Fertilizer prices are going up as a result of tensions in the Middle East, with a continued closure of the Strait of Hormuz restricting the supply of natural gas. Natural gas is vital in the production of ammonia, urea, and urea ammonium nitrate (UAN), among other things. In fact, natural gas accounts for as much as 90% of the cost of ammonia. Similar supply shocks are possible in the manufacturing of sulphur-based fertilizers, as sulphur is a byproduct of oil refining and natural gas processing. These supply-chain issues are expected to bring windfall profits for fertilizer manufacturers as fertilizer prices soar.

Two of the companies set to benefit from this price surge are CVR Partners (UAN) and Intrepid Potash (IPI). CVR Partners specializes in nitrogen-based fertilizers, while Intrepid Potash offers potassium-based products. Bank of America Securities recently pointed out that these windfall profits will benefit fertilizer stocks in the short term, but analysts were quick to add that they don’t change the fundamentals of the industry. In other words, this is a cyclical spike, and things could normalize as soon as the Iran war comes to an end. The opportunity could be short-lived, but it is there.

Fertilizer Stock # 1: CVR Partners (UAN)

CVR Partners is a pure-play nitrogen fertilizer player. It produces two key products — ammonia and UAN — both of which are essential inputs for crop production. The company runs two major plants, one in Coffeyville, Kansas, and another in East Dubuque, Illinois. CVR Partners is headquartered in Sugar Land, Texas.

UAN stock is up 36% in the last one month while the broader market has produced negative returns. This short-term boost has come on the back of windfall profits that are anticipated as a result of supply disruptions in the fertilizer industry.

The rally in fertilizer stocks has made UAN stock’s valuation rather unfavorable. However, it still offers a trailing 12-month dividend yield of 7.81%. With $69.2 million in cash and around $100 million in free cash flow, the company can continue paying the dividend, although long-term debt of $548 million means CVR is stretched and could face problems down the road if it continues paying the dividend at this rate.

CVR Partners' price-to-sales (P/S) ratio of 3.6 times is also well above the materials sector average and the company’s own five-year average. This premium suggests that UAN stock could revert to its mean as soon as the geopolitical issues subside, which makes it a risky bet at the current valuation.

The company announced fourth-quarter 2025 earnings on Feb. 18, reporting net sales of $131.1 million in the quarter and a loss of $10.2 million. During the ongoing quarter, management expects a 95% to 100% ammonia utilization rate. Demand was expected to be strong even before the Iran war began. Management’s plans for debottlenecking projects are likely to continue as it targets a consistent 95% utilization rate, excluding turnarounds.

UAN stock is not covered by Wall Street analysts tracked by Barchart. However, recent comments from Bank of America give insight into companies that produce nitrogen-based fertilizers like CVR Parnters. BofA analyst Matthew DeYoe has already raised earnings estimates across the sector, citing tightening supply as the primary reason for price increases and, as a result, improved earnings. UAN stock appears to be a beneficiary of the same bull thesis.

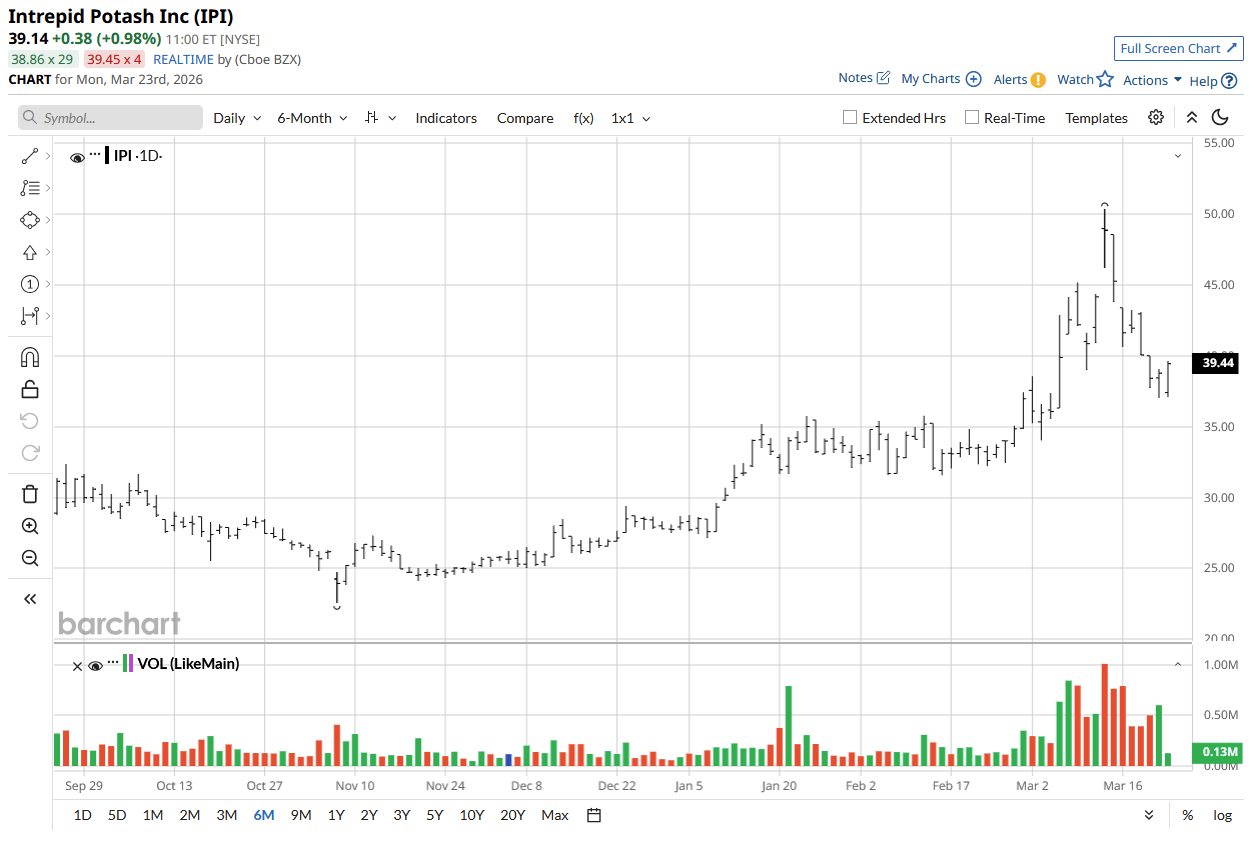

Fertilizer Stock # 2: Intrepid Potash (IPI)

Intrepid Potash produces potash and specialty nutrients used primarily as input in agriculture. Intrepid is the largest producer of potash in the United States, with production dominated by its facility in Carlsbad, New Mexico. The company is headquartered in Denver, Colorado.

IPI stock's returns are slightly muted next to UAN, returning 27% in the last one month. Since the company’s primary potassium product isn’t directly impacted by supply-chain issues, IPI has not rallied as much as other fertilizer stocks. However, it is still a beneficiary of the price increases because when farmers can’t get their hands on expensive nitrogen-based fertilizers, demand for alternative nutrients increases, and that's exactly what Intrepid Potash specializes in.

With IPI stock currently trading at a forward P/E of 33.9 times, there is a premium investors are paying right now. A similar premium can be seen through various other valuation metrics, with many hovering above the company’s five-year averages. Interpid Potash also doesn't pay a dividend, so investors hardly have any security in case fertilizer prices normalize. This also confirms that the opportunity in fertilizers is a short-term one for most market participants.

The company announced its Q4 2025 earnings report earlier this month. For the full year, IPI reported net income of $11.2 million, a welcome development against the net loss of $212.8 million in 2024. For Q1 2026, the company expects sales of 100,000 tons of potash at the midpoint. Management highlighted estimated capital expenditures of $40 million to $50 million for 2026 as well.

On March 5, UBS analyst Joshua Spector raised his price target on IPI stock from $24 to $25 while maintaining a “Sell” rating. Because this target remains significantly below the current price, it can be argued that most of the benefit from supply disruptions has already been priced into shares.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)