Shares of Navitas Semiconductor (NVTS) have rallied significantly, rising more than 300% over the past year. The significant upmove in NVTS stock is driven largely by the company’s strategic shift toward high-growth power semiconductor markets.

Navitas Semiconductor designs next-generation power semiconductors used in power conversion and charging systems. Its core technologies include gallium nitride (GaN) power integrated circuits, high-voltage silicon carbide (SiC) devices, and high-speed controllers that improve efficiency and performance in modern electronics.

Over the past year, the company has intentionally reduced its reliance on markets such as mobile and low-end consumer businesses. While this shift weighed on near-term revenue, it significantly improved the company’s long-term positioning.

Management is now concentrating on high-power applications where GaN and SiC technologies can deliver meaningful growth. The company is targeting four core growth areas, including AI data centers, energy and grid infrastructure, performance computing, and industrial electrification. These markets collectively represent a massive serviceable addressable market for the company and are expected to expand rapidly.

Further, AI is the key catalyst across all its target markets, and its rapid expansion is likely to create solid demand for Navitas’ products and solutions.

Early Signs that Navitas’ Strategy Is Working

Navitas closed 2025 with a notable milestone. In the fourth quarter, revenue reached $7.3 million, surpassing management’s internal guidance but declining year-over-year due to the company’s shift away from low-growth markets. More importantly, high-power markets accounted for the majority of revenue for the first time.

The shift away from mobile charging is also happening quickly. Mobile applications accounted for a majority of revenue in the third quarter but dropped to less than 25% in the fourth quarter. Management expects that segment to continue shrinking and become largely insignificant by the end of 2026.

Looking ahead, Navitas is guiding for sequential growth in its top line starting in the first quarter of 2026, with continued momentum expected throughout the year as adoption in high-power markets accelerates.

AI Data Centers: A Major Growth Engine for Navitas Semiconductor Stock

One of the most promising opportunities for Navitas is in AI data centers, where power efficiency has become a critical constraint. The massive compute density required for AI workloads demands more advanced power architectures, and GaN technology is increasingly viewed as a solution.

Navitas has been accelerating product sampling for several AI-focused designs, and more than a dozen customers are currently evaluating these solutions. Also, its focus on introducing a new GaN design platform positions it well in the AI infrastructure ecosystem.

On the silicon carbide side, the company is supplying 1.2-kilovolt SiC devices for power supply units used in AI data centers, leveraging its latest generation technology to improve thermal performance and efficiency.

Energy Infrastructure and Electrification

Beyond data centers, Navitas is targeting the transformation of global energy infrastructure. The power grid is undergoing modernization as electricity demand rises and AI accelerates power consumption. This trend is expected to unfold over decades, creating a durable growth opportunity.

Navitas is developing ultra-high-voltage SiC modules for grid and energy applications. These solutions are currently being evaluated by original equipment manufacturers globally, with particularly strong activity in the U.S. and Europe.

Meanwhile, GaN adoption is growing in performance computing. The company already has more than 15 projects in production for high-power laptop and computing chargers, along with dozens of design wins in development.

Industrial electrification is another emerging opportunity. Applications include industrial pumps, heavy equipment electrification, DC-DC converters, and high-power charging systems.

Navitas Stock: Valuation Concerns After the Rally

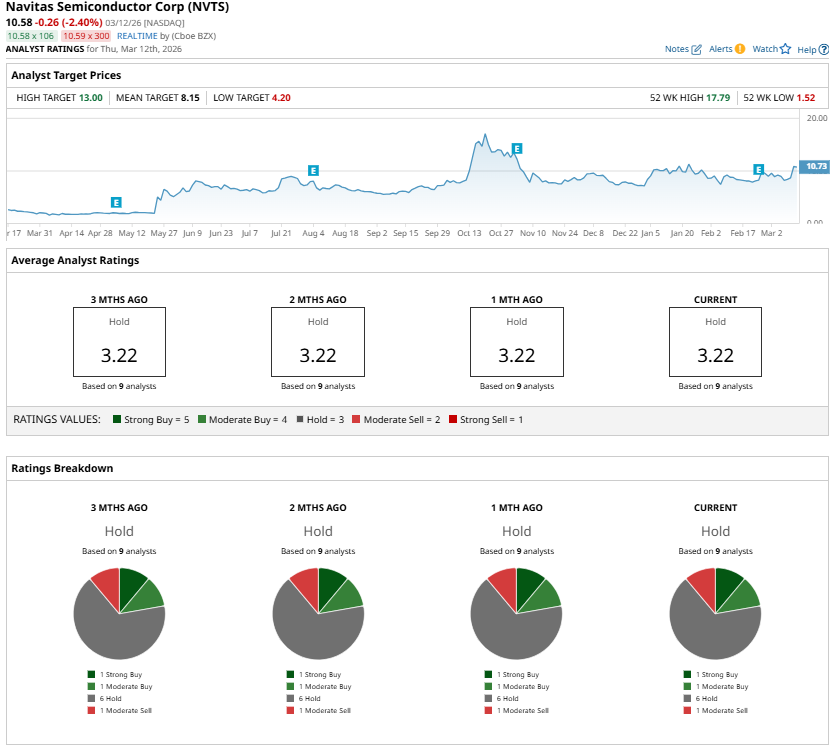

Despite the promising growth drivers, Navitas's stock’s extraordinary run has made analysts cautious. Navitas currently carries a consensus “Hold” rating from Wall Street. At the same time, the highest price target of $13 implies roughly 20% upside in NVTS stock from recent levels.

Conclusion

Navitas Semiconductor’s explosive rally is supported by its pivot away from consumer charging and toward high-power markets, which appears strategically sound and is already showing early results.

That said, the stock’s sharp rally suggests that a significant portion of this optimism may already be reflected in its current valuation. Another important consideration is that the company has not yet reached profitability, which could constrain near-term upside.

Navitas is still in the early phases of scaling its technology and market presence. If the company successfully converts its technology and growing design wins into consistent revenue growth, the stock, currently trading under $20, could see meaningful long-term appreciation. At the same time, investors who have already benefited from the recent run-up may want to consider locking in part of their gains.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)