Digital betting heavyweight DraftKings (DKNG) gained momentum on Monday, March 23, with shares rising 1.2% after reports of a bipartisan U.S. bill targeting prediction markets. The proposal aims to restrict contracts that mimic sports betting, tightening the blurred line between event trading and regulated gambling markets across jurisdictions.

The legislation, led by Nevada Representative Dina Titus, focuses on platforms like Kalshi and Polymarket. These firms list detailed contracts tied to sports outcomes while operating under federal financial rules, avoiding the state-level frameworks that govern traditional sportsbooks and enforce stricter compliance standards.

Critics, including regulators and casino operators, argued these platforms exploit a regulatory gap. They offer nationwide wagering without licenses, consumer safeguards, or tax obligations. Legal challenges in Massachusetts and Nevada reinforced the claim that such products closely resemble sports betting, raising concerns around market integrity and responsible gaming standards.

Investors could view the potential crackdown as a net positive for DraftKings. Tighter rules could limit loosely regulated alternatives and redirect wagering activity toward licensed operators. The shift would strengthen revenue visibility, reinforce its competitive moat, and support long-term confidence as regulatory clarity begins to shape the evolving industry landscape.

About DraftKings Stock

Headquartered in Boston, Massachusetts, DraftKings is a digital-first gaming powerhouse, blending online and retail sports betting with daily fantasy sports, lottery services, and emerging prediction markets.

With a market cap of approximately $11.8 billion, it rounds out its playbook with iGaming staples like blackjack, roulette, baccarat, and slots, while building the tech backbone that powers sportsbooks and online casinos globally.

However, the stock tells a more turbulent story. It has dropped 42.19% over the past 52 weeks. Lately, though, sentiment has started to turn. A 4.72% gain in the last month suggests buyers are testing the waters again.

Valuation adds another layer to the narrative. The stock is currently trading at 1.72 times sales, a premium to industry peers but below its own five-year average multiple. This suggests a wise entry point in the stock.

A Closer Look at DraftKings’ Q4 Earnings

On Feb. 12, DraftKings reported its Q4 fiscal 2025 results, delivering a top line that landed exactly where Wall Street expected. Revenue rose 42.8% year-over-year (YOY) to $1.99 billion, matching analyst estimates. Strong customer engagement, disciplined user acquisition, and improved Sportsbook net revenue margins did the heavy lifting, keeping growth on a steady track.

Yet profitability told a slightly different story. Adjusted EPS came in at $0.36, rising 157.1% from the prior year but falling short of the $0.41 Street forecast. The miss, paired with a cautious management tone, took some wind out of the sails and prompted a sharp market reaction.

Monthly Unique Payers held flat YOY at 4.8 million, suggesting stable engagement without fresh acceleration. But monetization stepped up meaningfully. Average Revenue per MUP climbed nearly 43% to $139, indicating DraftKings is extracting more value from its existing base.

Looking ahead, management is choosing discipline over bravado. The company guided fiscal 2026 revenue to a range of $6.5 billion to $6.9 billion and expects Adjusted EBITDA between $700 million and $900 million. The focus remains on measured investment in Predictions and tighter control over expansion spend.

The earnings trajectory still leans upward. Analysts expect Q1 fiscal 2026 EPS to surge 1,000% YOY to $0.09. For the full year, EPS is projected to rise 171.4% to $0.57, followed by another leap of 110.5% from the prior year to $1.20 in fiscal year 2027.

What Do Analysts Expect for DraftKings Stock?

Wall Street continues to back DKNG stock with measured conviction. Citizens analyst Jordan Bender has maintained a “Market Outperform” rating alongside a $38 price target, signaling confidence in the company’s long-term positioning despite near-term noise.

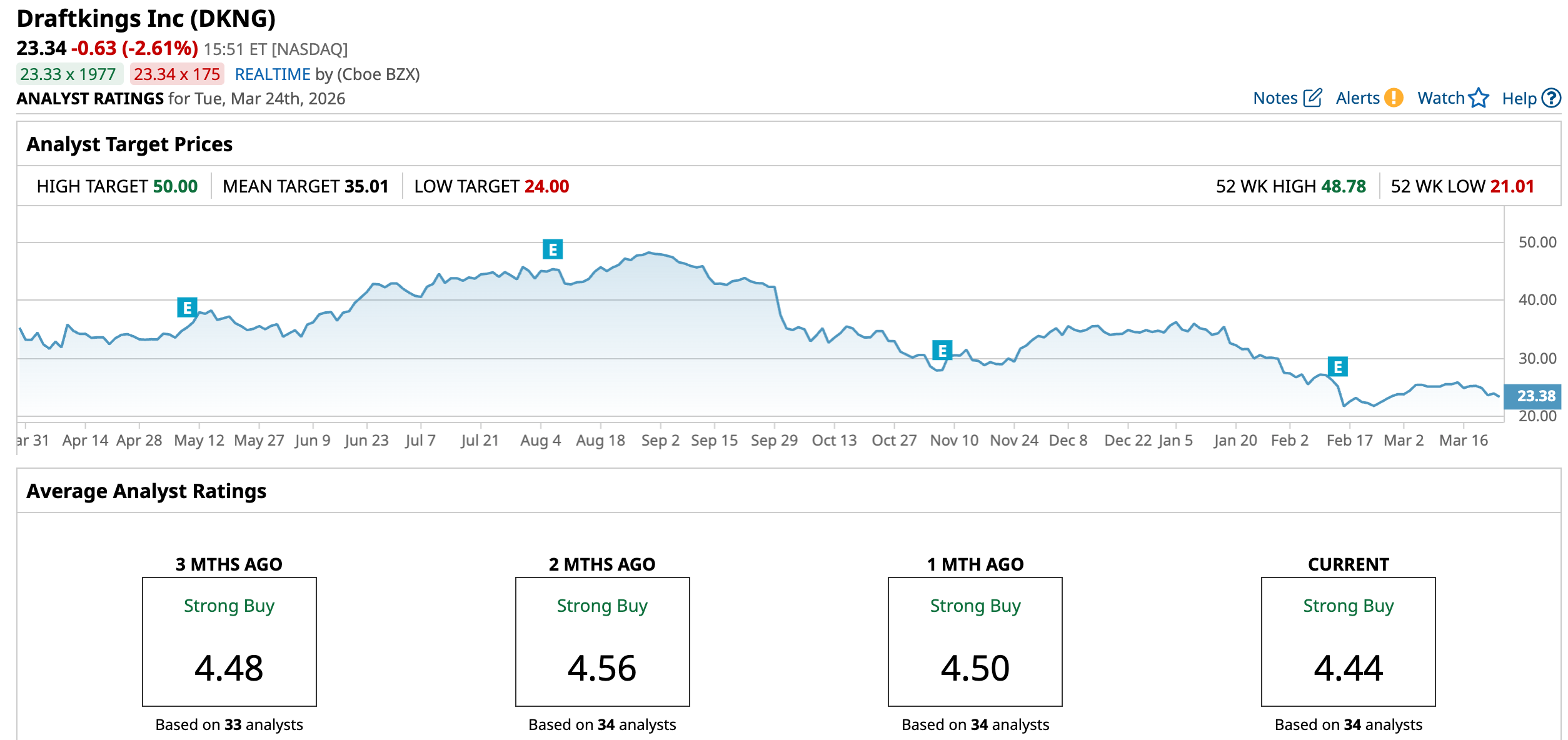

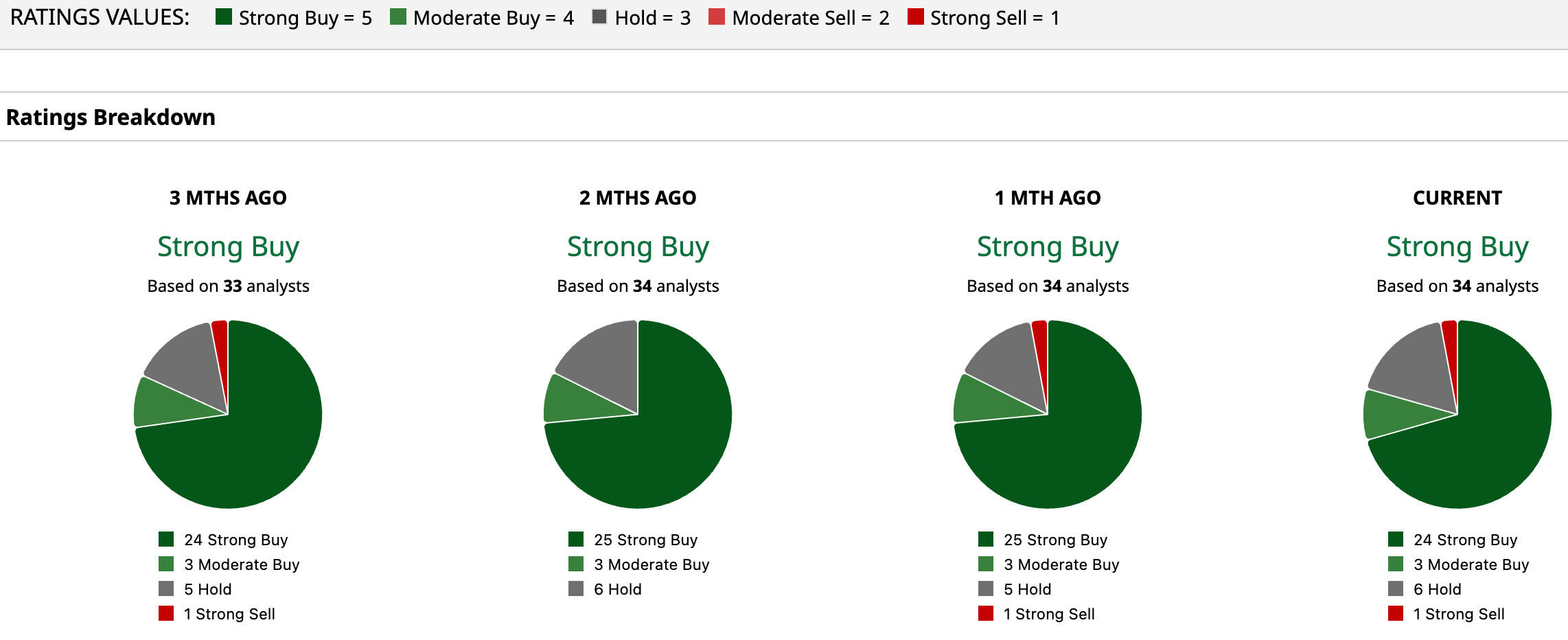

The broader analyst community leans decisively bullish. Among 34 analysts covering the stock, the overall rating sits at “Strong Buy,” with 24 calling it a “Strong Buy,” three assigning a “Moderate Buy,” six opting to “Hold,” and one flagging a “Strong Sell.”

Price targets reinforce the optimism. The mean price target of $35.01 signals 50% upside from current levels. Meanwhile, the Street-high target of $50 set by BMO Capital’s Brian Pitz suggests a gain of 114%.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)