/NVIDIA%20Corp%20logo%20on%20phone%20and%20AI%20chip-by%20Below%20the%20Sky%20via%20Shutterstock.jpg)

The next phase of the artificial intelligence (AI) boom would be defined by autonomous agentic systems that can plan, execute, and act independently, and that’s where OpenClaw is rapidly emerging as a potential inflection point for NVIDIA Corporation (NVDA). At its 2026 GTC conference, CEO Jensen Huang framed OpenClaw as a foundational shift in computing, arguing that every company will need an agentic AI strategy going forward.

Jensen Huang has highlighted OpenClaw as a breakthrough in AI, calling it the most successful open-source project ever and “the next ChatGPT.” He emphasized that it represents a major shift in human-AI interaction, moving beyond chat-based systems to autonomous agents that can independently perform tasks and execute complex workflows.

Against this backdrop, Nvidia’s partnership with OpenClaw and the launch of its enterprise-grade NemoClaw platform signal a strategic move to extend its dominance beyond chips into the software and orchestration layer of AI. By combining OpenClaw’s ease of building AI agents with Nvidia’s security, privacy, and full-stack infrastructure, the company is positioning itself to make its hardware more deeply embedded in enterprise workflows while opening up new monetization avenues.

The implications for investors are significant. If OpenClaw-style ecosystems become the backbone of next-generation software, Nvidia could evolve from a GPU leader into a full-stack AI platform provider, capturing a larger share of a rapidly expanding market opportunity, one that can propel to $1 trillion in AI infrastructure demand by 2027.

What should be your stance as an OpenClaw-driven ecosystem seems to be gearing up to unlock a new and more durable growth?

About Nvidia Stock

NVIDIA Corporation is a global leader in accelerated computing and AI, renowned for pioneering the GPU that revolutionized gaming, data centers, and AI-driven computing. Headquartered in Santa Clara, California, Nvidia’s technology now powers everything from high-performance gaming and cloud computing to autonomous vehicles and generative AI applications. With a market cap of roughly $4.34 trillion, Nvidia stands among the world’s most valuable companies, driven by its dominance in AI infrastructure and continued innovation in next-generation chip design.

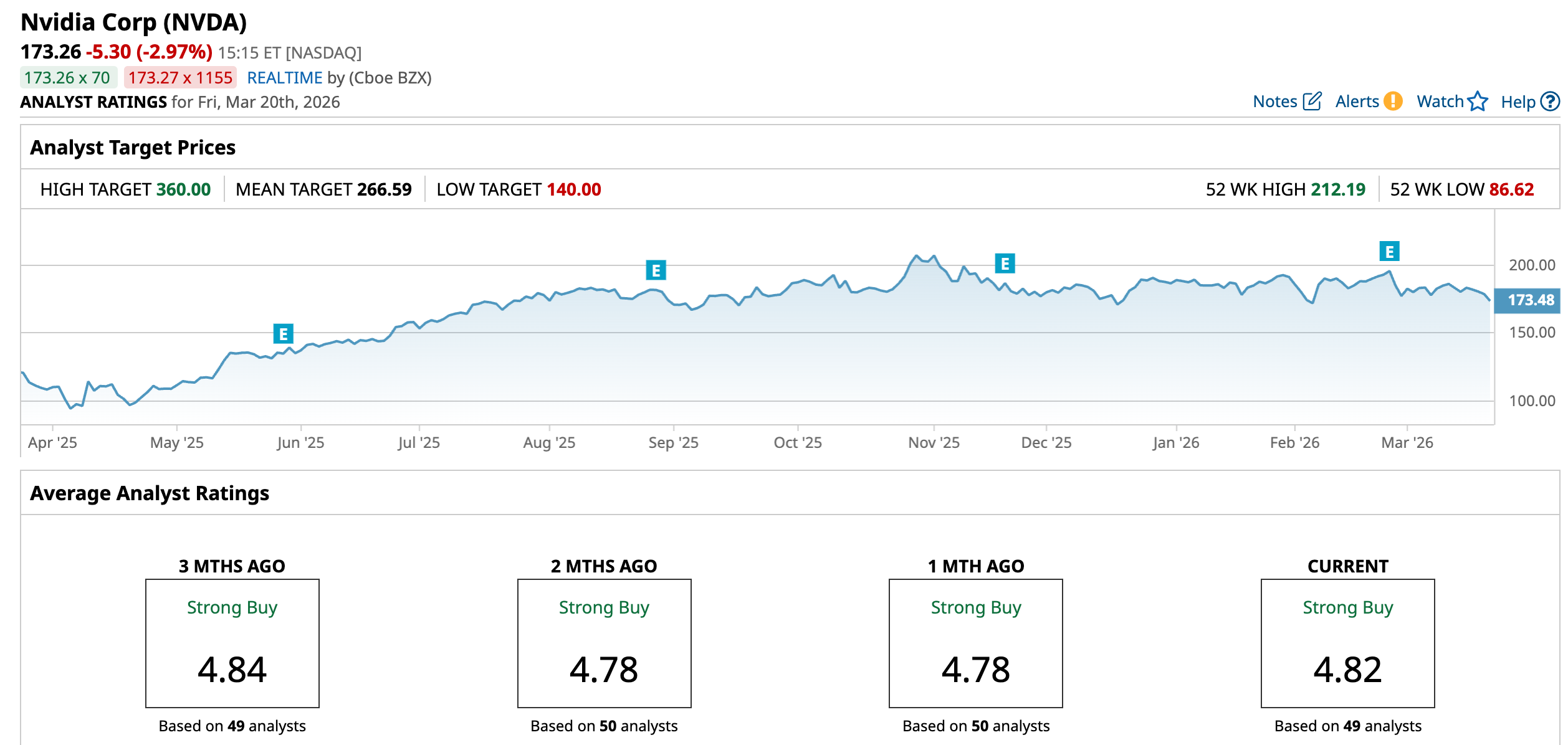

Over the past year, Nvidia’s stock has delivered robust gains, significantly outperforming broader markets as strong demand for generative AI and data center solutions fueled investor enthusiasm. The stock has returned 46.88% over the past 12 months, supported by rapid data center growth, continued leadership in AI hardware, and key product innovations that also pushed shares to a record high near $212.19 in October 2025.

However, performance in 2026 has been subdued, with the stock down 6.65% year-to-date (YTD), reflecting investor rotation out of tech names, rising competition, and cost pressures.

Moreover, price action around the OpenClaw partnership announcement at Nvidia’s GTC event on March 16 was notably muted. The stock traded in a tight range, indicating a largely flat-to-negative reaction despite the strategic significance of the news.

NVDA’s dominant position has led it to trade at a pronounced premium valuation compared to its industry peers, at 20.14 times price-to-sales (TTM).

Better-than-Expected Financials

NVIDIA reported its fourth-quarter and full-year fiscal 2026 results on Feb. 25, delivering another blockbuster performance driven by surging AI infrastructure demand.

For the fourth quarter, revenue came in at a record $68.13 billion, up 73% year-over-year (YOY), highlighting continued strength in AI-related spending. Adjusted earnings also exceeded expectations, with non-GAAP EPS of $1.62 in Q4, up about 82% YOY, and exceeding Wall Street expectations, while profitability remained strong with gross margins above 75%.

The data center segment remained the primary growth engine, generating about $62.3 billion in revenue, up 75% YOY, as hyperscalers and enterprises ramped AI deployments. Other segments also showed strength, with gaming revenue growing around 47% YOY, reflecting improving consumer demand and new product cycles.

On a full-year basis, Nvidia delivered record revenue of $215.9 billion, up 65% YOY, underscoring the scale of the AI boom and Nvidia’s dominant positioning within it. Also, adjusted EPS rose about 60% YOY to $4.77.

Furthermore, Nvidia provided strong forward guidance, forecasting first-quarter fiscal 2027 revenue of around $78 billion plus or minus 2%, implying continued robust demand for its Blackwell and next-generation AI platforms.

Analysts tracking Nvidia project the company’s EPS to climb 66.5% YOY to $7.61 in fiscal 2027 and grow another 29.8% to $9.88 in fiscal 2028.

What Do Analysts Expect for Nvidia Stock?

Following Nvidia’s conference, multiple analysts reaffirmed their bullish stance, issuing positive ratings and raising price targets, reflecting growing confidence in the company’s outlook.

Most recently, Argus reiterated a “Buy” rating and $220 price target on Nvidia following GTC 2026, highlighting Nvidia’s dominant AI positioning, and a projected $1 trillion GPU revenue opportunity by 2027.

Also, Raymond James raised its price target on Nvidia to $323 from $291 and maintained a “Strong Buy” rating, citing growing confidence in the company’s long-term AI opportunity.

Moreover, Truist Securities slightly raised its price target on Nvidia to $287 from $283 while maintaining a “Buy” rating, following the conference’s second day. The firm highlighted strong inference demand, improving product capabilities, and rising “tokenomics” efficiency as key drivers boosting revenue visibility.

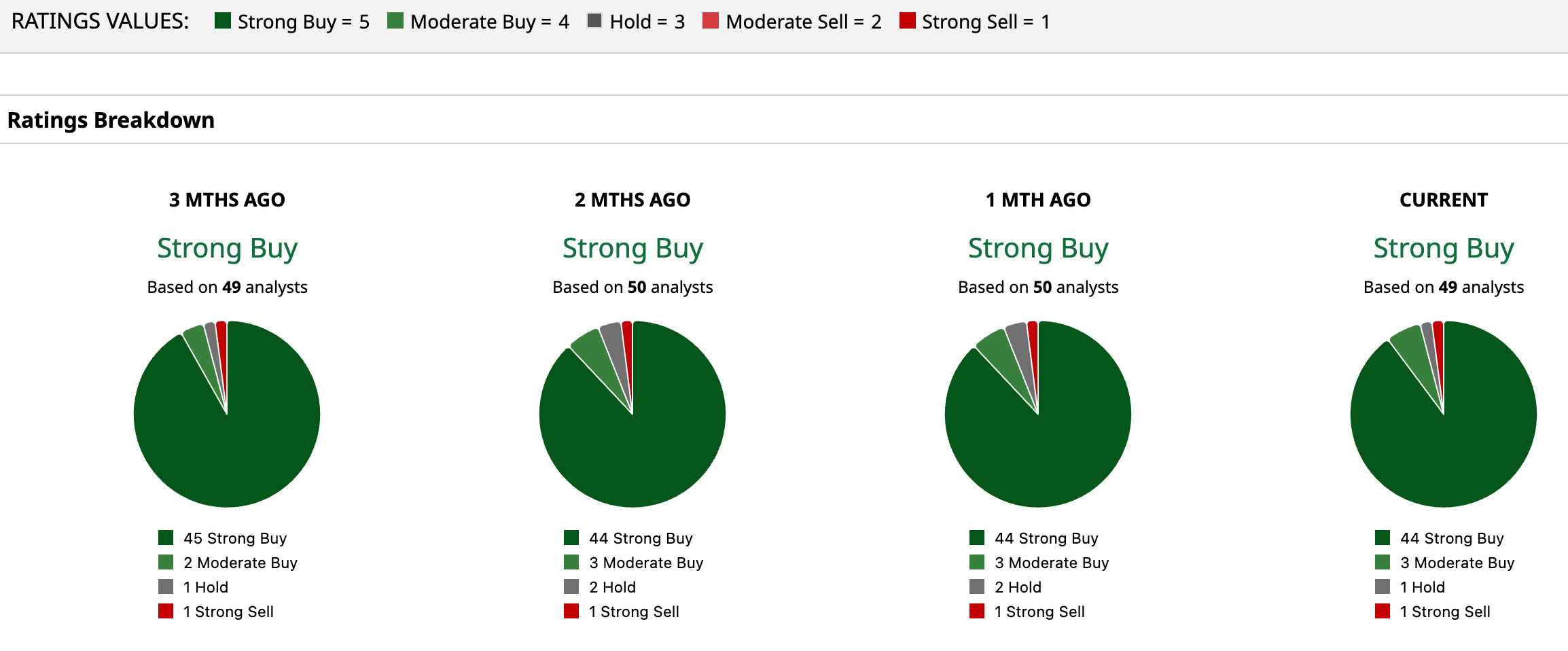

Wall Street’s bullishness is evident in NVDA having a consensus “Strong Buy” rating. Of the 49 analysts covering the stock, 44 advise a “Strong Buy,” three suggest a “Moderate Buy,” one analyst gives a “Hold” rating, and one offers a “Strong Sell” rating.

The average analyst price target for NVDA is $266.59, indicating a potential upside of 53.9%. Also, the Street-high target price of $360 suggests that the stock could rally as much as 107.8%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)