/Semiconductor%20by%20Sach336699%20via%20Shutterstock.jpg)

Arm Holdings (ARM) has transitioned from being a familiar face in the semiconductor licensing industry to being one of the more intriguing plays in the AI infrastructure space. This transformation has accelerated in recent times, especially after Needham & Company upgraded the company to a "Buy" rating with a $200 price target, citing its riskier strategic bets are now starting to pay off. The timing of the move by Arm Holdings also coincides with the growing realization by investors that CPUs are now set to be much more important in agentic AI and inference-heavy data centers than was anticipated just a year ago.

This sets the stage for the recent run in ARM stock's price. While the shares retreated partially on Friday, they are still significantly higher than the 52-week low and are trading within about 20% of the 52-week high. On a broader level, the market appears to be rethinking Arm as a winner in the AI platform space rather than just a royalty collector, especially after the company announced its first in-house-designed data center chip.

About Arm Stock

Arm Holdings is a semiconductor IP company based in Cambridge, UK, with a market capitalization now of roughly $163.5 billion. While the company has traditionally made its money through the licensing of its chip designs in exchange for royalties, the company now appears to be making a more concerted effort to move into higher-value compute subsystems, data center CPUs, and AI infrastructure opportunities. According to Reuters, the company announced its new AGI CPU designed for agentic AI workloads with Meta (META) as its lead partner.

From a stock performance perspective, it has not been easy to ignore the company in recent weeks. Yes, the stock fell hard on Friday and is already looking choppy today, but it still remains nearly 80% above its 52-week low of $80 a share and only 20% below its 52-week high of $183.16, as the data in the table above illustrates.

Yes, the valuation remains rich. ARM trades at 41.4 times sales and nearly 159 times forward earnings, as the data in the table above illustrates. Still, the market is not only willing to pay high prices for ARM anymore. It is willing to pay a premium for a company that now has exposure to the growth in artificial intelligence royalties, compute subsystems, as well as silicon. The upgrade by Needham & Company reflects this change in market perception.

Arm Beats on Earnings

Arm Holdings reported a strong fiscal third quarter. Revenue rose 26% year-over-year (YoY) to a record $1.24 billion. In addition, the company reported that royalty revenue grew 27% to $737 million, and licensing and other revenue grew 25% to $505 million. In addition, the company reported a fourth consecutive billion-dollar revenue quarter. This is as clear an indicator as one could find that the Arm platform is expanding well beyond smartphones.

The drivers of growth were strong, underpinned by increasing adoption of Armv9, improved adoption of Arm Compute Subsystems, and increasing adoption of Arm-based chips in data centers. In addition, the company has signed 21 CSS licenses to date, well in advance of its plan. Furthermore, the management is confident that Arm's market position in the top hyperscalers is forecast to be close to 50%. These are words that grab investors’ attention, especially in a period where CPU relevance in AI infrastructure is back in focus.

Management's near-term outlook also remains solid. Arm projected fiscal Q4 2026 revenue of $1.47 billion, plus or minus $50 million. It also projected non-GAAP EPS of $0.58, plus or minus $0.04. This is a very bullish environment for ARM, and now, combined with ARM's biggest announcement in years of AGI CPU. Reuters said that Arm is expecting its chip to begin contributing meaningfully over time. Arm is targeting up to $15 billion in annual revenue from its AGI CPU within five years. This is certainly ambitious. But it explains why Wall Street is so suddenly enthusiastic.

The next ARM earnings announcement is scheduled for May 6, 2026.

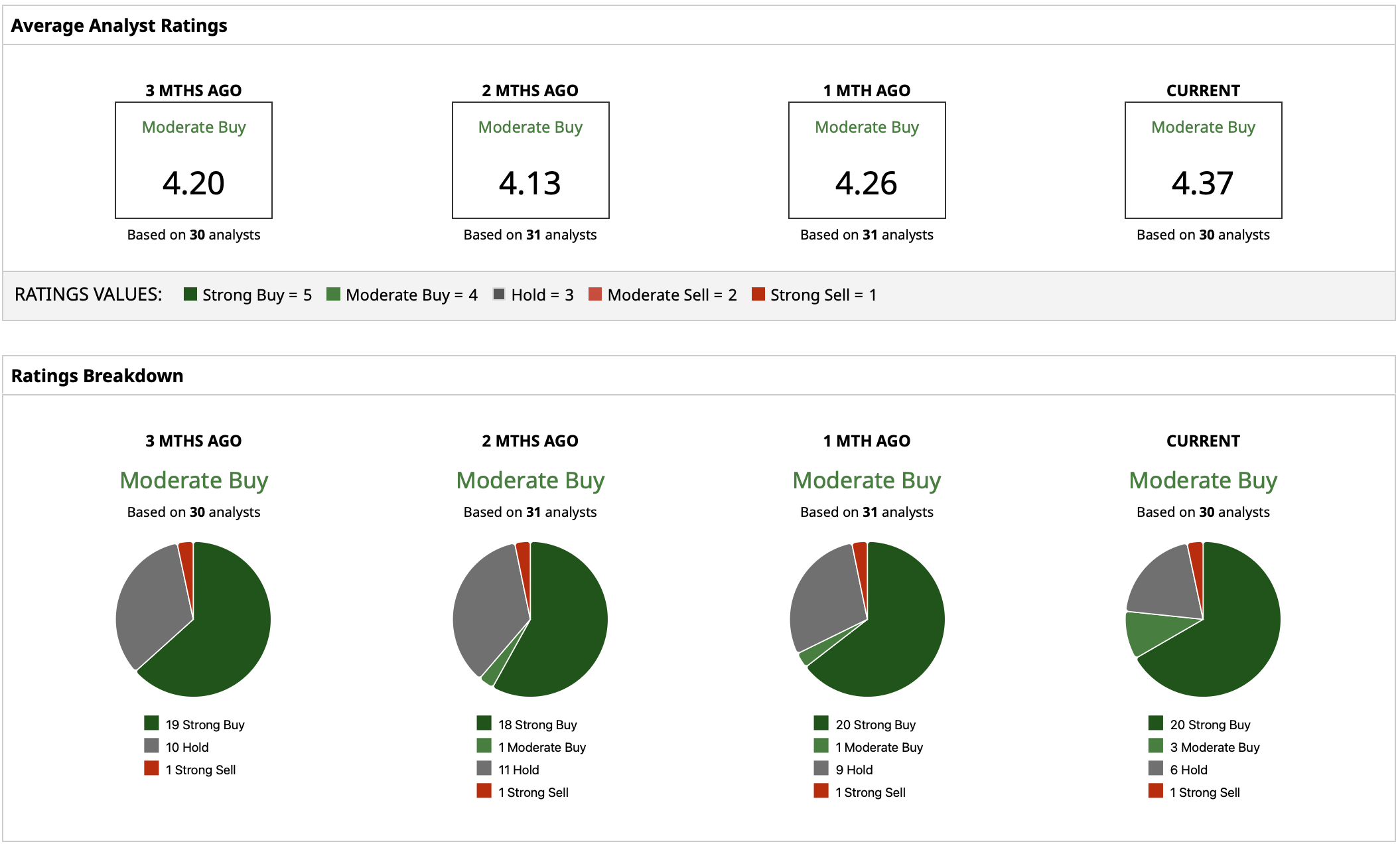

What Do Analysts Expect for ARM Stock?

Analysts' expectations for ARM stock have turned decidedly bullish with a “Moderate Buy” rating consensus, and Needham upgraded ARM stock to “Buy” with a target price of $200. Other analysts also upgraded their expectations for ARM stock in response to Arm's “Arm Everywhere” presentation and its AGI CPU launch.

ARM stock has a mean target price of $171.78. Its highest target is $240. Its current stock price is about $140, a potential gain of about 23% for its mean target and 71% for its high target. Not an insignificant potential gain, but it does suggest that Wall Street believes that ARM can go higher even after its big gain.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)