Iran’s escalating use of naval mines and drones in the Strait of Hormuz has turned one of the world’s most vital energy chokepoints into a slow‑motion crisis for global trade. Oil tankers and commercial vessels now navigate a corridor where a single misstep can trigger both physical damage and a fresh spike in risk premiums across energy and shipping markets.

The immediate question is no longer simply who sells missiles and interceptors, but which companies can supply the unglamorous, highly specialized technology needed to actually clear the waterway and keep it open. That shift is propelling a once‑niche corner of defense (that is, autonomous mine‑countermeasure systems) into the center of Washington’s and its allies’ operational planning. Textron (TXT) now stands out as a relatively under‑the‑radar name.

If the Strait of Hormuz becomes the first real‑world test of large‑scale, autonomous mine‑countermeasure operations, could Textron be one of the most asymmetric ways to invest in that shift? Let’s find out.

Textron’s Solid Numbers

Headquartered in Providence, Rhode Island, Textron builds aircraft, defense systems, and unmanned platforms that now include mine‑sweeping and mine‑hunting technology tied directly to the Strait of Hormuz narrative.

Its shares trade at 0.36%% year-to-date (YTD) and 17.52% over the past 52 weeks.

This valuation profile sits at about 14.97x trailing earnings against a sector median near 20.79x and at 1.97x book versus a sector median of 3.07x, suggesting the market has not fully priced in the upside from Textron.

Their most recent reported quarter, ending in December 2025, showed EPS of $1.73 versus a consensus estimate of $1.74, a small 0.57% downside surprise that did little to change the underlying trajectory. This print was paired with revenue of $4.18 billion, which translated into 15.6% year‑over‑year (YOY) growth and signaled that key defense and aviation programs are scaling.

It also came with adjusted EBITDA of $506 million versus estimates of $497.5 million, good for a 12.1% margin and a 1.7% beat. The cash‑flow picture adds another layer to the story, supporting Textron as a mine‑sweeping proxy rather than just a cyclical industrial.

Their operating cash flow for December 2025 reached roughly $1.31 billion, up 114.38%, which points to stronger cash conversion from earnings and healthier funding for R&D and capital returns. This improvement was mirrored in the net cash flow of about $584 million, a surge of 620.99% that gives the company more flexibility to backstop long‑cycle defense programs linked to the Strait of Hormuz.

Textron’s Aviation Momentum

Textron’s aviation arm has been busy, and that matters for anyone looking at the stock as a way to play mine‑sweeping tech in the Strait of Hormuz. The Cessna Citation CJ3 Gen2 has now entered service, bringing what the company describes as the most significant Gen2 updates so far to its popular midsize platform. These upgrades help reinforce the franchise with operators that value efficient, modern cabins and avionics, and they support the cash flows that ultimately fund Textron’s unmanned and mine‑countermeasure work.

Another step forward came as the Cessna Citation M2 Gen2, already the most delivered light‑entry jet in its class, entered service with Garmin autothrottles. This feature gives pilots greater control and precision, and it keeps the M2 Gen2 competitive with newer rivals without requiring a clean‑sheet design cycle.

A quieter but important piece is training. A full‑flight simulator for the Cessna Citation Ascend, developed by Textron’s TRU Simulation unit, has secured Federal Aviation Administration (FAA) qualification. That certification expands advanced training capacity for midsize‑jet pilots and deepens relationships with operators that rely on high‑fidelity simulators.

What Wall Street Sees in Textron’s Mine‑Sweeping Upside

Textron’s earnings setup is more “steady grind higher” than explosive, with the next earnings release scheduled for April 23, and the Street looking for Q1 2026 EPS of $1.29 versus $1.28 in the prior-year quarter, implying a modest YOY growth rate of about 0.78%.

That slow‑and‑steady message also shows up in the company’s guidance. Their adjusted EPS guidance for the 2026 financial year sits at $6.50 at the midpoint, which comes in 4.9% below where analysts had been modeling.

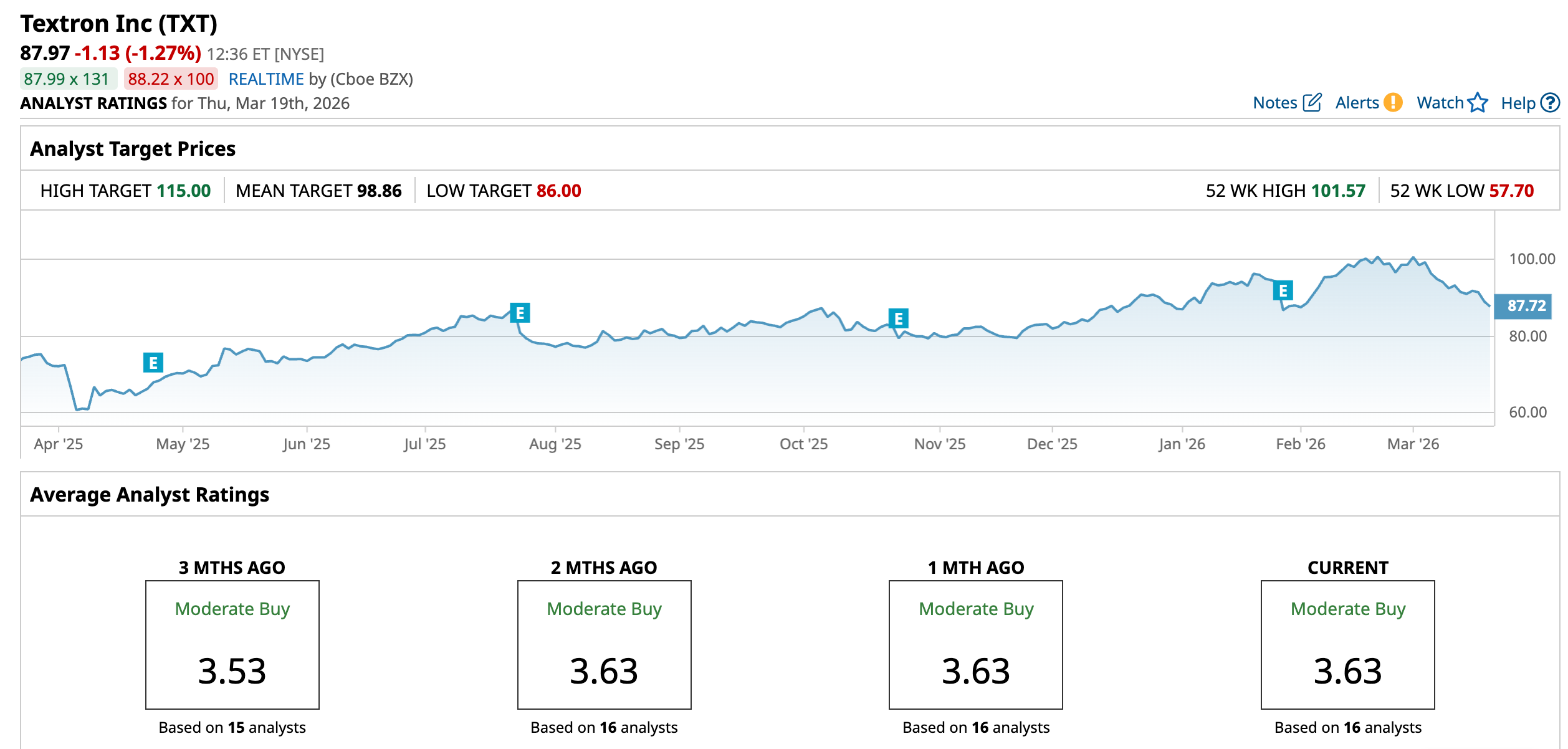

The way the Street is framing the stock backs that up. One of the more vocal voices, Jefferies analyst Sheila Kahyaoglu, recently reiterated a “Buy” rating while trimming her price target to $110 from $115, reflecting a slightly more tempered valuation outlook without changing the positive stance on execution or the long‑term story.

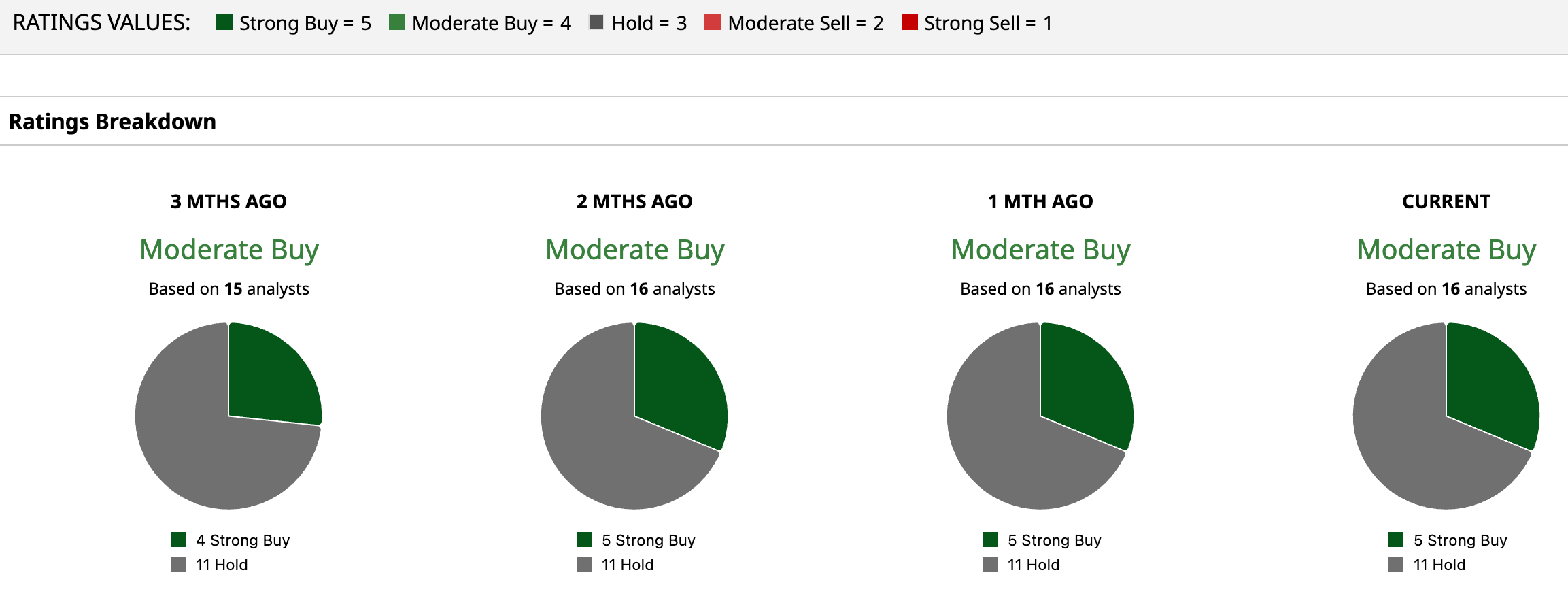

The broader analyst consensus lands at “Moderate Buy,” based on input from 16 firms. Their average price target stands at $98.86, which implies roughly 12.4% upside from the recent share price.

Conclusion

Textron looks like a quietly compelling way to express a view on mine‑sweeping demand in the Strait of Hormuz, backed by real cash flow and credible programs rather than just headlines. Its earnings expectations for 2026 are conservative, and guidance sits a bit below prior forecasts, yet the Street still leans “Moderate Buy.” The setup points more toward a gradual grind higher than a moonshot, helped by growing interest in unmanned surface vessels and mine‑countermeasure tech. In that context, Textron looks less like a speculative bet and more like a reasonably priced ticket.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)