/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Micron (MU) reported strong second-quarter financial results, outperforming expectations with record revenue across its core businesses, including DRAM, NAND, and high-bandwidth memory (HBM). Management said that each business unit achieved new highs, supported by robust artificial intelligence (AI)-driven demand for its advanced memory products and improved pricing conditions.

Micron also delivered notable expansion in gross margins, earnings, and free cash flow, reflecting operational efficiency and favorable market dynamics. Its balance sheet remains solid, with total debt reduced by more than $5 billion over the past three quarters, resulting in a healthy net cash position.

Thanks to its solid financial performance and significant cash generation, Micron announced a 30% increase in its quarterly dividend, raising it to $0.15 per share. This move reflects management’s confidence in the company’s long-term profitability and capital return strategy.

Why Micron Stock Fell: Capex Concerns Take Center Stage

Despite these positive developments, Micron’s stock declined following the earnings release, weighed down by concerns about rising capital expenditures. The company projected fiscal 2026 spending to exceed $25 billion, substantially above its previous estimate of $20 billion. The anticipated increase in investment has raised questions about potential pressure on margins and the pace of future earnings growth.

However, the broader outlook for MU stock remains constructive. Strong demand trends, supportive pricing, and expectations of record margins and earnings continue to strengthen its growth trajectory and investment case. Moreover, its attractive valuation suggests Micron stock has room for further upside, making pullbacks a potential buying opportunity for long-term investors.

Micron’s Growth Outlook Remains Strong

Rising demand for memory, driven by the rapid expansion of AI workloads and supply constraints, has positioned Micron for strong growth. As AI systems evolve, computing architectures are becoming increasingly memory-intensive, driving the demand for advanced memory and storage solutions. This shift plays into Micron’s favor and positions it well as one of the top beneficiaries in the AI ecosystem.

Management struck an optimistic tone during the Q2 conference call. The company forecasts third-quarter revenue of approximately $33.5 billion, which implies year-over-year (YoY) growth of more than 260%. Moreover, it reflects a strong sequential growth from the $23.86 billion reported in the second quarter.

This strong top-line performance is expected to translate into substantial margin expansion. Gross margins are projected to reach approximately 81%, a significant improvement from the adjusted gross margin of 39% recorded in the third quarter of fiscal 2025. Earnings are also set to rise sharply, with projected earnings per share of $19.15 at the midpoint, compared with $1.91 in the same quarter of the prior year.

Micron’s data center end market could continue to drive its financials. Demand for server units remains robust, and Micron has strategically positioned itself to capture incremental demand and sustain growth through a portfolio of high-value offerings, including high-bandwidth memory (HBM), high-capacity server memory modules, and data center solid-state drives (SSDs).

Industry supply dynamics will further support Micron’s growth. Memory supply remains constrained, driving higher prices. This favorable pricing condition will support revenue growth and margin expansion.

Looking ahead, Micron’s growth outlook is supported by several factors, including sustained demand, an expanding addressable market, favorable pricing conditions, and a strategic focus on high-value and next-generation products. Together, these elements position the company to deliver significant long-term growth.

MU Stock’s Valuation Still Attractive, Supporting a Buy

Micron stock trades at 12.5 times forward earnings, a multiple that appears modest given the company’s projected earnings trajectory.

Consensus estimates suggest earnings could grow by over 364% in 2026, despite higher capital expenditures, followed by a 54.7% jump in fiscal 2027. Such strong growth projection and relatively low valuation multiple indicate further upside in MU stock.

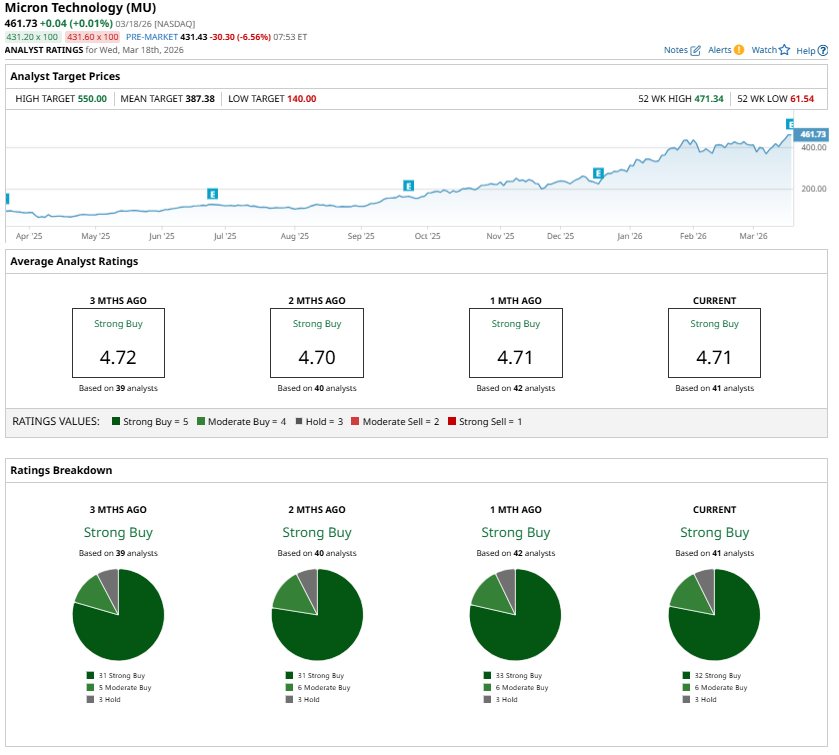

Most analysts are bullish, with MU stock sporting a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.