Protect Your Profits Before the Next Crash (Get Paid to Hedge Your Stocks)

You’d think if a stock has already made you money, the hard part would be over. But then volatility picks up, the stock starts sliding, and the real mistake could be actually doing nothing. One sharp drop can wipe out months, even years, of gains, and that’s where a protective collar can save the trade.

In this article, I’ll show you exactly when the strategy makes sense, how the trade is built, and what you gain and give up, before you place your trade.

So, first, let’s talk about when you should use protective collars. Because knowing HOW is all well and good, but knowing WHEN allows you to use it strategically.

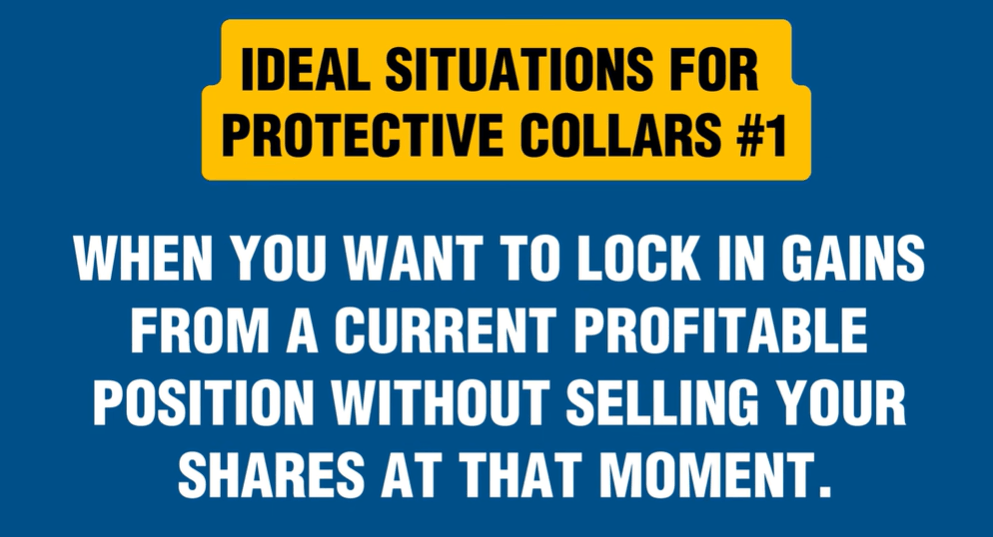

First, protective collars are most useful when you already own shares that have gone up in value and want to lock in gains without selling. Maybe you’re afraid of further downside because of recent geopolitical events, or maybe you’ll need to sell the stocks to pay for something, perhaps within the year. With protective collars, you’re protecting yourself against sharp market drops.

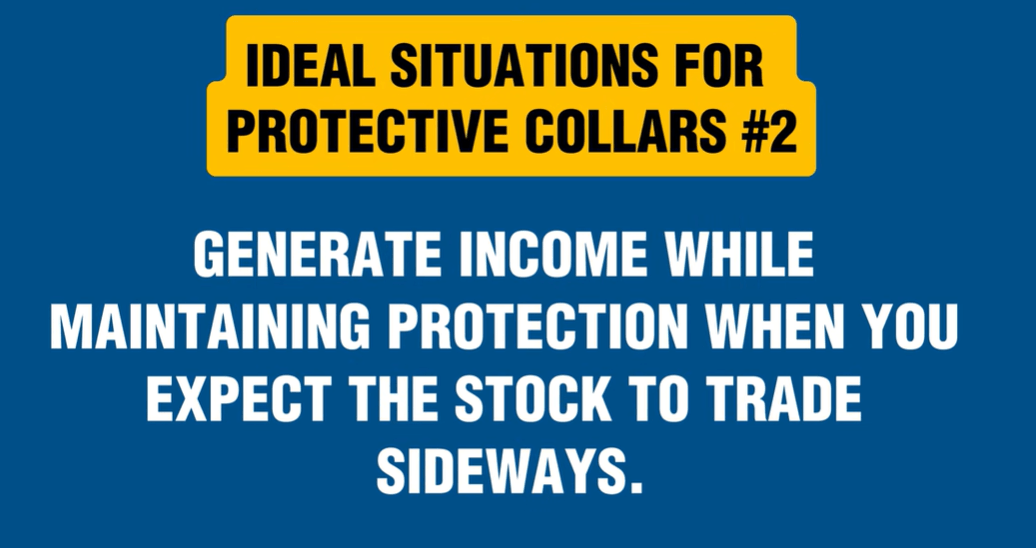

Also, collars can be valuable when you expect a stock to trade sideways.

Third, they’re helpful when you’re looking for a low-cost hedge when you expect higher volatility. Think of earnings seasons, events, or market announcements that can send the stock up or down.

Whatever the reason, the strategy provides downside protection by giving up a little upside.

So now, let’s pick apart what a protective collar is.

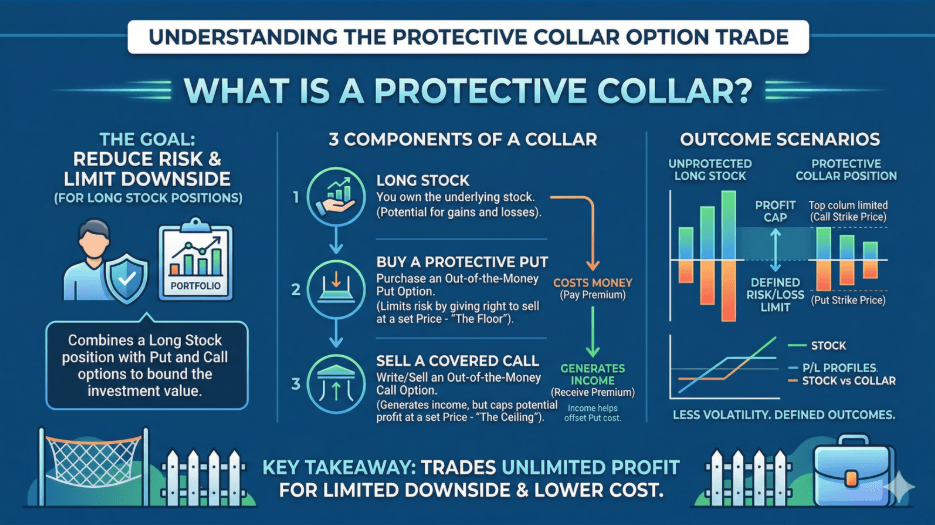

A protective collar is an options strategy where an investor who owns at least 100 shares of a stock or etf buys a put option to limit their downside risk and simultaneously sells a covered call to generate income. This helps cover the cost of the put, sometimes entirely. That means investors can get downside protection for free, or even get paid for it.

So what’s the catch?

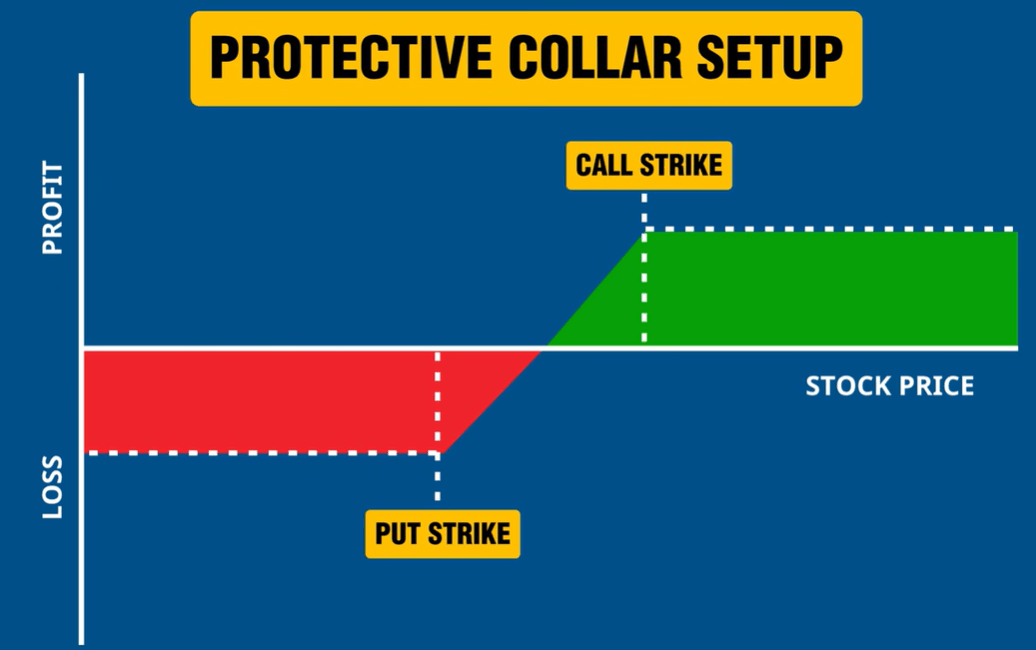

Well, the put creates a floor, and the call creates a ceiling. So you get downside protection beyond a certain point at the expense of capping potential upside.

Let’s use a real-world example.

Say you bought 100 shares of stock years ago, when it was trading around $300. And the stock got as high as $500 - but now, it’s trading at around $400.

And now, you’re worried it could fall further, and you’ve had enough.

A protective collar can be an inexpensive way to protect that position.

First, you decide on the long put’s strike price, which will be the floor. This should be the level you’re comfortable selling the stock if the price continues to decline.

So in this case, let’s say it’s $395. That’s your protection level.

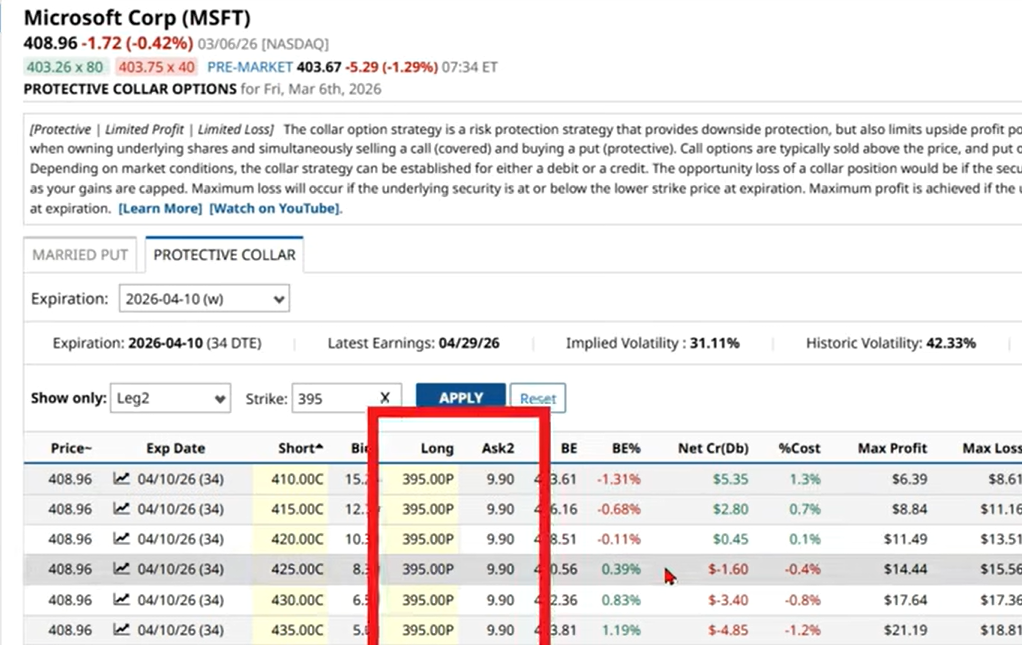

So, now that you have a starting point, let’s jump on over to stock’s profile page and click protection strategies, and then click the protective collar tab.

Now, we need to decide on an expiration. How long are we going to get protection for? A day? A week? A month? A year? The longer the expiration, the more expensive it’ll be. With protective collars, I usually find that somewhere between four and six weeks is the sweet spot.

So, I’ll change the expiration date to April 10, which is 34 days away from the time of writing.

Next up, we’ll want to change the strike selection here in Leg 2, to 395, and click Apply. Leg 2 is your long put - which creates the floor.

And there we have it, a selection of protective collar trades. Right now, a 395-strike puts costs $9.90 a share or $990 for the contract. That would be your total cost for protection if you were only using a long put.

By the way, if you want to learn more about long puts and how you can profit from them, you can watch this video.

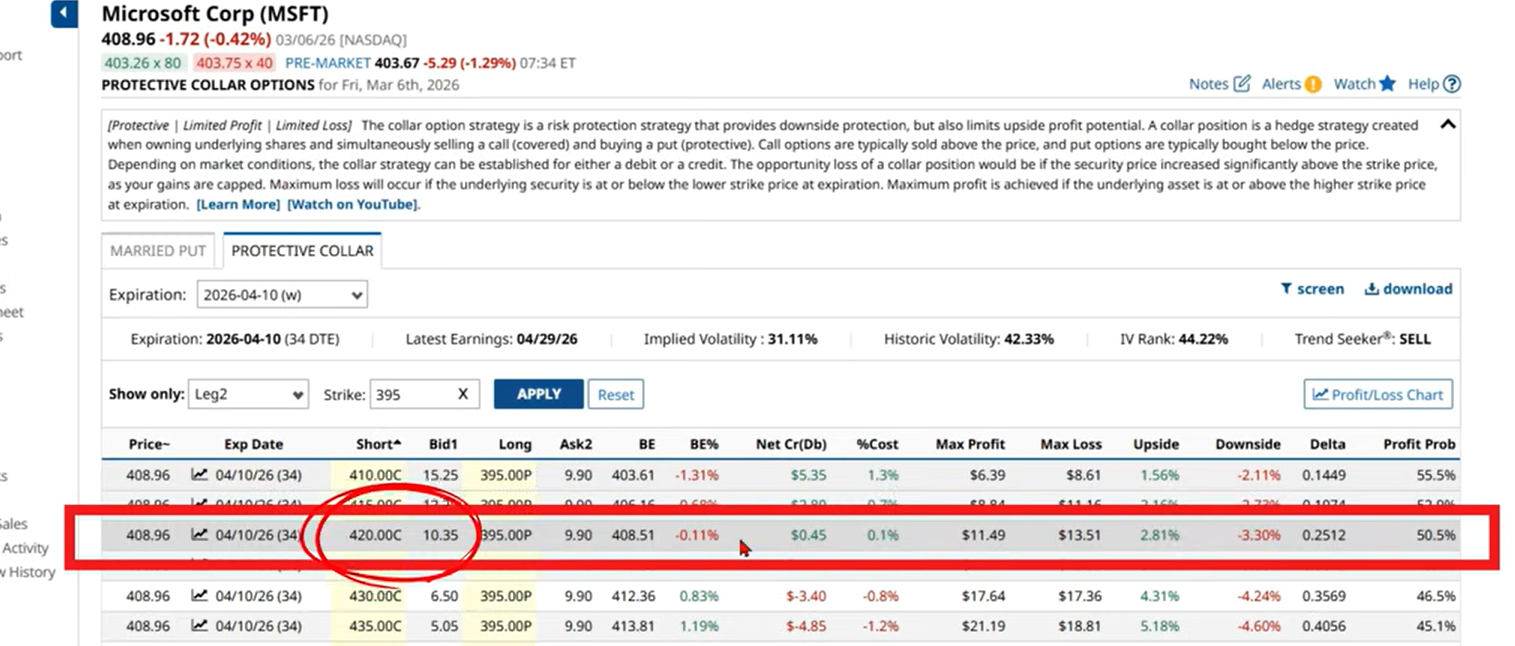

Now, the other leg will help subsidize the cost of the put, that’s the covered call.

You can even look for trades that more or less eliminate the cost of the long put. So, here we see 420-strike call would net us $10.35 a share, and the 425 strike would get us 8.30. For the purposes of this example, I’ll use the 420 strike.

Also, if you want to know more about covered calls, we recorded an entire video about it.

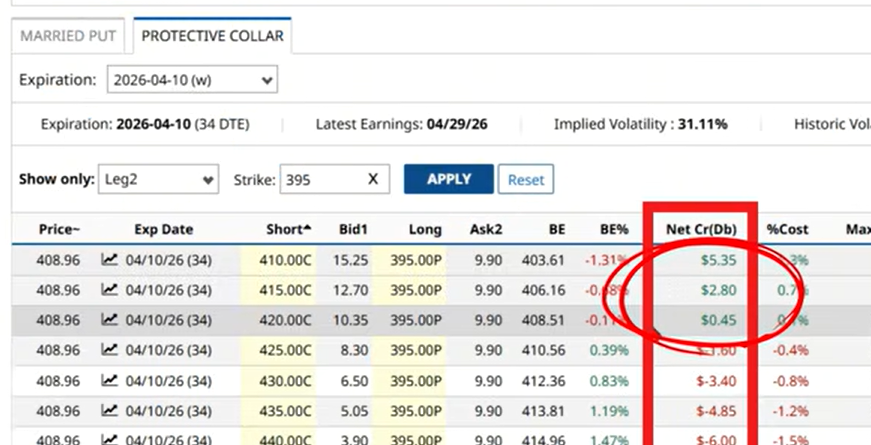

So, to calculate the total cost of the protective collar, subtract the cost of the long put from the premium you received from the short call. Or, you can check the Net Cr(Db) column on the Protective Collar screener. Green means it’s a credit, you get paid. Red means it’s a debit, it means you pay. And multiply it by 100 to get the contract price.

So in this example, this trade starts at a 45-cent credit per share, or $45 total. And you’re essentially getting paid to protect your Microsoft shares if they trade below $395 at or before expiration.

Let’s fast-forward to expiration: what if Microsoft didn’t move much, say it trades between the $395 and $420 strikes?

Well, in that case, both your options expire worthless, and you get to keep that $45 credit and your 100 Microsoft shares.

This is often the best outcome for someone selling a protective collar: to keep and protect their shares from downside, while subsidizing the cost of protection.

After that, you can set up another protective collar if you want. Or if the markets have improved, you might consider a different strategy. The point is, you still have your 100 shares and the flexibility to do as you please.

But what if the stock actually moved below 395 at expiration? Say Microsoft trades at $350 now. Well, in that case, now your long put will be in the money. And it’s going to be worth more than you paid. In this case, it’ll have $45 of intrinsic value. More or less, that’ll be the premium for the put.

So, you have choices here. You can sell the put for about $45 a share, or exercise it and sell your shares for $395 each if you no longer want them. Either way, your P&L is the same.

Now, there’s one thing to remember: options have time value baked into the premium as well, so if you decide to sell the put while it still has intrinsic and time value, you could receive a higher premium by closing out your trade, rather than waiting until expiration. But that will always depend on the current market conditions. For example, volatility may be declining. In any event, for this type of trade, it’s often best to wait it out.

But what if, at expiration, Microsoft trades above $420 - your short call strike?

Well, you’ll get assigned. It means you’ll sell 100 Microsoft shares for $420 each. And that’s the thing: it’ll happen regardless of how much the stock is trading for at expiration. Microsoft could be at $450, $500 even $1,000. Selling protective collars means getting downside protection at the expense of giving up a little upside.

But what if you wanted a little more flexibility - for example, maybe you’d accept a lower floor and higher ceiling? Well, the good thing about protective collars is that you can always pick the strikes.

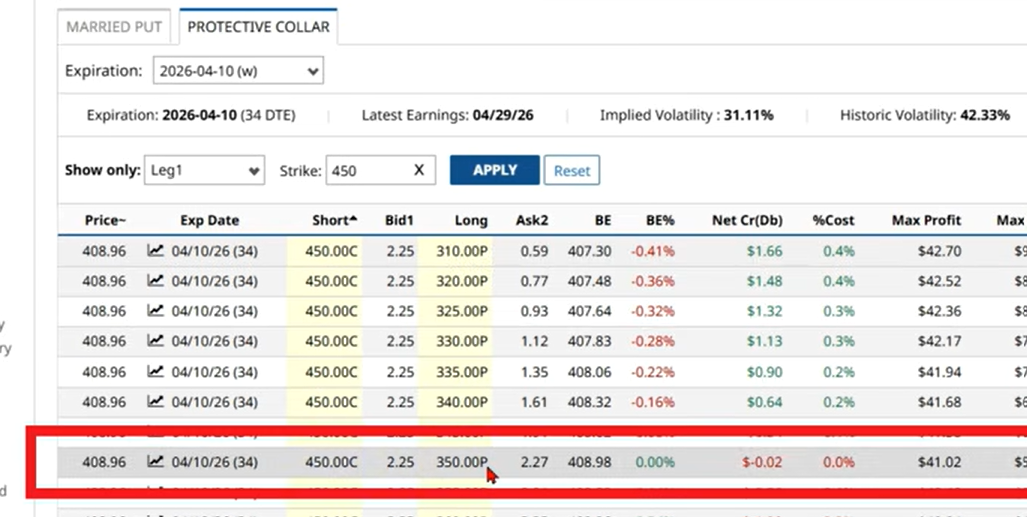

So let’s say you’d be fine capping your upside at $450 while protecting your shares below $350.

This time we can search using leg 1, which is the short call strike, type in 450, click apply, then look for the trade that has a 350-strike put.

According to the screener, you can sell a 450-strike call on Microsoft for $2.25 and buy a 350-strike put for $2.27.

That brings your net debit to 2 cents per share or just two bucks for the trade. This time, you’re paying a small amount for protection.

If Microsoft trades above $450, you sell your 100 shares at that price. If it trades below $350, say at $300 or $200 or whatever it might be, you still sell the shares at $350. Simple as that.

By the way, if you want a quick reference guide for trading protective collars, you can find a free downloadable cheat sheet here.

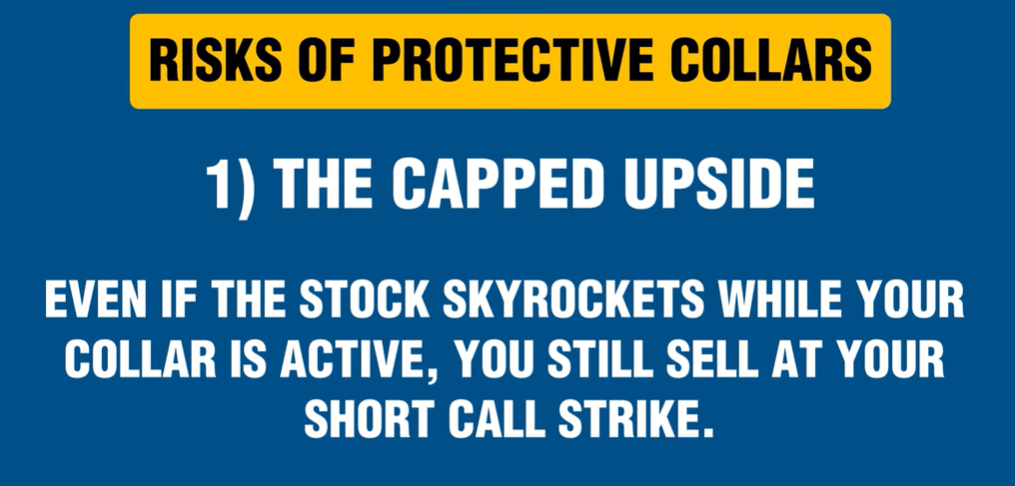

Let’s now cover one of the most important topics about the strategy: the risks of protective collars. The most obvious trade-off is that your upside is capped. If the stock skyrockets while your collar is active, your profit is capped at your short call strike.

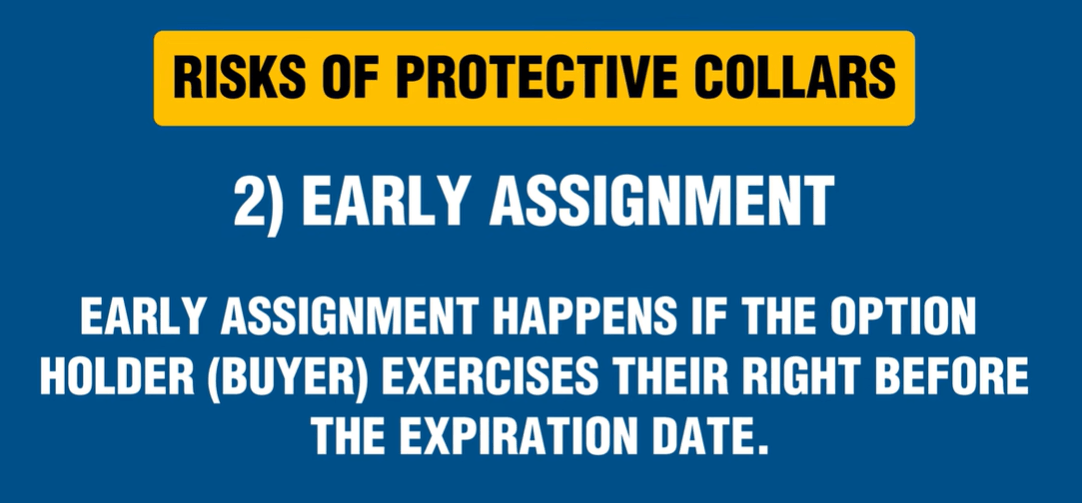

Also, when you sell options, there’s always the risk of early assignment. Early assignment happens when the option holder exercises it before expiration. That means you will be forced to sell your 100 shares to fulfill the obligation on your short call. It’s an automated process. You don’t get a choice. No one picks up the phone and calls you - it just happens in your brokerage account.

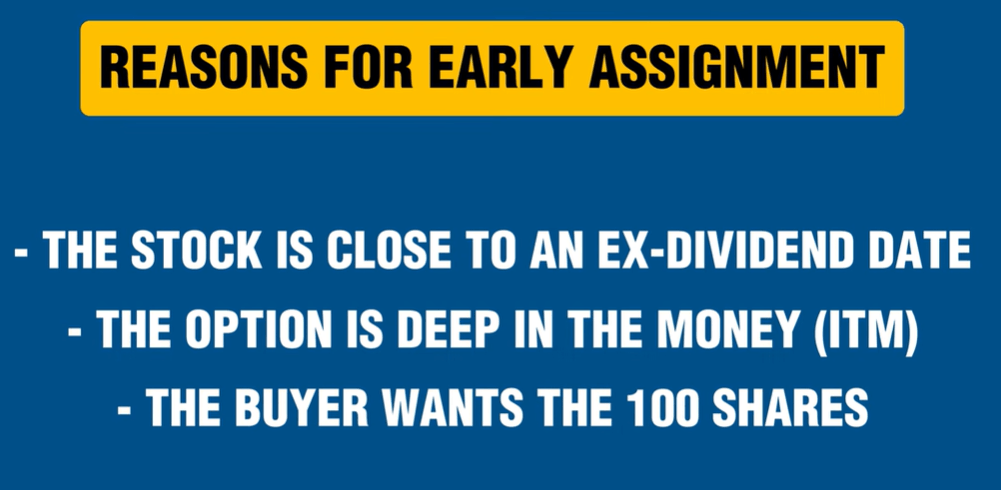

The most common reasons for early assignment are when the stock is about to reach an ex-dividend date, when the call is deep in the money, and there’s profit to be made, and the buyer wants to get those 100 shares.

If it happens, your collar collapses. The short call and the associated stock position disappear, but you get paid 100 times the strike for each contract, and you’re still left with the long put. Now, if the call option was exercised because it was in the money, the put will most likely have very little value left, especially if there’s little time remaining until it expires. You could still either sell it or just let it expire. You never know with the markets today; it may turn around by expiration.

Lastly, there may be some tax implications when you set up a protective collar, because this strategy involves offsetting positions. For example, if you’re in the US, the trade may fall under Section 1259 of the Internal Revenue Code.

Of course, that’s beyond the scope of this video - for further questions about tax, always consult a qualified tax advisor.

The protective collar is one of the most powerful strategies for protecting your shares at a low cost. Actually, in some cases, you might even get paid to enter the trade.

But, then again, protection is never free. If you’re not paying in dollars, it means you’re paying in capped upside. The key is knowing when it makes sense to use a collar and setting your strikes thoughtfully so the protection fits your goals.