Chewy (NYSE: CHWY) stock faces headwinds in 2026, as do many retailers. However, its digital-first, asset-light model is working, gaining share as evidenced by its industry-leading growth pace. Chewy consistently outgrows peers and the broader pet-care industry, driven by global digital penetration and a greater focus on nutrition and pet healthcare. The takeaway for investors is that this stock surged by double-digits following an otherwise tepid release, indicating market support and potential for additional gains this year.

Chewy Leads Market in Q4: Guides for Strength in 2026

Chewy had a solid quarter despite the tough comparison to last year and analysts' expectations. The company reported $3.26 billion in net revenue, a 0.5% gain on an as-reported basis and an 8.1% increase on an adjusted basis. The adjustment is for an extra week; Chewy’s strength was driven by a 4% increase in active customers, a 2.2% increase in sales per active user, and a 4.8% increase in autoship sales.

Autoship sales are a critical factor for this business, as they represent sticky, monthly revenue tied to food, medicine, and healthcare products. At 84% of net, autoship provides Chewy with a solid foundation to accelerate growth in 2026 and to provide its investors with clear revenue visibility.

Margin news was mixed. The company widened its margins across the board, driving a 30.4% increase in adjusted EBITDA, a 72% increase in net income, and a 47% increase in free cash flow (FCF), but fell slightly short of expectations.

The adjusted earnings per share (EPS) fell by a penny year over year and was short of the consensus, but was sufficient to enable cash build on the balance sheet while maintaining its low-debt and buying shares.

Chewy’s buybacks aren’t robust, failing to reduce the count significantly in fiscal 2026, but they offset share-based compensation and are likely to be increased over time. Chewy is forecasting margin improvement over time and an accelerated pace of earnings growth. As it stands, the long-term outlook is a high-teens to low-20% compound annual EPS growth rate, which has this stock trading at around 9X its 2031 EPS forecast. While there is concern about Chewy’s valuation today, this metric suggests a 100% upside potential over the next few years.

Guidance was the trigger for CHWY’s post-release price action. The company’s revenue forecast was as expected, and its earnings outlook was optimistic. The company forecasts FY2027 adjusted EPS in the range of $13.68, nearly a dime better than MarketBeat’s reported consensus.

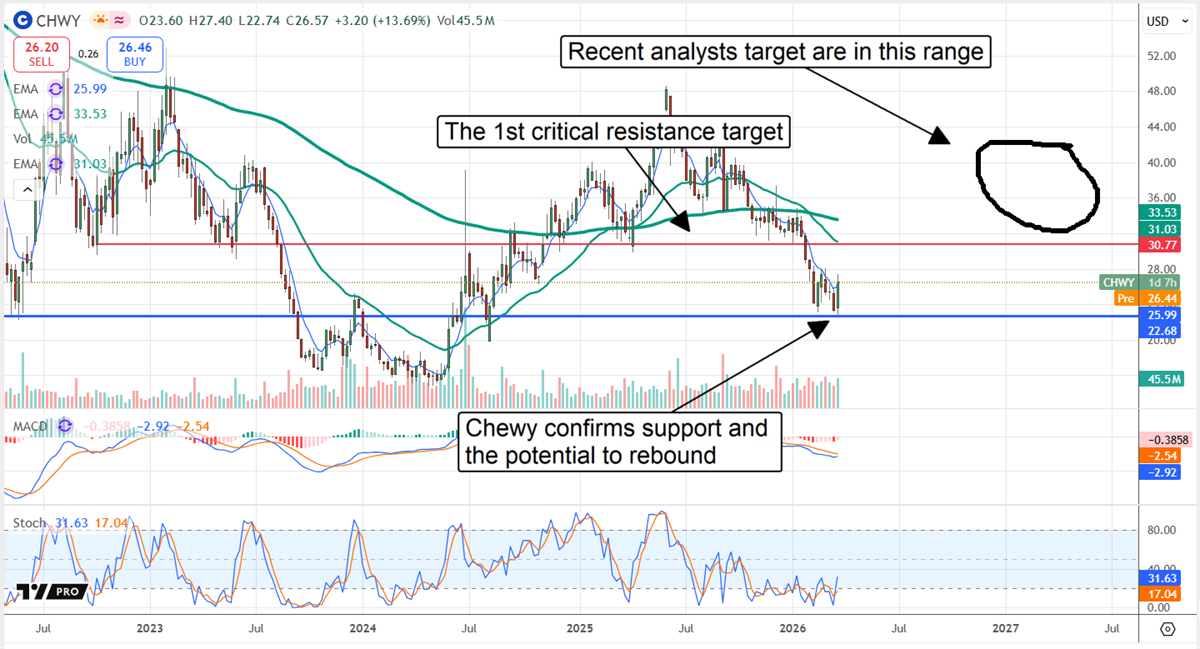

Analysts Put Bottom in Chewy Stock: Institutions Pose Risk

The analyst response following the release was as mixed as the results, with the early updates including positive chatter, focused on earnings strength and 2026 guidance, offset by price target reduction. The net result is that Chewy’s Moderate Buy rating and 80% Buy-side bias are intact, but the consensus price target was moderated. The consensus price target forecasts approximately 60% upside this year; however, investors should note that price target revisions following the release have been in the low end of the range.

Even so, the new targets suggest at least some upside is possible, with most in the 20% to 50% range. These targets affirm Chewy stock's potential to rebound, setting the stage for positive revisions later this year. In this scenario, Chewy continues to build on its momentum and outperforms in the upcoming quarters.

Institutions are among the risks. The group owns more than 90% of Chewy stock and sold it in early Q1. If this trend continues in Q2 2026, CHWY stock will struggle to advance past critical resistance levels. The critical resistance level as March comes to a close is near $20.75 and is likely to be reached before the quarters end. The opportunity is that institutions revert to accumulation, strengthening the market bottom and creating a potential for a rebound.

Chewy’s catalysts include the execution of its high-margin strategies. They include Chewy Vet Care, private label expansion, AI, and its advertising business. Chewy enables product manufacturers to advertise directly to consumers on a pay-per-click basis and uses AI to drive efficiency across its digital ecosystem. Private labels are a growing business, driving not only margin but enabling market share gains versus premium brands.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "Chewy Gobbles up Market Share in 2026: Poised to Advance in Q2" first appeared on MarketBeat.

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Quantum%20Computing/A%20concept%20image%20showing%20a%20ray%20of%20light%20passing%20through%20cyberspace_%20Image%20by%20metamorworks%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)