/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOGL) stock has cooled off a bit after a strong rally over the past year. Notably, the launch of Gemini 3 and the significant revenue opportunity from its internal Tensor Processing Units (TPUs) gave its share price a significant boost. However, geopolitical tensions in the Middle East have contributed to market caution, while concerns about the company’s rising capital expenditures have stalled GOOGL’s upward momentum.

Alphabet is investing aggressively as it expands its artificial intelligence (AI) capabilities and underlying infrastructure to meet growing demand. Management has indicated that capital expenditures are projected to rise significantly, reaching between $175 billion and $185 billion in 2026. This marks a substantial increase from the $91.4 billion deployed in 2025, with spending expected to accelerate throughout the year. Such elevated investment levels are likely to place pressure on margins and free cash flow in the near term.

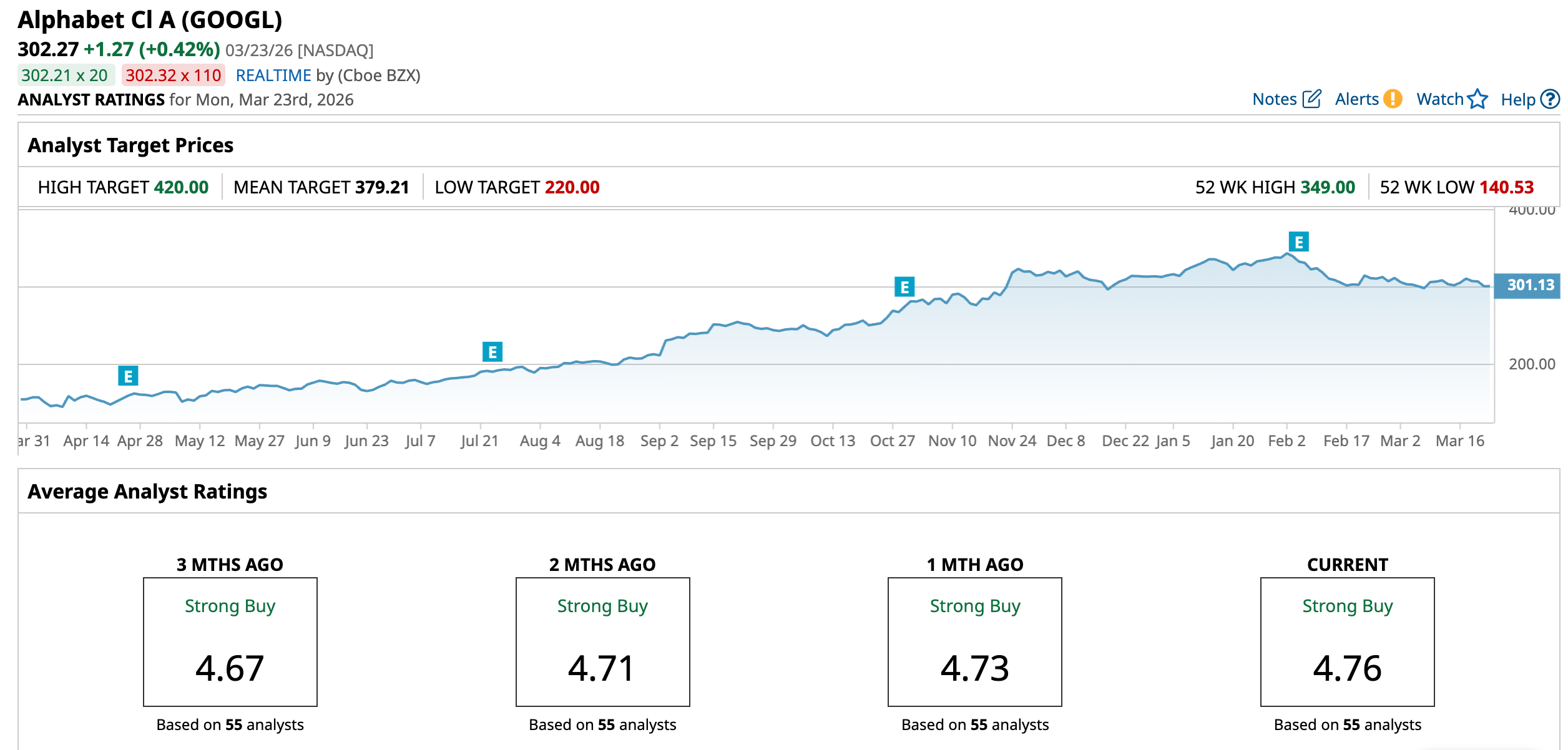

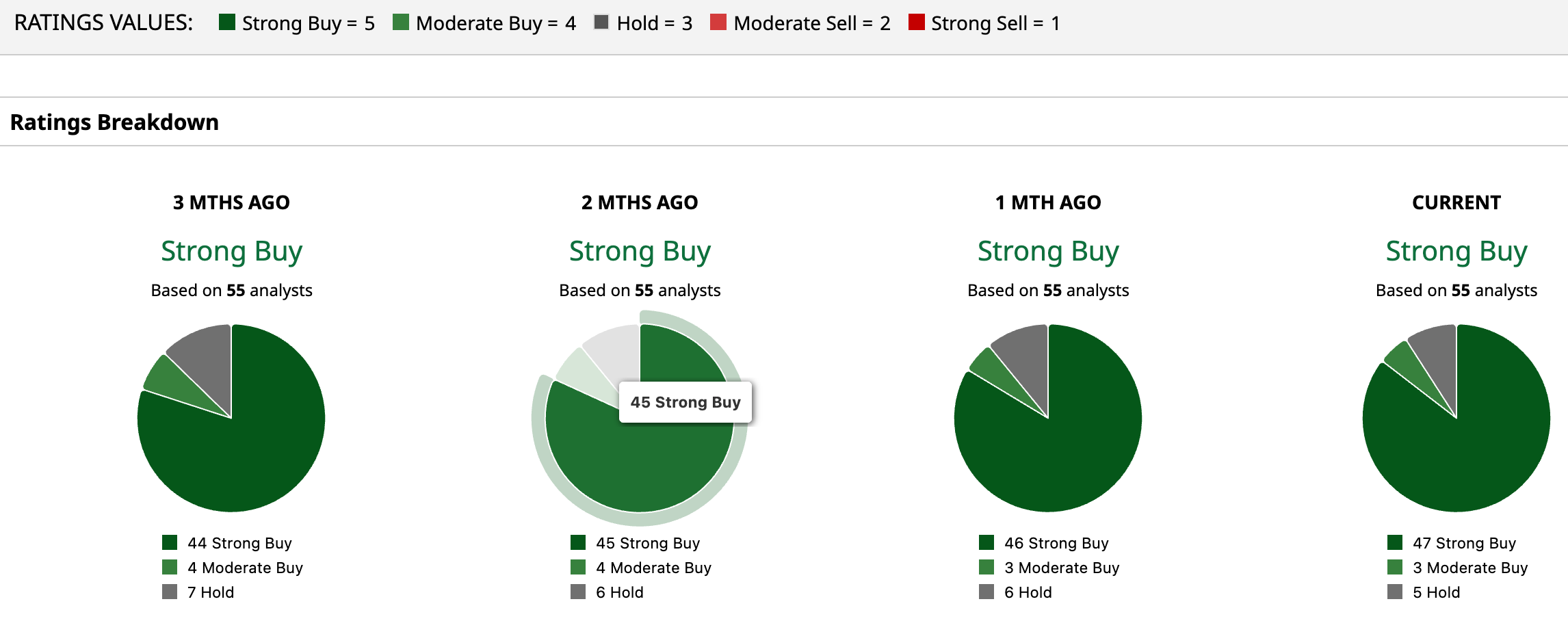

Despite these concerns, most analysts remain optimistic about Alphabet’s long-term outlook. Moreover, at least one analyst is projecting GOOGL stock to hit $420 (the Street's highest price target) over the next 12 months. Based on recent pricing, this implies a potential upside of approximately 40%.

Is GOOGL’s Rising Capital Expenditures Justified?

Alphabet’s rising capital expenditures have weighed on investor sentiment in the near term, but the company’s accelerating investment in AI and infrastructure is translating into solid financial performance.

In 2025, Alphabet generated $403 billion in annual revenue for the first time, reflecting early contributions from its AI initiatives. Momentum remained strong in the fourth quarter, with consolidated revenue reaching $113.8 billion, up 18% year-over-year (YOY). This performance reflects broad-based strength across its businesses.

Its largest segment of Google Services, which includes Search, YouTube, and subscription offerings, saw revenue rise 14% to $95.9 billion. The standout performer remained Search, where revenue climbed 17% to $63.1 billion. This growth shows the durability of Alphabet’s core advertising engine, as AI reshapes the ways in which users interact with information. Enhanced user engagement and improved monetization, driven by AI-powered features, are strengthening Search’s dominance.

Also, YouTube advertising contributed positively, with revenue increasing 9% to $11.4 billion. While more modest compared to Search, this growth reflects steady demand in performance-driven advertising, indicating that advertisers continue to see value across Alphabet’s ecosystem.

Google Cloud continued to deliver strong performance, with quarterly revenue rising 48% to $17.7 billion. Growth was driven by strong enterprise demand for AI-focused solutions, particularly within Google Cloud Platform (GCP). The platform is gaining share through higher customer win rates, larger long-term commitments, and increased spending from existing clients. Enterprise AI products are now generating billions in quarterly revenue, highlighting their growing significance within Alphabet’s overall revenue mix.

AI is proving to be a powerful multiplier within the cloud segment. Approximately 75% of Google Cloud customers now utilize its integrated AI stack, spanning custom silicon, foundational models, and enterprise-grade tools. These customers tend to adopt significantly more products than non-AI users, deepening client relationships and expanding revenue opportunities.

At the same time, enterprises are rapidly scaling AI workloads, driving demand for advanced computing infrastructure such as TPUs and GPUs. Alphabet’s proprietary models, including Gemini 3, are gaining adoption across industries, positioning the company as a vertically integrated AI provider.

Perhaps the clearest validation of this strategy is Google Cloud’s backlog, which reached $240 billion by the end of the fourth quarter. More than doubling YOY and rising 55% sequentially, this backlog represents committed, multi-year revenue, largely tied to enterprise AI contracts.

Alphabet’s elevated capital expenditures are less a risk and more a strategic necessity. The company is effectively building the infrastructure layer of the AI economy while simultaneously monetizing it through its existing platforms.

What’s Next for GOOGL Stock?

Alphabet’s strong fundamentals, led by robust growth in Search, accelerating cloud adoption, and expanding monetization of AI, provide a solid base for sustained revenue expansion. The rapidly growing cloud backlog and deepening enterprise AI integration further strengthen its outlook.

However, investors should note that aggressive capital expenditures, projected to nearly double in 2026, are likely to compress margins and weigh on free cash flow, potentially limiting multiple expansion in the short term. Additionally, macro and geopolitical uncertainties could dampen investor sentiment.

In sum, a near 40% upside is achievable if Alphabet continues to consistently convert its heavy AI investments into sustained revenue growth and focuses on improving margins across its core segments.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)