Stablecoins have become a mainstream digital asset. As the cryptocurrencies pegged to reserve assets gain prominence, so do their flows. Bloomberg Intelligence estimates that global stablecoin payments will reach $56.60 trillion by 2030. However, compliance regulation frameworks have been slow to move. In the U.S., the GENIUS Act establishes a federal framework that subjects the use of payment stablecoins to federal banking regulation.

Stablecoin issuer Circle Internet Group (CRCL) dropped by a whopping 20.1% intraday on March 24 as investors reacted to the latest version of a bill called the Clarity Act. The new legislation could limit the yield on stablecoin balances.

Basically, stablecoins like Circle’s USDC earn yield, providing an incentive to hold them, just as cash sitting in a bank earns interest. On the other hand, the new bill could enable activity-based rewards, for instance, by incentivizing the use of stablecoins for payments, trading, or lending.

Against this backdrop, should you buy the dip in Circle’s stock?

About Circle Stock

Headquartered in New York City, Circle operates as a leading payments technology company focused on building a new internet financial system. It issues stablecoins pegged to major currencies and provides infrastructure for blockchain-based applications, enabling faster cross-border payments, tokenized transactions, and institutional financial services.

The company acts as a stablecoin clearinghouse, fostering secure, transparent global economic interactions through its digital asset platform and network utilities. It has a market capitalization of $24.97 billion. Circle’s stock went public last year in a successful IPO, soaring 168% on its debut day.

However, Circle’s stock has declined 17.1% over the past six months, amid regulatory concerns, execution risks with its Arc project, growing stablecoin competition, and heavy investment spending. The stock reached a six-month high of $159.47 in October 2025, but is down 34.3% from that level. It dropped to a six-month low of $49.90 on Feb. 5, but is up 109.5% from that level. Over the past five days, Circle’s shares declined 22.2%.

On a forward-adjusted basis, Circle’s price-to-earnings ratio of 110.75 times is significantly higher than the industry average of 28.74 times.

Circle Reports Q4 Results Amid Strategic Stablecoin Push

For the fourth quarter of fiscal 2025, Circle’s revenue and reserve income increased 76.9% year-over-year (YOY) to $770.23 million. The company had $75.30 billion USDC in circulation by year-end, up 72% from the prior-year period. USDC on-chain transaction volume soared to $11.90 trillion in Q4 2025, reflecting a 247% YOY surge.

Circle highlighted that major enterprises are adopting its infrastructure and using stablecoins. The company’s digital assets reserve is also growing, and its Circle Payments Network (CPN) is being adopted by financial institutions. The company earned an EPS (on a diluted basis) of $0.43. Its adjusted EBITDA grew from $32.73 million in Q4 2024 to $167.48 million in Q4 2025.

Wall Street analysts have a mixed view about Circle’s bottom line trajectory. For the current quarter, its EPS is expected to decrease 100% to $0.15. On the other hand, for the full fiscal 2026, the company’s EPS is projected to grow by 293.2% annually to $0.85, followed by another 101.2% growth to $1.71 for fiscal 2027.

What Do Analysts Think About Circle Stock?

This month, analyst Owen Lau from Clear Street upgraded Circle’s stock from “Hold” to “Buy,” and raised the price target from $92 to $136. The analyst highlighted the company’s flagship stablecoin USDC, which has shown significant growth despite volatility in the broader cryptocurrency market.

Baird, represented by analyst David Koning, has maintained an “Outperform” rating on Circle’s stock and raised the price target from $110 to $138, reflecting a positive outlook for Circle’s performance. On the other hand, in February, Wells Fargo analyst Jason Kupferberg cut the stock’s price target from $128 to $111, despite maintaining an “Overweight” rating.

Citing lower forecasted interest rates and declines in cryptocurrency prices, which have impacted USDC supply growth, analysts at Needham lowered Circle’s price target from $190 to $130 but kept their “Buy” rating.

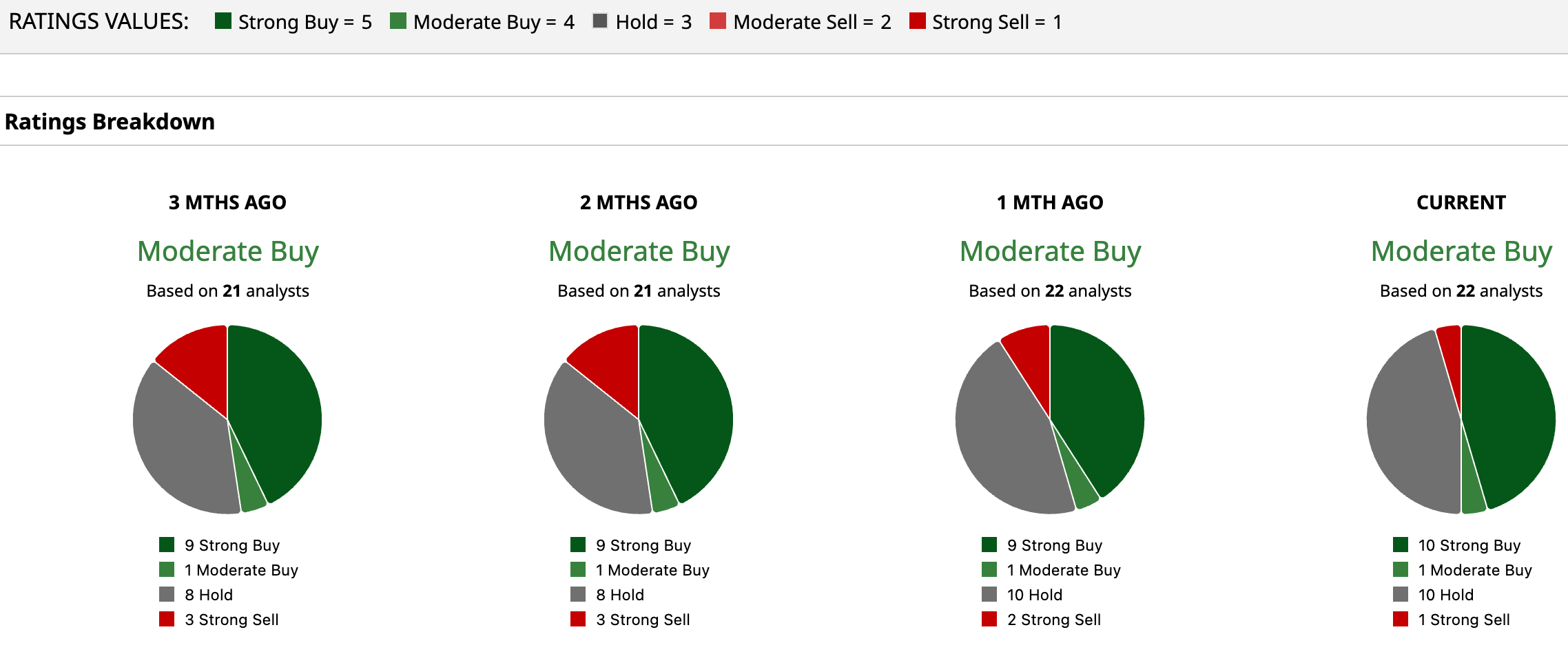

Circle is a sound favorite on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 22 analysts rating the stock, 10 analysts have rated it a “Strong Buy,” one analyst suggests a “Moderate Buy,” while 10 analysts are playing it safe with a “Hold” rating, and one analyst suggests “Strong Sell.” The consensus price target of $126.28 represents a 20.9% upside from current levels. Moreover, the Street-high price target of $280 indicates a 168% upside.

Key Takeaways

The regulatory backdrop has created uncertainty around stablecoins, affecting Circle. However, the company is trying to establish a payment ecosystem. Therefore, until regulatory clarity is reached, it might be wise to observe the stock for now.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Hands%20of%20robot%20and%20human%20touching%20on%20big%20data%20network%20connection%20by%20PopTika%20via%20Shutterstock.jpg)