Shares of Lumentum Holdings (LITE) have delivered extraordinary performance in recent months, more than doubling year-to-date (YTD) and rising 1000% over the past year. The sharp appreciation has been largely driven by robust demand linked to artificial intelligence (AI) applications, which has significantly strengthened the company’s growth outlook. Moreover, its inclusion in the S&P 500 ($SPX) boosted investors’ sentiment around the stock.

Lumentum specializes in optical and photonic products that serve a range of high-growth end markets, including cloud computing, AI and machine learning (ML), telecommunications, and consumer and industrial applications. The rapid expansion of AI and ML workloads has intensified data traffic within cloud data centers, accelerating the adoption of advanced optical components and modules. This structural shift in data infrastructure demand has positioned Lumentum to deliver strong growth.

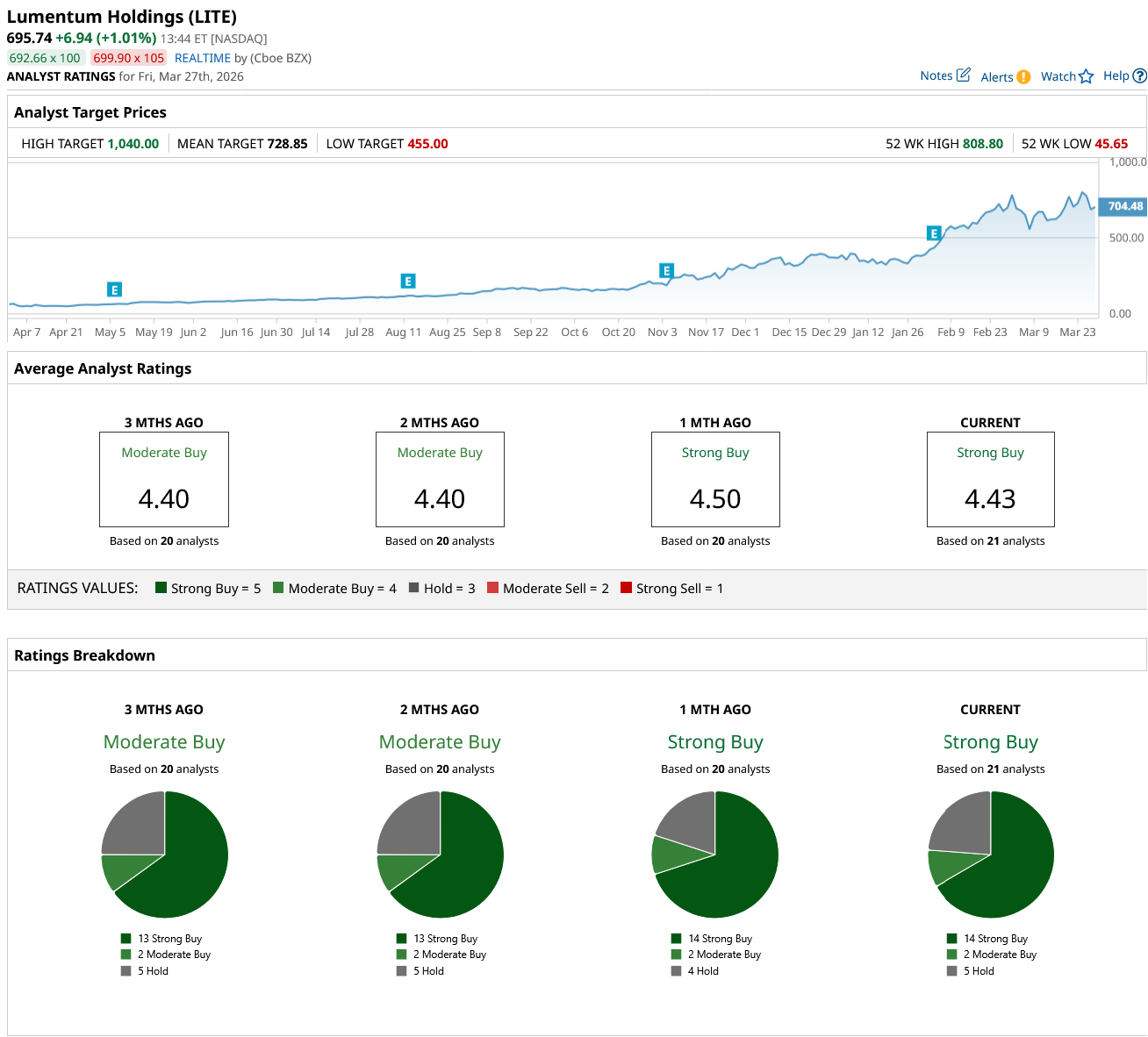

Despite the stock’s substantial rally, sentiment on Wall Street remains positive. Analysts continue to highlight the company’s exposure to long-term AI-driven demand as a key investment driver. Notably, at least one analyst has a 12-month price target of $1,040 for LITE stock. Based on the recent closing price of $688.80, this projection implies a potential upside of about 51%.

Lumentum’s Growth Is Accelerating

Lumentum is in a solid growth phase, supported by strong operating performance and expanding demand across key optical technologies. The company reported a strong second quarter, delivering more than 65% year-over-year (YoY) revenue growth alongside a significant improvement in adjusted operating margins. Its forward guidance indicates that Lumentum’s growth is likely to accelerate. March quarter revenue is projected at approximately $805 million, implying YoY growth of more than 85%.

Supporting Lumentum’s growth are three primary catalysts, including cloud transceivers, optical circuit switches (OCS), and co-packaged optics (CPO). While cloud transceivers remain the dominant contributor to current results, Lumentum is increasingly unlocking the long-term potential of OCS and CPO. At the same time, the company continues to benefit from consistent execution in its foundational components business, including laser chips for cloud applications and specialized data center interconnect solutions.

Demand for OCS is strengthening meaningfully, supported by both technological complexity and Lumentum’s ability to scale production. The company’s backlog has exceeded $400 million, with most shipments expected in the second half of the year. The backlog provides strong visibility into near-term revenue growth.

Cloud transceivers are also performing well, with revenue exceeding historical run rates and maintaining solid momentum. Operational efficiencies, including higher yields and reduced scrap rates, are further supporting profitability in this segment.

In CPO, Lumentum has secured additional multi-hundred-million-dollar orders for ultra-high-power lasers, with shipments expected to begin in the first half of 2027. The company is also expanding into external light source (ELS) modules, which broaden its addressable market and enable more integrated solutions for customers adopting next-generation architectures.

Across its broader portfolio, Lumentum continues to see sustained demand in long-haul, interconnect, and cloud-related applications, with several product lines delivering strong YoY growth. Systems revenue also increased sharply, driven primarily by cloud transceivers as manufacturing capacity ramps stabilized.

Looking ahead, Lumentum expects to deliver strong revenue growth across both components and systems. Its strong product portfolio positions it to benefit from ongoing structural shifts in data center connectivity.

Will LITE Stock Hit $1,040 in 12 Months?

Lumentum has a solid growth trajectory, driven by AI-led expansion of its data infrastructure. It is executing effectively across its core businesses while positioning itself in next-generation optical technologies such as OCS and CPO, which could meaningfully expand its total addressable market over the medium to long term. Strong revenue growth, improving margins, and a visible backlog strengthen its prospects.

While LITE stock has rallied significantly, a $1,040 price target over the next 12 months is not unreasonable, especially amid strong demand trends and an expanding backlog.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)