/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Following Morgan Stanley's move to move on from Micron as its top pick, I had made a case in my latest piece as to why, in the larger scheme of things, nothing dents the bullish case for the memory chip major. However, what about their latest favorite, the world's biggest company, Nvidia (NVDA)? Well, the rationale for the firm's latest stance on the chip major is rather tactical—they believe that the current demand scenario for memory is “exceptional” and things will get back to normal soon. The consequent beneficiary: Nvidia, as the chip giant is a consumer of memory chips on a large scale, and lower prices for the same will only be a good thing.

However, what the Jensen Huang-led company has proven in recent years in its journey to become a $4.4 trillion market cap mammoth is that it has become almost indispensable in the realm of AI. A testament to that is that even amid overblown fears of overvaluation among AI stocks, shares of Nvidia are up 56% over the past year. Though at first glance and in relative terms, NVDA does seem to trade at elevated valuations, it appears that the market remains convinced about its prospects. Why? Let's find out.

Near-Perfect Financials

Nvidia has been handily beating Street expectations for a while now. However, in some of these instances, NVDA stock reacted negatively as the quantum of beat was not as per the expectations (crazy, right?).

So, with the results for its latest quarter, Nvidia delivered that as well, as revenues came in ahead of the consensus estimates by almost $2 billion, while earnings, as usual, beat Street expectations as well.

For the fourth quarter ended Jan. 25, 2026, Nvidia reported revenues of $68.1 billion. This was up 73% from the previous year and more than $3 billion from its earlier guidance. Data center revenues continued to accelerate, rising by 75% from the year-ago period to $62.3 billion as the company introduced its Rubin platform. Revenues from its erstwhile core segment of gaming also went up by 47% from the previous year to $3.7 billion.

Earnings, meanwhile, grew at an even faster tick of 82% in the same period to $1.62 per share, coming in ahead of the consensus estimate of $1.53 per share. Notably, this was the ninth consecutive quarter of earnings beat from the company.

Net cash from operating activities more than doubled to $36.2 billion from $16.6 billion in the year-ago period, as the company ended the quarter with a cash balance of $62.6 billion. This was much ahead of its short-term debt levels of just under a billion dollars.

For fiscal Q1 2027, Nvidia is projecting revenues to be about $78 billion, which would imply a year-over-year (YoY) growth rate of 76.9%.

Now to valuations, Nvidia is overvalued, but the overvaluation is not stark. While its forward P/E of 21.83 is almost comparable to the sector median of 21.63, its forward P/S and P/CF stand at 11.93 and 22.92, compared to the sector medians of 3.05 and 16.97, respectively.

Hard to Stop the Nvidia Juggernaut

Despite fears about hyperscalers developing their own chips (read: Google's TPU), they have a lot to catch up on Nvidia's GPUs, which are more widespread, can handle numerous different tasks, and have an established ecosystem. This has led to the Santa Clara-based company commanding a dominating market share of more than 90%.

So, what makes Nvidia a juggernaut? Well, Nvidia's sustained leadership in the accelerated computing sector is not merely a function of superior silicon but rather the result of a meticulously engineered full-stack ecosystem. At the hardware layer, the current Blackwell architecture and the upcoming Vera Rubin platform provide a generational leap in performance-per-watt and inference efficiency, effectively lowering the total cost of ownership (TCO) for enterprises.

Then, there is the CUDA (Compute Unified Device Architecture) software layer. With over five million registered developers globally, CUDA has become the industry standard for AI development. This creates a massive switching cost. Furthermore, Nvidia’s integration of high-speed networking (NVLink and InfiniBand) ensures that their chips do not just act as standalone components but function as a unified, data-center-scale engine. By offering a complete solution encompassing silicon and networking to specialized libraries and NIM (Nvidia Inference Microservices), Nvidia provides a capability that competitors struggle to replicate, reinforcing its position as the foundational utility of the AI economy.

Moreover, in a global environment upended by geopolitical upheavals, trade sensitivity, and supply chain fragility, Nvidia has established a unique strategic advantage through its "Sovereign AI" initiative. As nations like Japan, France, and Saudi Arabia seek to build domestic AI infrastructure to protect their data and cultural digital assets, they are turning to Nvidia as the trusted architect. This geographic diversification reduces the company’s historical reliance on a handful of US-based hyperscalers and creates a robust buffer against localized economic downturns.

Strategically, Nvidia’s move toward internalizing more of its supply chain, highlighted by multibillion-dollar investments in domestic U.S. optics and manufacturing partnerships like Lumentum, insulates it from some of the volatility inherent in traditional cross-border semiconductor logistics. While export controls, particularly regarding the Chinese market, remain a point of scrutiny, Nvidia’s aggressive annual product cadence allows it to pivot rapidly, releasing region-compliant hardware that maintains performance leadership. By positioning itself as a matter of national security and economic competitiveness for sovereign states, Nvidia has transcended its role as a hardware vendor to become a critical piece of global geopolitical infrastructure.

What Do Analysts Think About NVDA Stock?

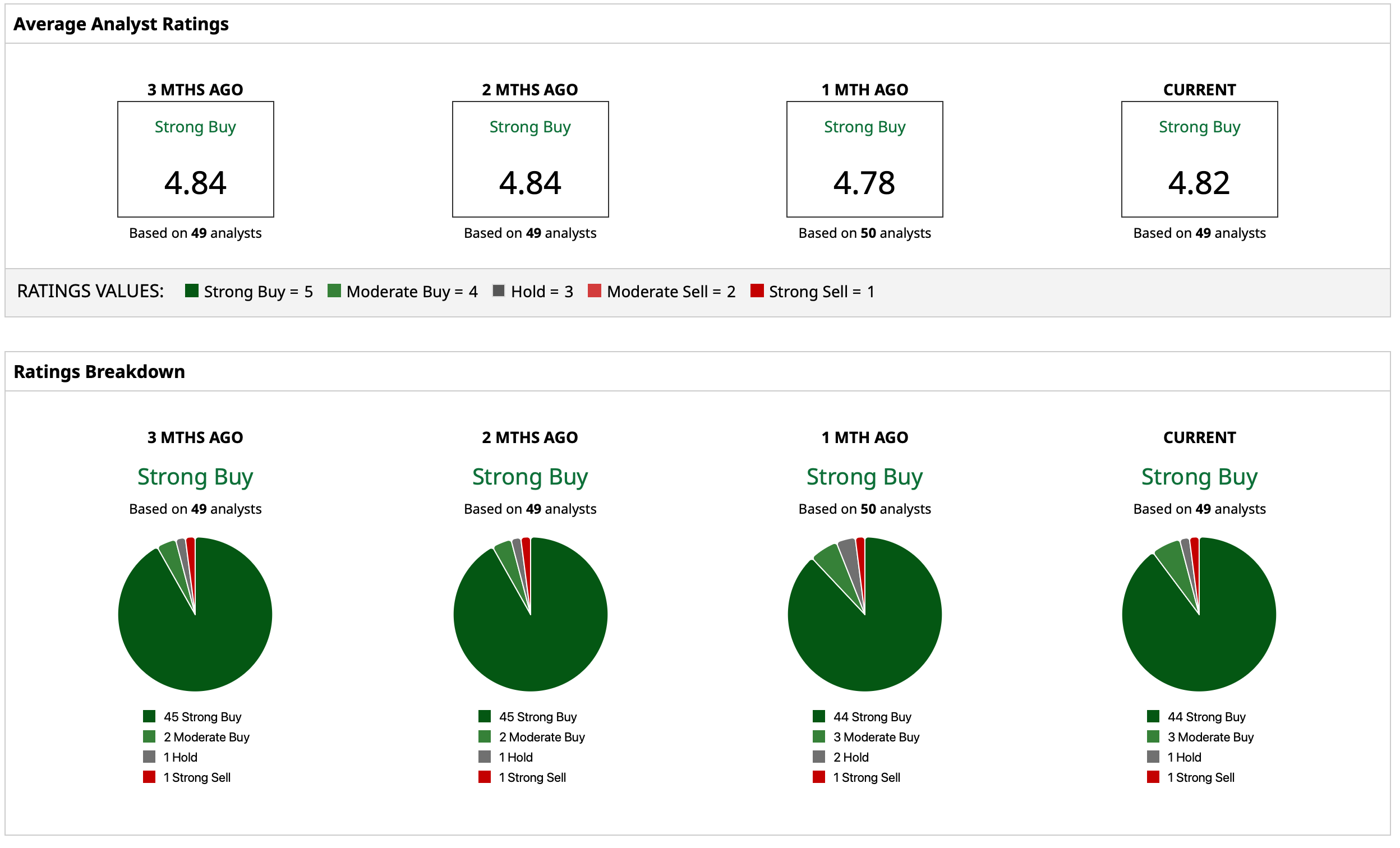

Thus, analysts have attributed an overall rating of “Strong Buy” for the NVDA stock with a mean target price of $264.38. This denotes an upside potential of about 44.4% from current levels. Out of 49 analysts covering the stock, 44 have a “Strong Buy” rating, three have a “Moderate Buy” rating, one has a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)