The S&P 500 heads into Friday trading down 0.45% after the previous four days of trading. The futures point to a lower open this morning on ongoing concerns about the war in the Middle East.

News reports that the White House and Pentagon are considering sending another 10,000 combat troops to the region won’t do the markets any favors. An escalation of tensions will undoubtedly ratchet up the VIX index, which sits slightly under 30 as I write this pre-market.

Handicapping what President Trump will do has never been easy, so I won’t even try. All I know is that troops on the ground in Iran likely means the U.S. casualty numbers will go up, perhaps dramatically. Let’s hope it doesn’t come to that.

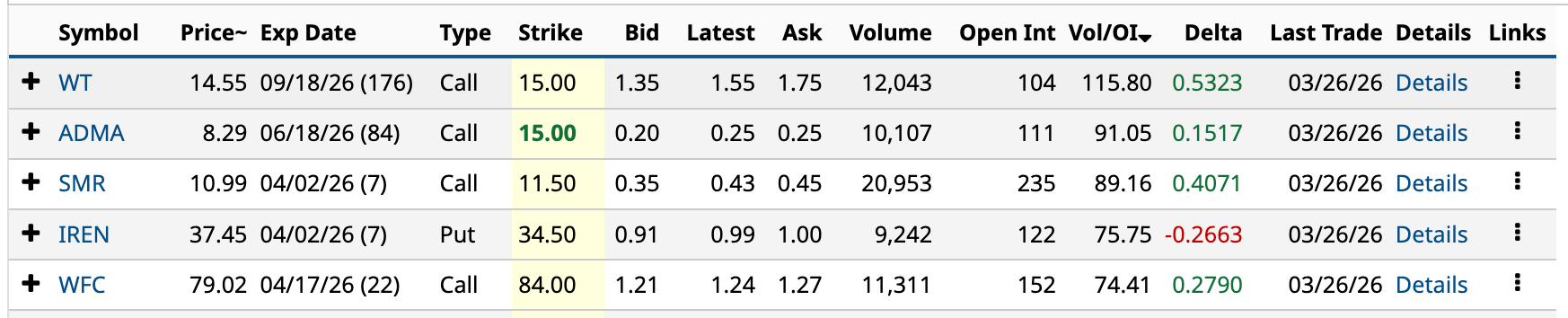

In yesterday’s unusual options activity, asset manager WisdomTree (WT) led the way with a Vol/OI ratio (volume-to-open-interest) of 115.80 -- based on options expiring in seven days or more -- considerably more than the second-highest at 91.05.

The top 5 unusually active options from Thursday’s trading

I’ve been bullish about WisdomTree for several years. It appears to be finally coming into its own in the highly competitive asset management industry.

WisdomTree’s unusual options activity provides a compelling argument for why investors should pass on BlackRock (BLK) and opt for this much smaller competitor.

Have an excellent weekend.

The Option in Question

It’s not often you’ll see an asset manager leading the way in unusual options activity. The Sept. 18 $15 call’s volume of 12,043 was 8.3 times higher than its 30-day average of 1,457. The call accounted for 49% of its total volume on the day, the highest single-day volume in the past three months, three times the second-highest.

All that to say, it was a very unusual day. What prompted it is the question du jour.

Possible Reasons for the Unusual Options Activity

It could be the lingering effects of its March 16 announcement that it was acquiring Atlantic House Holdings Limited, a UK-based asset manager specializing in defined outcome and derivatives-driven investment strategies. The firm has $5.5 billion in assets under management (AUM).

The acquisition broadens WisdomTree’s capabilities while expanding the presence of its Models and Portfolio Solutions business in the UK wealth market.

WisdomTree paid $200 million for the firm. That’s 3.6 times the firm’s AUM. While that’s high -- BlackRock’s market cap is 1.1% of its $14.04 trillion in AUM -- the specialized nature and strategic value of the acquisition justifies paying up for the UK firm.

“This transaction also advances our multi-year strategy to build a more diversified and higher-quality growth platform, expanding on WisdomTree’s 2025 acquisition of Ceres Partners, LLC and our strategic entry into private markets,” stated WisdomTree CEO and founder Jonathan Steinberg in the company’s acquisition announcement.

Another possibility is the recent launch of the WisdomTree Tech Megatrends UCITS ETF in Europe. This tech fund invests across eight disruptive themes, including artificial intelligence, blockchain, cloud computing, cybersecurity, quantum computing, and others.

The launch marks its 15th thematic ETF in Europe since it entered thematic investing in 2018. The unit has $9 billion in AUM and has attracted $5.8 billion in inflows since the beginning of 2025.

One thing I’ve always liked about WisdomTree is its ability to do things slightly differently from other peers in the asset management industry.

This new ETF uses a three-tiered approach to outperform benchmark indices. While passively managed -- it tracks the performance of the WisdomTree Tech Megatrends Equity UCITS Index -- the process starts by rating sub-investment themes, such as AI, on a conviction scale of High, Medium, and Low. The low-conviction stocks are excluded from consideration. It then applies a tactical thematic asset allocation approach, overweighting sub-themes deemed more positive at any given moment. Finally, it uses experts to identify the up-and-coming companies for each sub-investment theme.

Its process isn’t earth-shatteringly different, but it's enough to allow it to gather new assets relatively quickly.

Lastly, while only seven analysts cover its stock, five of them rate it a Buy (4.43 out of 5), with a target price of $19.04, well above its current share price. As WisdomTree continues to scale its business while differentiating itself from other players, more analysts will follow it.

Why WisdomTree Over BlackRock?

It comes down to valuation. By most metrics, WT is cheaper than BLK.

For example, analysts expect WisdomTree to earn $1.12 a share in 2026 and $1.22 a share in 2027, according to S&P Global Market Intelligence. Its stock trades at 13.0 and 11.9 times these estimates. BlackRock’s P/E multiple based on the 2026 estimate is 17.9x and 15.7x 2027’s EPS estimate, 34% higher than WisdomTree’s.

Another example is EV/Revenue (enterprise value to revenue). WisdomTree’s is 3.91x compared to 5.6x for BlackRock; the former’s 30% lower than the latter’s.

The one area where BlackRock outshines WisdomTree is on the balance sheet. That’s what happens when you only have $158 billion in AUM compared to BlackRock’s $14 trillion. For example, WisdomTree’s net debt is 2.9 times its EBITDA (earnings before interest, taxes, depreciation and amortization), while BlackRock’s is a meager 0.1x. That’s what scale does for you.

However, when it comes to revenue and earnings growth, BlackRock can’t hold a candle to WisdomTree. The company’s three-year compound annual growth rate (CAGR) for revenue and EBIT (earnings before interest and taxes) are 17.9% and 43.9%. That compares to 10.7% and 9.7% for BlackRock.

Right now, despite WisdomTree’s share price gaining 56% over the past year, you can get more growth than BlackRock on both the top and bottom line, but pay less for that growth.

WisdomTree could be the ultimate GARP (growth at a reasonable price) stock.

Back to the Unusually Active Call

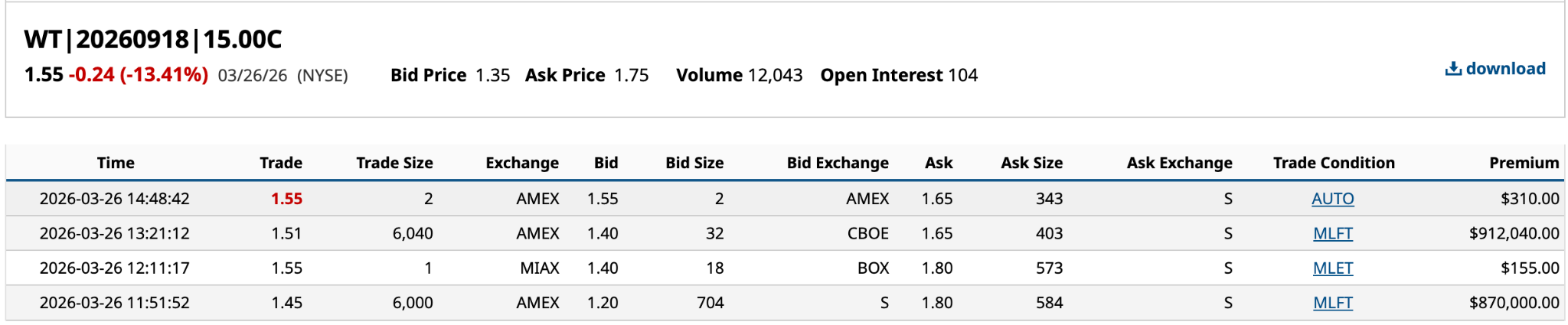

The Sept. 18 $15 call’s 12,043 in volume consisted of four trades, two of which accounted for all but three of the call contracts. There’s a good chance that both the 6,000 and 6,040 trades were made by the same person.

With a DTE (days to expiration) of 178, the trade prices of $1.45 for the 6,000 and $1.51 for the 6,040, and their breakevens of $16.45 and $16.51, are 13.1% and 13.5% higher than yesterday’s $14.55 closing price. With an expected move of 9.23%, they’ve got their work cut out for them. That said, both calls cost about 10% of WisdomTree’s share price, so the downside isn’t significant. It’s a good use of leverage.

You’ll see, however, that the trades were part of multi-leg trades, so they weren’t basic long calls. Several options strategies come to mind.

However, after tracking down the other legs of the 12,040 calls, I’ve concluded that the trader used a custom diagonal ratio call spread. It involved buying 6,000 Sept. 18 $15 calls at 11:51 yesterday. At the same time, the trader sold 3,000 June 18 $15 calls and 3,000 June 18 $12.50 calls for premium income to offset the cost of the long calls.

So, the cost of the 6,000 Sept. 18 $15 calls was $870,000, while the premium generated from the 3,000 June 18 $12.50 and 3,000 June 18 $15 calls was $1.035 million for a net credit of $165,000.

So, the cost of the 6,000 Sept. 18 $15 calls was $870,000, while the premium generated from the 3,000 June 18 $12.50 and 3,000 June 18 $15 calls was $1.035 million for a net credit of $165,000.

The trade at 1:21 yesterday afternoon, which involved buying 6,040 Sept. 18 $15 calls, and selling 3,020 June 18 $12.50 and 3,020 June 18 $15 calls, generated a net credit of $166,100. That’s $331,100 for both multi-leg trades.

What’s the risk of such trades?

Let’s say the shares hit $18 by June 18. The buyer of the $15 and $12.50 calls exercises their right to buy WisdomTree shares. The trader would have to buy shares for $18 and transfer them to the buyer of calls. That could cost millions.

However, let’s say the trader already owns the 1.204 million WisdomTree shares, and they were acquired in the March 2020 correction when they traded under $3. They transfer those shares to the buyer, who pays $12.50 and $15 per share, for a smaller gain but still a big one.

They still have the long calls and three more months of potential appreciation, plus the $331,100 in premium from selling the short calls.

These are issues that small retail investors likely will never have to deal with.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)