/Marsh%20%26%20McLennan%20Cos_%2C%20Inc_%20magnified%20logo%20by-%20Casimiro%20PT%20via%20Shutterstock.jpg)

With a market cap of $84.1 billion, Marsh & McLennan Companies, Inc. (MRSH) is a leading global professional services company providing insurance brokerage, reinsurance, risk management, and consulting services through its major brands Marsh, Guy Carpenter, Mercer, and Oliver Wyman. Headquartered in New York, it serves clients in over 130 countries and is known for its diversified, fee-based business model and strong presence in risk and advisory services.

Companies worth $10 billion or more are generally described as “large-cap” stocks, and Marsh & McLennan fits right into that category with its market cap exceeding this threshold. Operating in more than 130 countries, MRSH leverages broad geographic diversification alongside a solid financial foundation. The company continues to prioritize innovation, integrating data analytics and AI to refine its offerings, while its strong client-first approach supports high retention rates and enduring relationships.

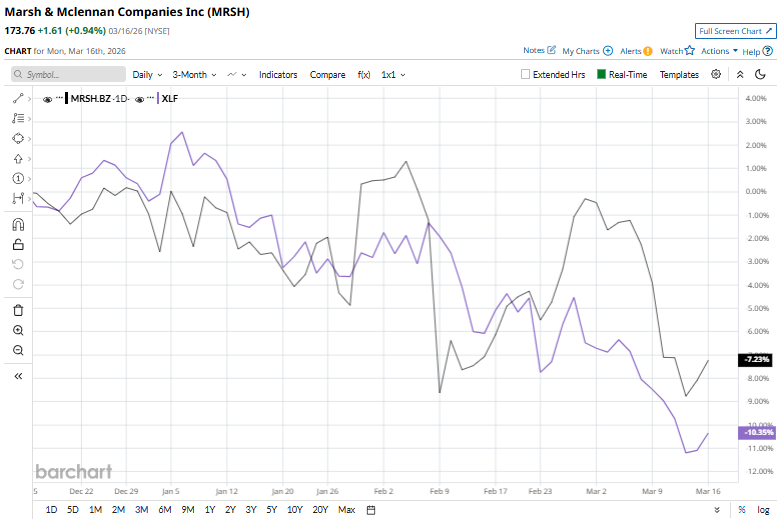

But it’s not all sunshine and rainbows for the stock. MRSH is currently trading 29.9% below its 52-week high of $248. Shares of MRSH have declined 7.2% over the past three months, outpacing the State Street Financial Select Sector SPDR Fund’s (XLF) 9.8% fall.

However, MRSH has tanked 11.7% over the past six months, underperforming XLF’s 8% returns. However, shares of MRSH have plunged 25% over the past 52 weeks, trailing XLF’s 1.6% gains over the same time frame.

MRSH has been trading below its 200-day moving average since early June and has dipped below the 50-day moving average recently, indicating a downtrend.

On Feb. 11, the company priced $600 million of 4.95% senior notes due 2036. The proceeds will be used for general corporate purposes, with the offering expected to close on Feb. 19, 2026, subject to customary conditions.

In the competitive arena of insurance brokers, Aon plc (AON), MRSH’s top rival, is in the lead, declining 18.1% over the past 52 weeks and 8.4% over the past six months.

Wall Street remains cautious about its prospects. The stock has a consensus rating of “Moderate Buy” from the 25 analysts covering it, and the mean price target of $208.28 represents a premium of 19.9% from the current market prices.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)