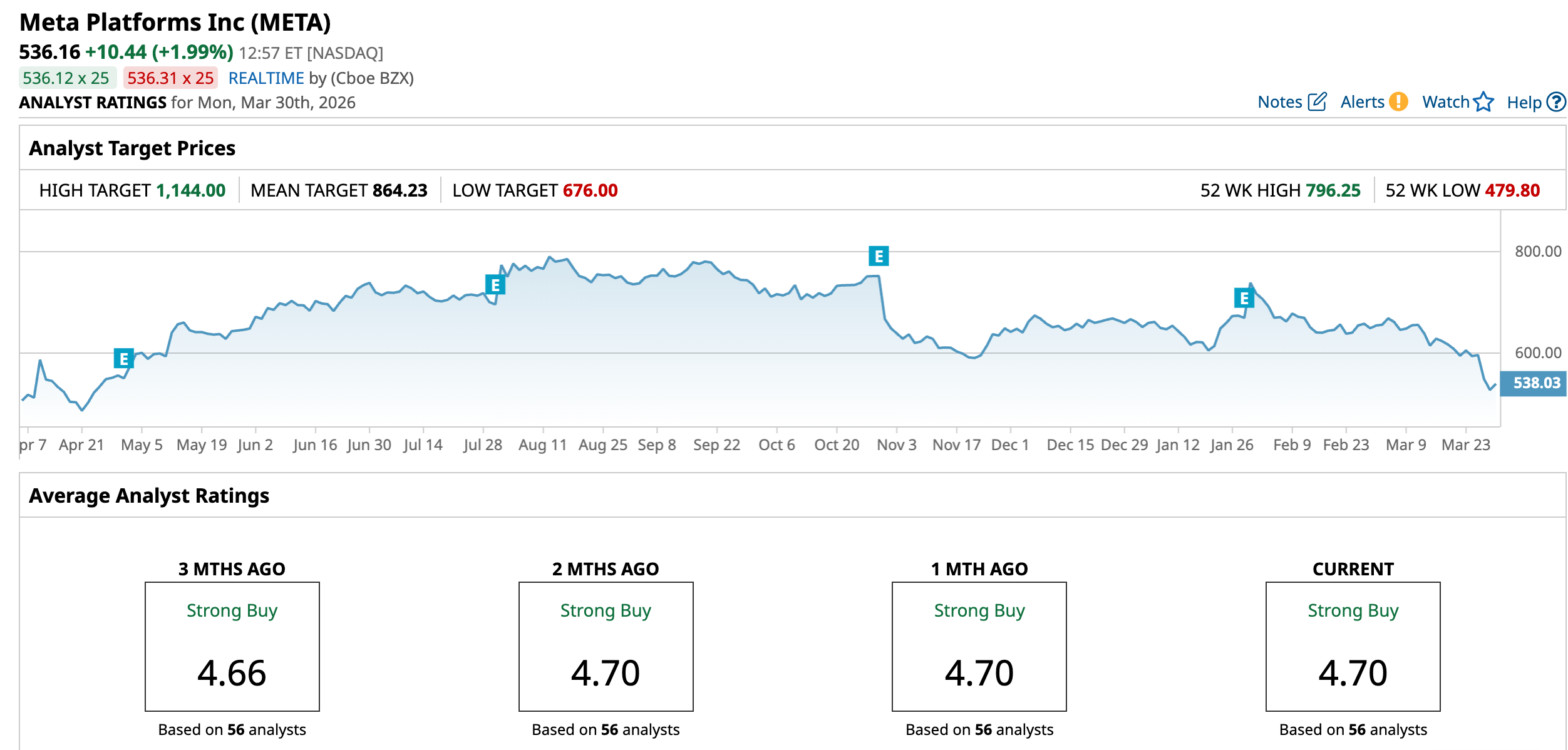

Shares of Meta Platforms have entered a period of heightened volatility. Most notably, the stock has declined 11.13% over the past five trading days, marking one of the steepest short-term drawdowns in recent months.

Meta’s weakness has been building over time. The stock is down 18.67% year-to-date (YTD), amid rising concerns around cost structures and regulatory risks. Over the past 52 weeks, the decline has been more moderate at about 6.92%.

Importantly, Meta is now trading well below its 52-week high of $796.25 reached in August 2025, implying a drawdown of 32.5% from peak levels. The correction reflects investor concerns around the sustainability of Meta’s earnings trajectory as the company ramps up capital expenditures, particularly in AI, while also facing mounting legal headwinds tied to social media addiction litigation.

Meta’s capital expenditure strategy has become a central concern for investors, primarily due to the sheer scale and pace of spending tied to its AI ambitions. The company has guided for $115 billion to $135 billion in capex for 2026, nearly double the roughly $72.2 billion spent in 2025, marking one of the largest single-year investment ramps.

This aggressive spending is largely directed toward AI infrastructure, including data centers, and advanced computing capacity to support its “superintelligence” initiatives. While strategically necessary to compete with peers, the magnitude of this outlay has raised concerns about near-term profitability.

On the other hand, the legal overhang tied to social media addiction represents one of the most significant and emerging risks for Meta, and it stems from a series of landmark court rulings in March 2026 that fundamentally challenge how its platforms are designed and monetized. Meta has suffered several lawsuit defeats in the past week and found liable for contributing to a young user’s mental health harm through addictive platform design.

META currently trades at a premium compared to the sector median but below its own historical average at 18.40 times forward earnings.

Stable Top Line Growth

Meta Platforms’ fourth-quarter and full-year 2025 results, released on Jan. 28, reflected continued top line strength alongside intensifying investment in AI and infrastructure.

For Q4 2025, Meta reported revenues of $59.9 billion, up 24 % year-over-year (YOY), driven by robust advertising demand across its Family of Apps. Net income for the quarter rose 9% from the prior-year quarter to $22.8 billion, while earnings per share (EPS) increased 11% to $8.88 compared with $8.02 in Q4 2024, exceeding analyst expectations. Total operating margins for the quarter were about 41%, compressed versus Q4 2024 as costs climbed with higher infrastructure and investments.

On a full-year basis, Meta’s 2025 revenue reached $201 billion, up 22% from $164.5 billion in 2024, underscoring sustained demand. However, full-year net income was $60.5 billion, modestly below the prior year’s $62.4 billion, while EPS came in at $23.49, a decline of about 2% from $23.86 in 2024, reflecting the impact of significantly higher expenses tied to scaling AI infrastructure and other strategic initiatives.

In tandem with these results, management provided 2026 guidance that emphasized continued growth and heavy investment in AI capabilities. For the first quarter of 2026, Meta guided revenue of $53.5 billion to $56.5 billion.

Additionally, despite the elevated expense base, Meta reiterated its expectation that operating income in 2026 will exceed 2025 levels, underscoring management’s confidence in long-term profitability even as it invests heavily in future growth engines.

Analysts predict EPS to be around $29.75 for fiscal 2026, up slightly YOY, before surging by 14.9% annually to $34.19 in fiscal 2027.

What Do Analysts Expect for Meta Stock?

Meta Platforms is currently navigating a period of heightened investor scrutiny, with its recent share price weakness. However, analyst sentiment remains broadly positive.

Earlier this month, Morgan Stanley cut its price target on Meta Platforms to $775 from $825 but maintained an “Overweight” rating, noting that sentiment has weakened amid concerns over AI investment returns and regulatory risks. Despite near-term estimate cuts, the firm views the pullback as a compelling buying opportunity.

Also, Evercore ISI reiterated an “Outperform” rating and $900 price target on Meta, downplaying concerns around legal exposure tied to underage users. The firm estimates users aged 8 to 13 represent only a mid-single-digit share of Meta’s 3.6 billion daily users and notes that such risks have long been debated.

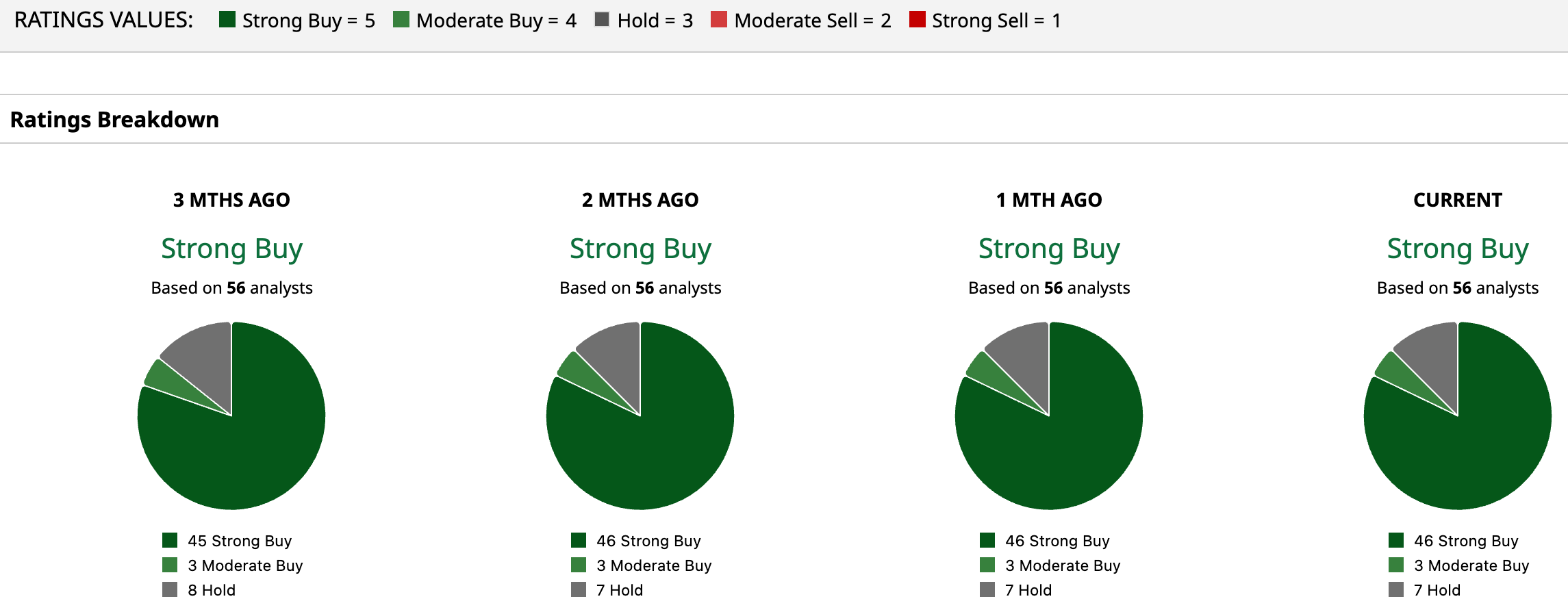

Overall, META has a consensus “Strong Buy” rating. Of the 56 analysts covering the stock, 46 advise a “Strong Buy,” three suggest a “Moderate Buy,” and the remaining seven analysts are on the sidelines, giving it a “Hold” rating.

The average analyst price target for META is $864.23, indicating a potential upside of 61.2%. The Street-high target price of $1,144 suggests that the stock could rally as much as 113.4%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)