/AI%20(artificial%20intelligence)/AI%20by%20TierneyMJ%20via%20Shutterstock.jpg)

Market volatility tests even the most disciplined investors. When uncertainty rises, especially during a war, many investors focus on protecting their capital by trimming positions or selling stocks that have already pulled back. While this instinct is understandable, market situations can change quickly — and often for the better.

Here are two beaten-down artificial intelligence (AI) stocks that investors may be tempted to sell but shouldn’t just yet.

Beaten-Down AI Stock #1: Snowflake (SNOW)

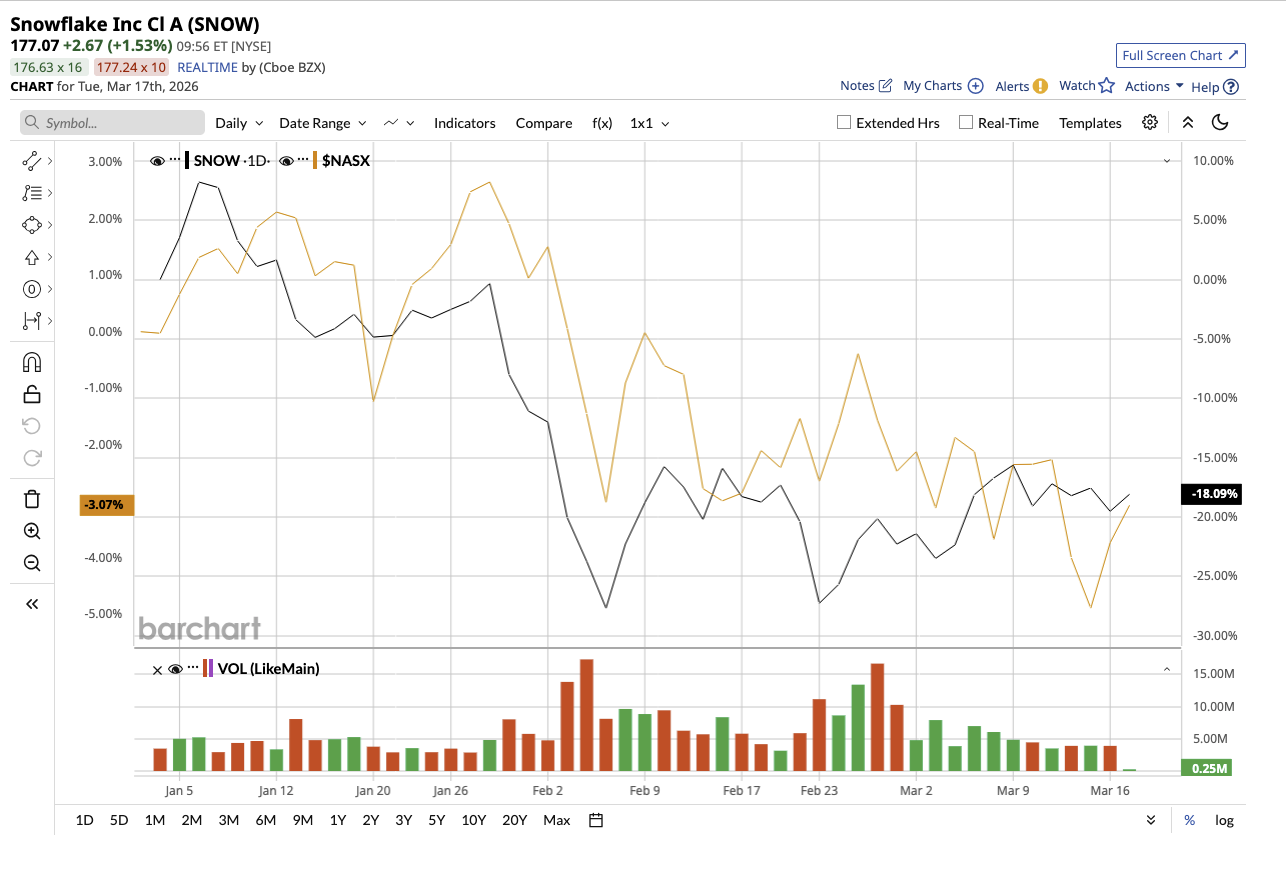

Snowflake (SNOW) received a lot of attention last year amid the AI boom. However, it has been one of the more frustrating names for investors lately. Despite strong long-term positioning, SNOW stock has struggled to maintain momentum. SNOW stock is down 21% so far this year and down 38% from its 52-week high of $280.67.

Investors are wondering whether it’s time to cut losses. But recent quarterly earnings reveal why dumping shares now would be a mistake.

Snowflake is a cloud-based data platform that has evolved from just a traditional data platform to a full-fledged AI-native application layer, where businesses not only store and analyze data but also build and deploy AI-powered workflows. This has led to 30% year-over-year (YOY) growth in revenue to $1.23 billion in the fourth quarter of fiscal 2026. Remaining performance obligations (RPO) surged 42% to $9.77 billion, with net revenue retention rate staying strong at 125%. These numbers do not reflect a struggling business but rather one facing huge demand, especially as AI workloads ramp up. Snowflake’s growing suite of AI tools, particularly Snowflake Intelligence (agent-based AI for enterprises) and Cortex Code (AI-powered development and automation tools), are gaining popularity. Snowflake now has 733 customers spending over $1 million annually, up 27% YOY, and 56 customers now spending more than $10 million, growing 56% YOY.

Despite its rapid expansion, Snowflake's bottom line remains in the red. However, management pointed out that profitability trends are improving, with operating margins rising to 10.5% in the quarter.

The company generated $782 million in free cash flow for the quarter and $1.1 billion for the fiscal year. At the end of the quarter, it had $4.8 billion in cash and investments. Snowflake is also expanding its total addressable market with the acquisition of Observe, which will allow it to join the $50 billion AI-powered observability market. Additionally, Snowflake's relationships with OpenAI, Anthropic, Alpahbet's (GOOGL) Google Cloud, and SAP (SAP) position it as a full-stack AI platform.

Looking ahead, management anticipates a 27% revenue increase in fiscal 2027, driven by continued expansion of AI-powered workloads. Analysts estimate the company will report a $1.79 profit in fiscal 2027, with earnings increasing by 36% the next year. SNOW stock is currently valued at 97 times projected earnings for 2027. The stock's premium valuation reflects investor confidence in its long-term growth prospects. While Snowflake’s pace is slower than that of hypergrowth AI stocks, selling Snowflake now could mean missing out just as its AI strategy starts to pay off.

What is Wall Street Saying About SNOW Stock?

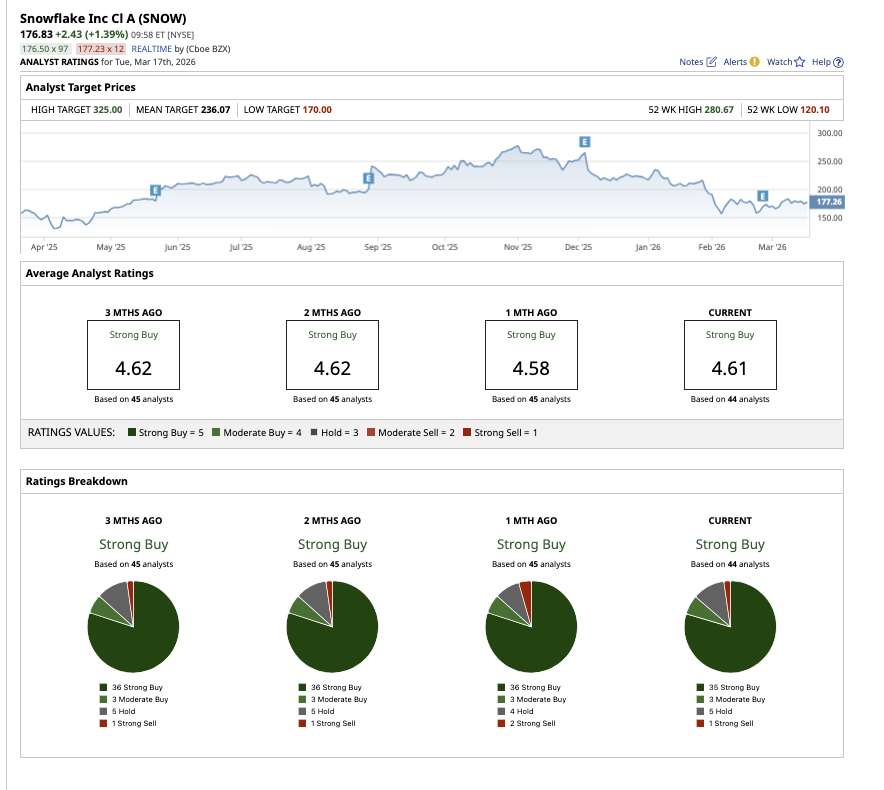

Overall, SNOW stock has garnered a “Strong Buy” consensus rating on Wall Street. Out of the 44 analysts covering SNOW, 35 rate it a “Strong Buy,” three suggest a “Moderate Buy,” five have a “Hold” rating, and one recommends a “Strong Sell.” Based on the average target price of $235.12, the stock has potential upside of 36% from current levels. Plus, the high target price of $325 suggests as much as 88% upside over the next 12 months.

Beaten-Down AI Stock #2: ServiceNow (NOW)

The second beaten-down growth stock that hasn’t been immune to recent market volatility is ServiceNow (NOW). Like many AI-linked software stocks, its valuation has also been questioned recently. NOW stock is down 26% so far this year and 47% from its 52-week high of $211.48. However, the company is executing really well and might just be the most misunderstood AI winner right now.

ServiceNow reported another standout quarter despite market concerns. In Q4, subscription revenue grew 21% YOY to $3.47 billion driven by growth in key areas like CRM, security, and AI-driven products. Remaining performance obligations (RPO) rose 22% YOY to $28.2 billion. The company reported a 98% renewal rate, showing strong customer stickiness, and signed 244 deals over $1 million, including multiple mega deals in the quarter.

ServiceNow's AI push, Now Assist, is getting major traction, with over $600 million in annual contract value. Furthermore, recent acquisitions such as VESA and ARMS have strengthened the company's position in AI security, taking its addressable market beyond $600 billion. Unlike many high-growth tech businesses, ServiceNow is already profitable, with adjusted net income of $959 million in Q4 and $3.6 billion in 2025. The company generated $4.6 billion in free cash flow and had over $10 billion in cash and investments at the end of Q4.

There is rising speculation that AI will disrupt traditional software enterprises. Management answered these concerns, claiming that ServiceNow is no longer solely a SaaS company. It is in fact evolving into a full enterprise AI platform. Looking ahead to 2026, the company anticipates 20% organic subscription revenue growth and continued AI-driven expansion. Analysts expect earnings to rise by 19% and 20% over the next two years.

Trading at 27 times forward earnings, NOW seems like a reasonable buy currently. ServiceNow stock may have fallen this year, but this could be due to broader market sentiment rather than a flaw in the company's fundamentals or growth strategy. For long-term investors, this drop may be an appealing entry point.

What is Wall Street Saying About NOW Stock?

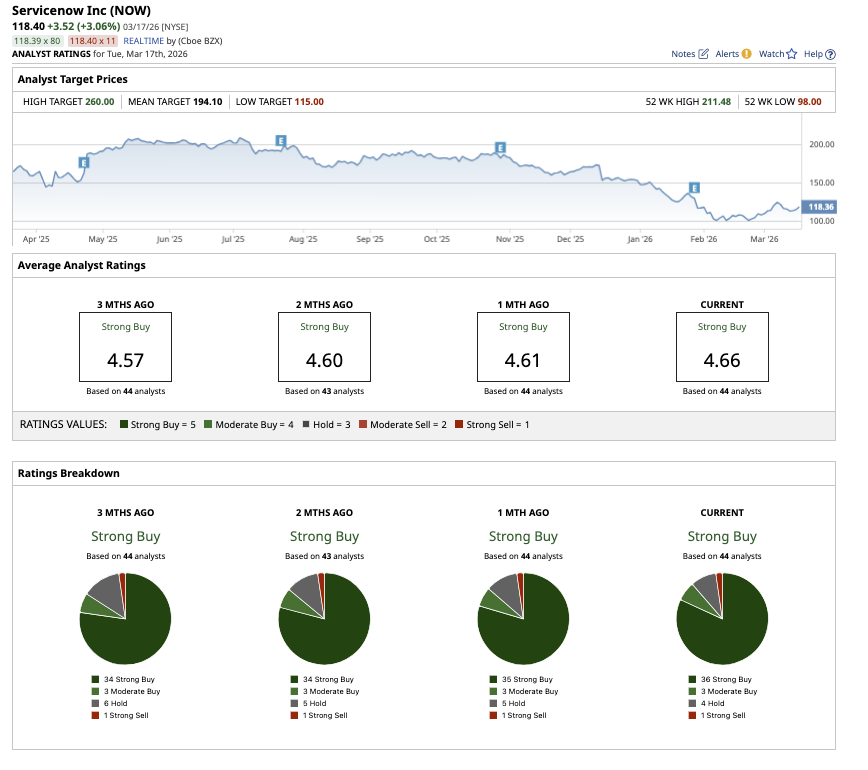

Overall, NOW stock has a “Strong Buy” consensus rating on Wall Street. Out of the 44 analysts covering NOW stock, 36 have a “Strong Buy,” three suggest a “Moderate Buy,” four rate it a “Hold,” and one recommends a “Strong Sell.” Based on the average target price of $193.07, the stock has potential upside of 72% from current levels. Plus, its high target price of $260 suggests that the stock could gain as much as 131% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)