Howdy market watchers!

It has been a busy week in the markets, to say the least. It has also been a historic week. If being at war with Iran wasn’t enough, Sunday night’s spike in crude oil markets was the largest in the history of crude oil trading! April WTI futures traded to a high at $119.48 per barrel before collapsing under its own weight to trade to a low of $81.19 in the same session, a daily range of $38.29 per barrel, before closing at $85.08. And that all happened during Monday’s session that started on Sunday at 5 PM CDT.

As the commentary and news headlines began to oscillate, so too did the markets. The trade flow was all led by crude oil that then had the opposite effect on the equity market. Grains rallied with crude oil while cattle weakened with stock market softness. Metals wanted a stronger stock market and weaker crude oil. You could basically watch the crude oil trend and the rest would follow.

With the Strait of Hormuz representing 20 percent of global oil flows, restriction of this critical channel causes major disruptions for many economies. Dozens of countries this week through the International Energy Agency decided to release 400 million barrels from their reserves in hopes of easing oil prices that spill over into consumer fuel prices. The US also announced releasing 172 million barrels of oil from the Strategic Petroleum Reserves next week.

Oil futures weakened slightly on this news, but then began to climb higher. Note these reserves are not immediately available to the market. It takes time to distribute, but the pace is also determined by the capacity of the infrastructure, which can cause damage if done too quickly.

A new Iranian Supreme Leader emerged this week on paper only making statements that crude could surge to $200 per barrel and that they would continue fighting and attacking regional targets including ships in the Hormuz. Surprisingly, oil markets remained below $100 for the entire week other than that brief initial spike on Sunday evening. However, as the trading week began to draw to a close, oil futures began creeping higher. April WTI futures closed $0.01 cent off the day’s high at $99.31 per barrel. All eyes will be on actions over the weekend.

The US military has continued to aggressively destroy targets and the ability for the enemy to fight back. Having said that, the disparate nature of the combatants launching from remote areas with underground storage bunkers makes it more difficult to achieve comprehensive defeat. With attacks on neighboring countries, Iran has become increasingly if not totally isolated other than help from Russia and China.

The impact on global fertilizer is as much of a story as energy if not more for the agricultural sector. The stock prices of listed fertilizer companies surged this week following the spike in nitrogen prices, in particular. This comes at a time when wheat farmers are topdressing and row crop producers are preparing for planting. There is talk that such increase in fertilizer prices could change the acre mix with fewer corn acres being planted due to higher input costs. There may be some of this in play, but many of the corn acres are fertilized over the winter.

If this conflict is sustained and fertilizer prices remain elevated, it will have an impact on farmer margins as well as the amount of fertilizer applied, especially if crop prices do not increase accordingly. Grain prices spiked in Monday’s session starting Sunday evening along with crude, but suffered a similar fate finish the day’s session. While futures chopped around in wide ranges, futures contracts managed to continue making new daily highs as the week progressed.

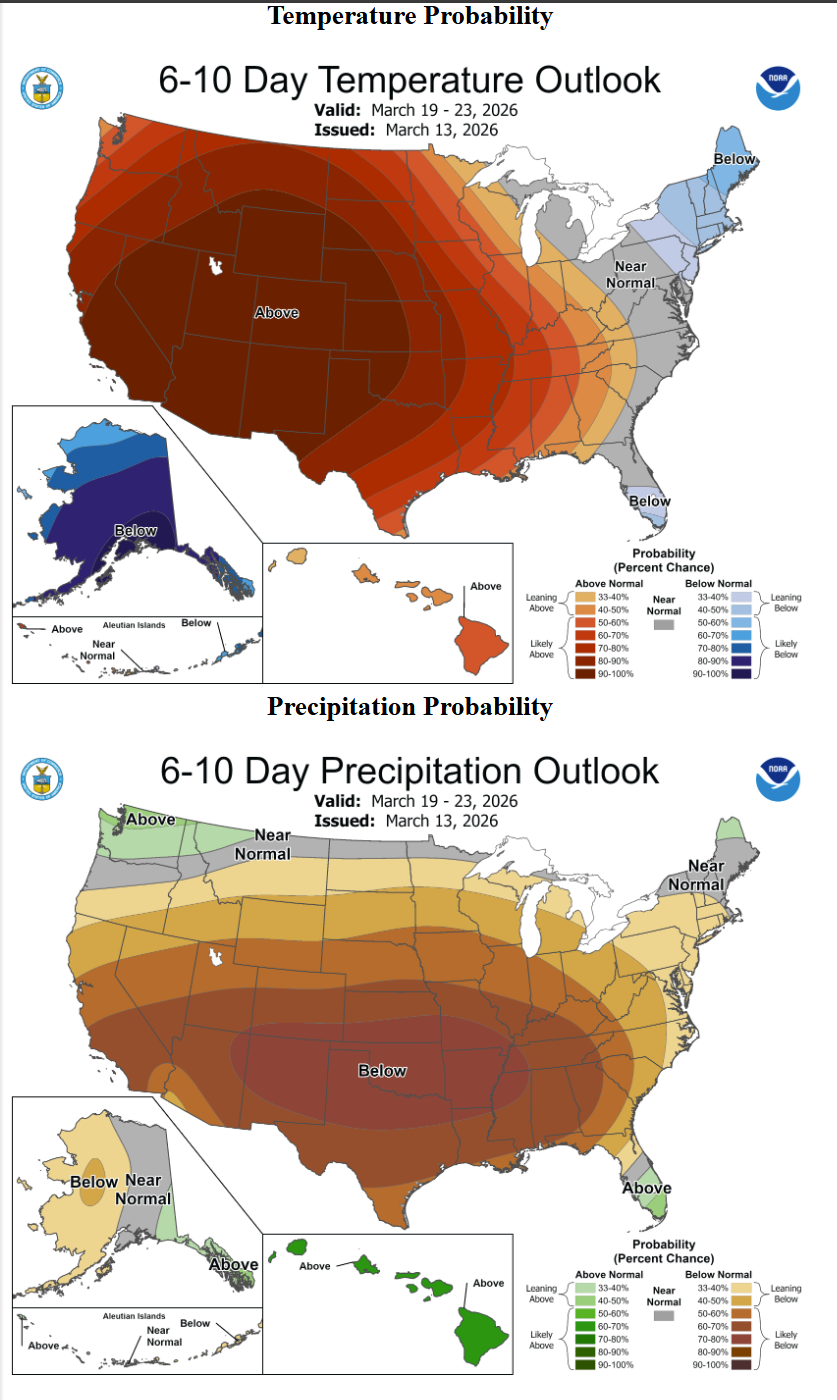

The corn market benefited from higher crude, which supported wheat. However, the wheat market alone has the drivers of conflict demand on its side as well as a freeze for the Southern Plains wheat areas on Sunday and Monday. While it is only mid-March, the heat and some recent moisture have accelerated growth out of dormancy in recent weeks, making the impact of freeze more concerning. On top of that, the drought situation across Oklahoma and Texas continues to spread with a dry and hot forecast ahead with highs in the 90s by late next week. These fundamental factors combined with an unpredictable oil market could lead to some meaningful upward price action next week.

On Friday, both the KC and Chicago wheat charts put in outside reversals higher suggesting that we could get follow-through into next week. The moves could potentially be significant to the upside if funds really start moving money into the ag commodities as inflationary pressures re-emerge from higher energy prices.

Corn futures rallied with the new crop December 2026 contract reaching $4.98 ½ on Monday’s high and closing just off that high at $4.91 ¾ after the strong recovery on Friday. I think it’s a possibility that we see above $5.00 new crop corn futures this next week, depending on the Middle East situation. The all-important USDA March Planting Intentions report is coming up on March 31st.

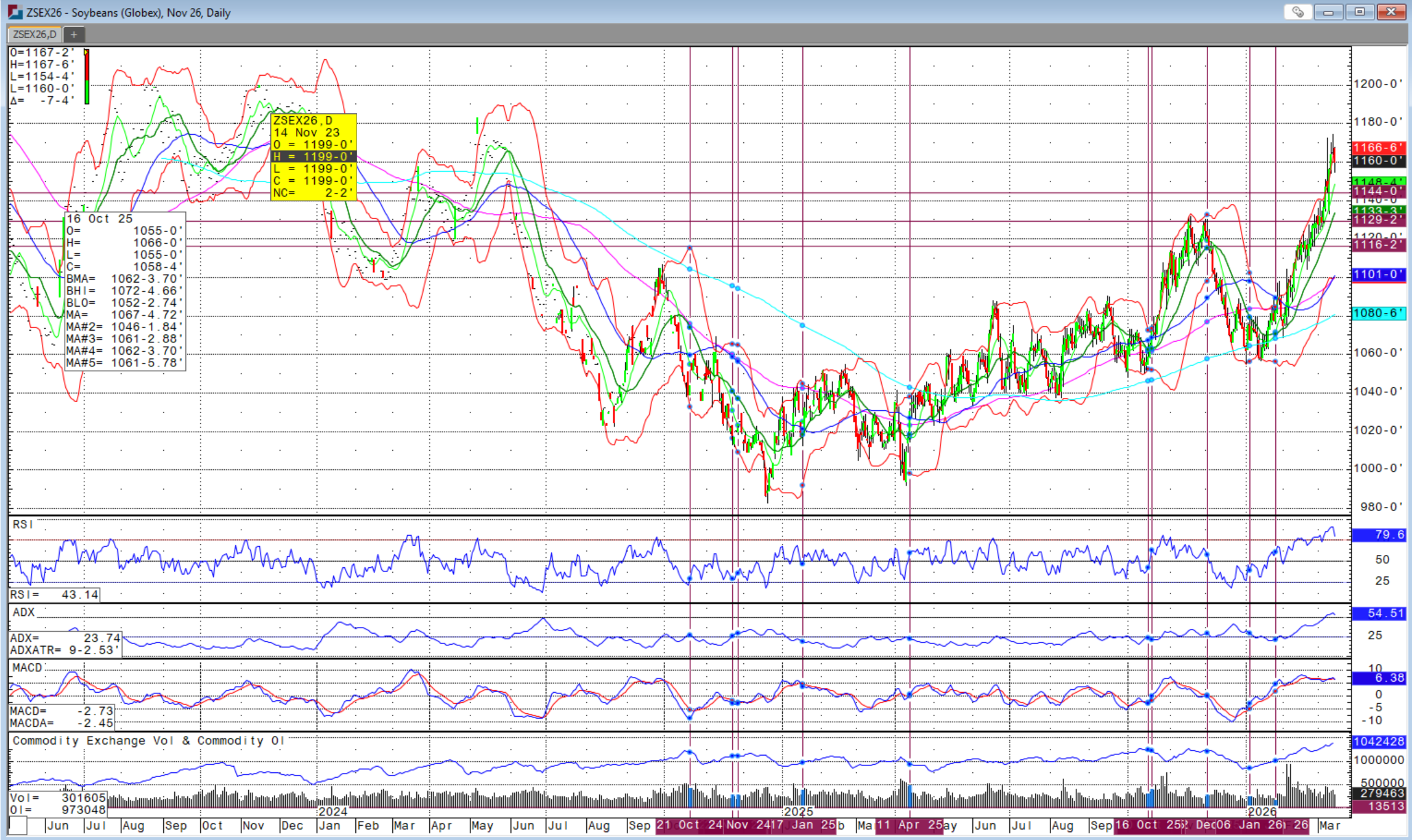

New crop November soybeans struggled towards the end of the week to hold gains, but still managed to close at $11.60 after making a high on Thursday at $11.74 ½. It is still unclear if President Trump will be making the trip to China at the end of March to meet with President Xi, but the soybean market will be paying very close attention to trade that news. Interestingly, China this week started cracking down on Brazilian soybean imports due to purity and weed issues. Could this be in preparation for more China purchases of US soybeans ahead of or during President Trump’s potential visit as a gesture of a continued truce? Perhaps.

The US dollar has surged back above 100.00 to finish the week, not seen since November 2025. That could be a headwind for US grain exports if and when the crude oil market calms down although such circumstances may also see the US dollar index weaken in tandem. The Federal Reserve FOMC meets this next week with the interest rate decision on March 18th. In light of the energy spike in particular, the broad consensus is for a pause in any interest rate change, especially with the February US CPI rising to 2.4 percent, unchanged from January, but still above the long-term inflation objective of 2.0 percent.

USDA’s monthly Crop Production and WASDE reports were released on Tuesday. US corn ending stocks were lower than expected, but unchanged from last month. Ending stocks were higher than expected for soybeans and wheat, but also unchanged from last month. The Brazil soybean crop was unchanged at 180.0 MMT while a slight decrease was expected. Brazil’s corn crop increased slightly above last month, but less than expected. Argentine corn and soybean crops declined less than last month and were also lower than expectations.

Global corn ending stocks increased above last month and expectations. Global soybean ending stocks decreased slightly from last month, but not as much as expected. Global wheat ending stocks declined more than unchanged expectations. The Australia wheat crop was lowered while Argentine wheat exports increased. EU, Russia and Ukraine wheat exports were lowered while Ukraine's wheat crop increased.

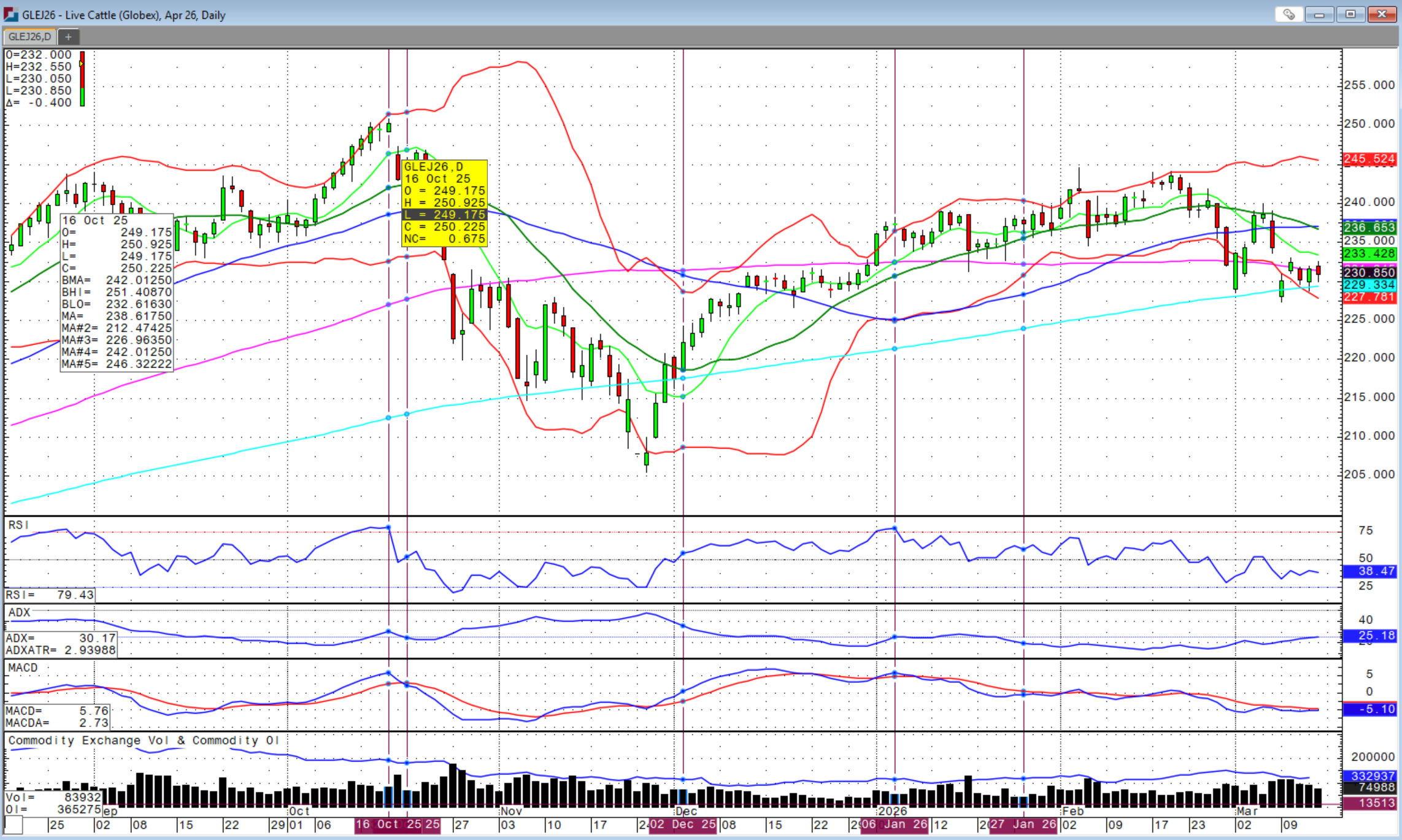

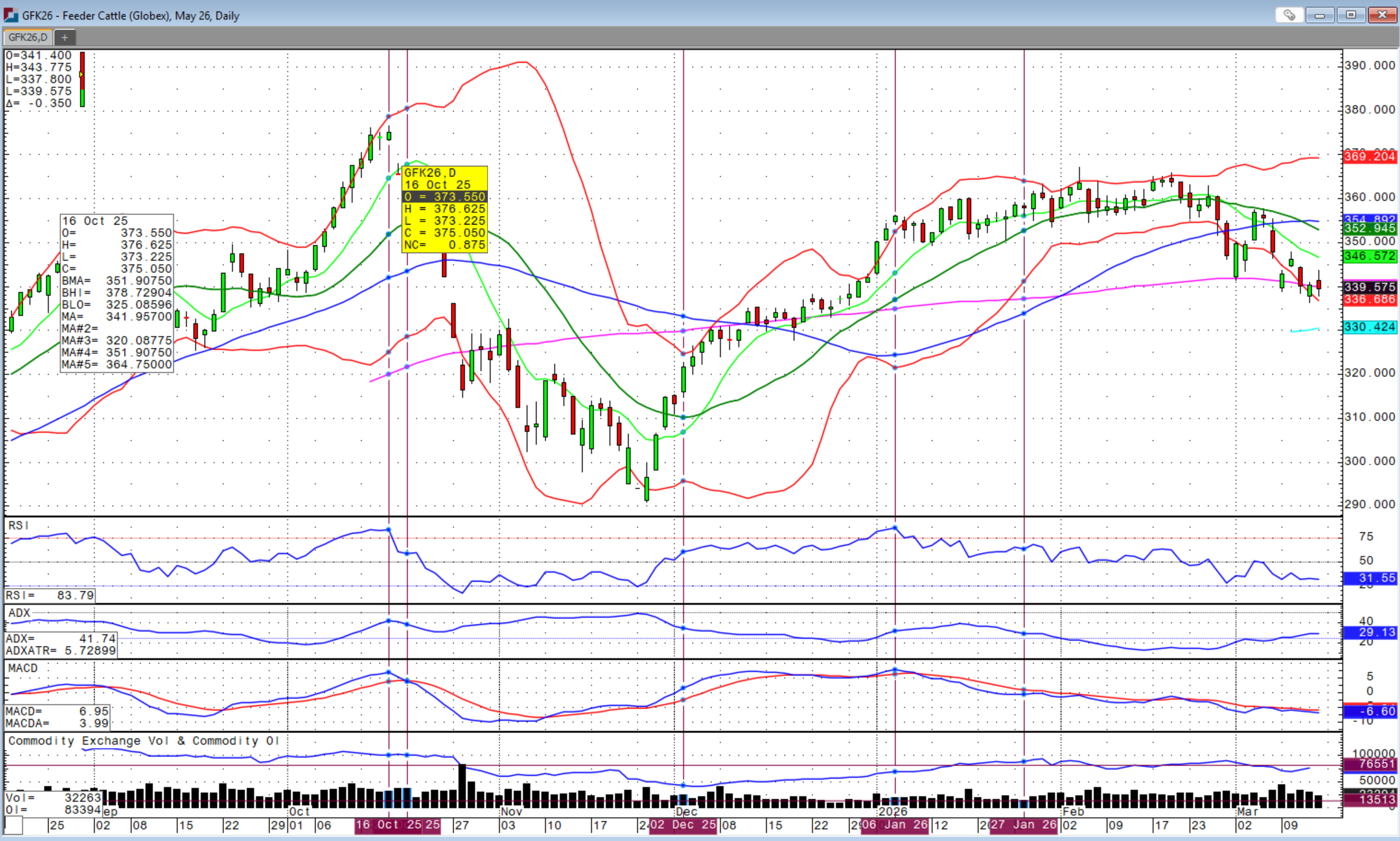

The cattle market has held up reasonably and surprisingly well considering all of the rhetoric from the war and continued headlines of the JBS Greeley plant strike that has been scheduled for this next Monday. Fed cattle cash trade was light and lower this week topping out at $235 in Kansas. The JBS Greeley plant has been shut down this week ahead of the strike with cattle shifted to other plants. Certainly, a negotiating tactic and surprising that it did not have a greater impact on cattle futures.

Markets gapped lower and opened limit down on Monday, but managed to close positive and well off the lows. While there were some mid-week setbacks, the cattle market held its ground well considering all the noise and volatility in the markets. This next week will be another large run of cattle in sale barns and a rebound in the stock market would go a long way in providing underlying support to cattle futures. Even if we should continue to see choppy, sideways trade, I believe this market will rebound once we can get some risk off trade back into the markets.

However, it may take the Iran situation to calm down considerably for that to happen. Personally, I feel this conflict could drag out longer than expected as I think it already has for some in the Administration. The equity market has been extremely resilient, especially considering high valuations and so, psychologically, we could soon get to a place where the market internalizes the fact that the conflict will continue, but the worst is over and oil prices will stabilize. That would be welcome news for the cattle complex.

Even if the JBS Greeley strike goes forward on Monday, that could be priced in at this point and any news of a deal could become bullish. But I will say it again, there are a lot of cattle coming to market at the moment and it is a reason for futures to come under pressure. With summer grilling season right around the corner, I think demand is going to start picking up again and therefore, any weakness could be short lived after any short-term period of larger runs. The cash market in sale barns continues to be strong, making heifer retention difficult. The top of this market could very well not be in yet.

If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)