The war in Iran couldn't have come at a worse time for American farmers, and it's sending fertilizer stocks soaring.

According to a StreetInsider report, a sizeable chunk (over 30%) of global fertilizer supply passes through the Strait of Hormuz. Since Iran was attacked, it has restricted supply in the Strait, delaying delivery timelines.

With fertilizer prices rising, two relatively unknown fertilizer stocks are poised to outperform in the near term.

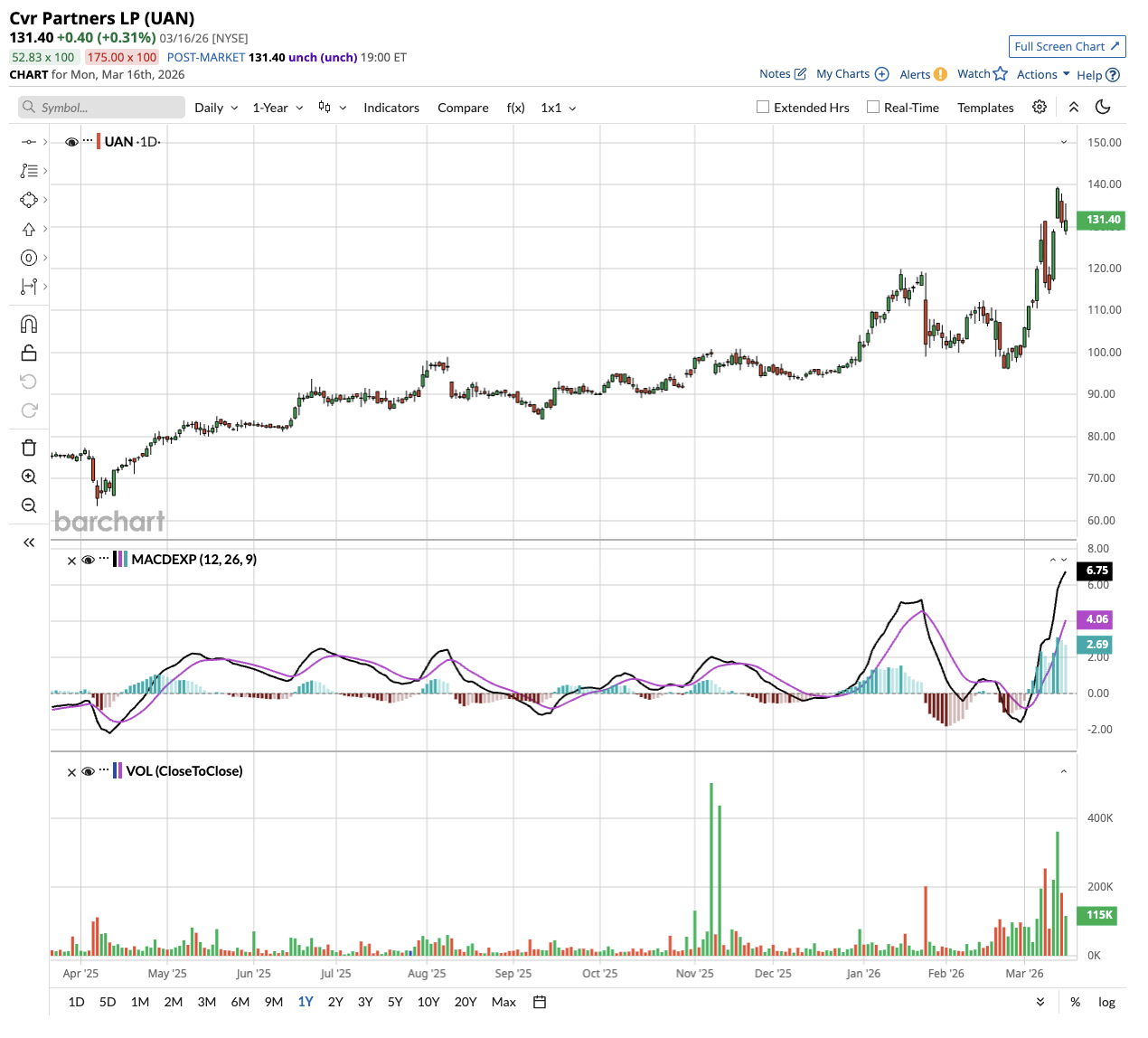

CVR Partners' Stock Was Already Rising Before the War

CVR Partners (UAN) reported full-year 2025 EBITDA of $211 million and paid out $10.54 per common unit in distributions for the year.

The setup heading into spring 2026 was already constructive before the Iran conflict escalated. CEO Mark Pytosh emphasized that the company's order book heading into Q1 was larger than typical, after December pre-buying came in lighter and then surged in January and February.

He added that ammonia was already moving across a broad stretch of the Midwest, from the Southern Plains all the way to Iowa and Illinois, in mid-February, weeks ahead of the usual pace.

"If you can get a jump on your ammonia application, that really helps you get prepared for the spring," Pytosh said.

With ammonia prices up roughly 32% year-over-year (YoY) in Q4 and the supply picture now tighter than ever, CVR Partners is operating in one of the best nitrogen fertilizer pricing environments in years.

Pytosh also pointed to structural support from Europe, where natural gas prices have been running above $13 per MMBtu, keeping European production well below historical levels and creating ongoing export opportunities for U.S. Gulf Coast producers.

In 2025, CVR reported revenue of $606 million, an increase of 15.4% YoY. It reported an operating margin of $130 million and a free cash flow of almost $100 million. UAN stock is up 30% in 2026 and has surged 75% in the past year.

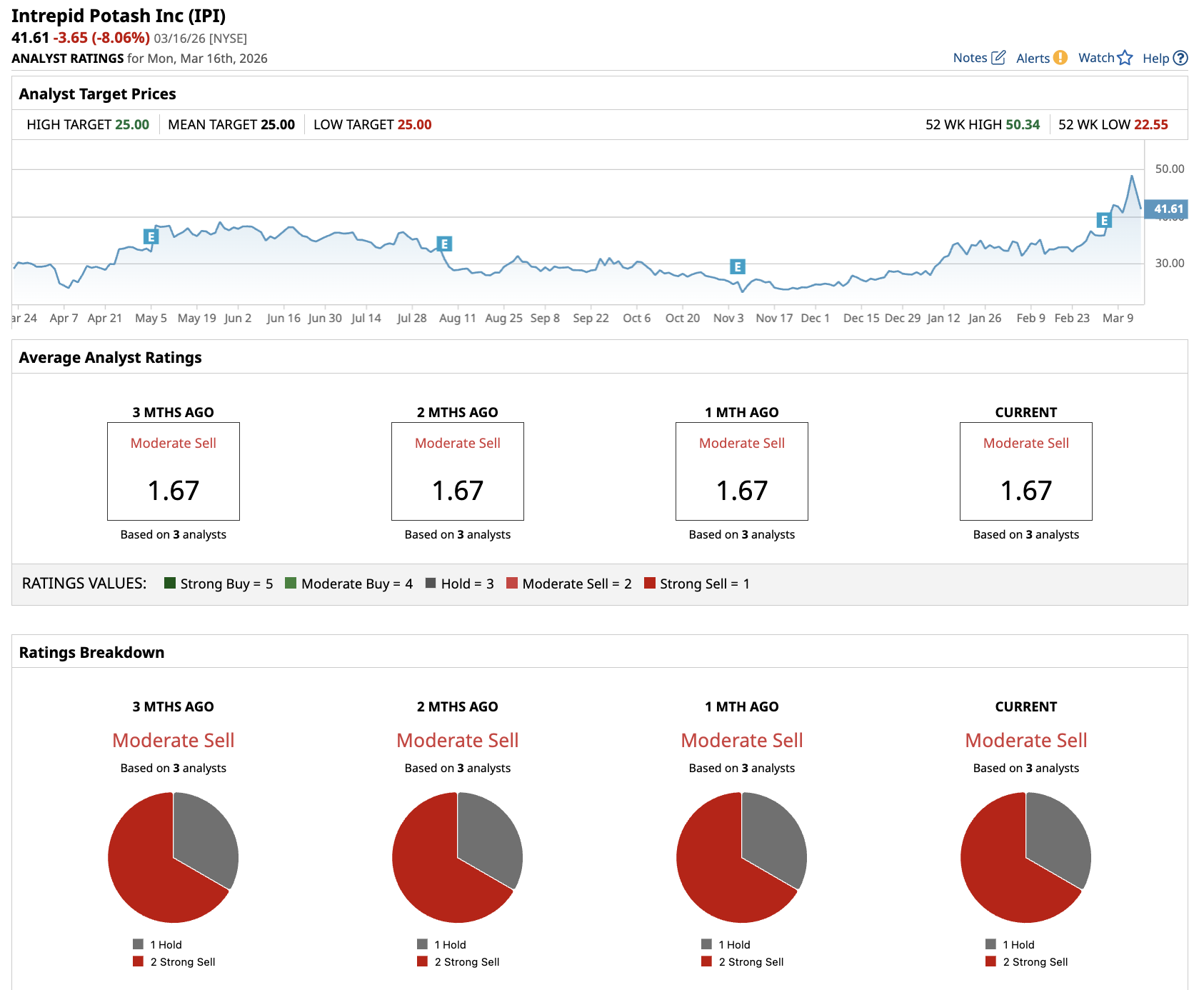

Intrepid Potash is a Sleeper Fertilizer Stock Pick

Intrepid Potash (IPI) delivered full-year 2025 adjusted EBITDA of $63 million, one of its best results since 2016 and an improvement of nearly 80% versus 2024, according to its Q4 earnings call.

CEO Kevin Crutchfield noted that potash remains attractively priced for growers, with U.S. prices trading at a discount to virtually every major global benchmark. That gap creates room for domestic price increases as global supply tightens.

Trio, Intrepid's sulfate-based fertilizer product, could be a key driver.

- Middle East tensions have already driven a sharp increase in sulfur prices, and management said on the earnings call that they were watching closely to see whether that flows through to higher sulfate valuations, a direct tailwind for Trio pricing.

- Record Trio sales of 303,000 tons in 2025 and a guided production increase of roughly 7% in 2026 give the company meaningful volume leverage on top of any pricing tailwind.

Intrepid also holds a wildcard: a lithium project in Wendover, Nevada, where maiden resource estimates of approximately 119,000 tons of lithium carbonate equivalent were published alongside its 2025 annual report. At 5,000 tons per year of estimated production capacity, that represents a roughly 25-year project life, an optionality play that most investors aren't pricing in yet.

With fertilizer markets in crisis mode and both companies posting strong fundamental momentum before the conflict even escalated, UAN and IPI stand out as two names worth watching closely this spring.

Valued at a market cap of $545 million, IPI stock is up 45% in the last 12 months. Out of the three analysts covering IPI stock, one recommends “Hold,” and two recommend “Strong Sell.”

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Quantum%20Computing/A%20concept%20image%20of%20a%20green%20and%20yellow%20motherboard_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)