/Arthur%20J_%20Gallagher%20%26%20Co_%20billboard-%20by%20monticello%20via%20Shutterstock.jpg)

With a market cap of $57.9 billion, Arthur J. Gallagher & Co. (AJG) is a global insurance and reinsurance brokerage firm that provides risk management, consulting, and third-party property and casualty claims services to businesses and individuals worldwide. Operating through its Brokerage and Risk Management segments, the company delivers retail and wholesale insurance placement, reinsurance solutions, claims administration, and loss control consulting across a wide range of industries.

Companies worth more than $10 billion are generally labeled as “large-cap” stocks and Arthur J. Gallagher fits this criterion perfectly. It serves commercial, industrial, public, religious, and nonprofit organizations through an extensive global network of brokers and consultants.

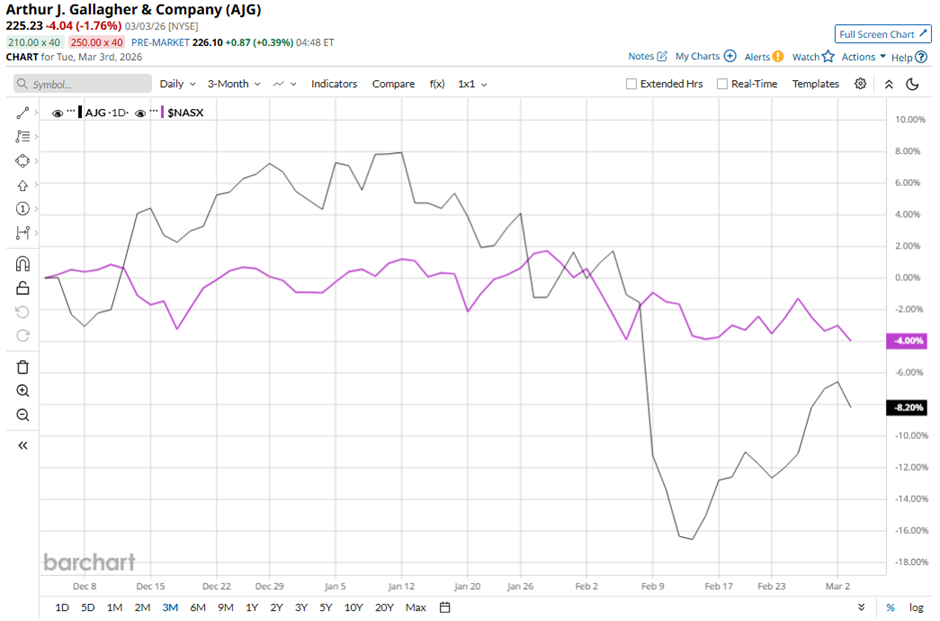

Shares of the Rolling Meadows, Illinois-based company have declined 35.9% from its 52-week high of $351.23. AJG stock has decreased 8.2% over the past three months, lagging behind the Nasdaq Composite’s ($NASX) 4% dip over the same time frame.

AJG stock is down nearly 13% on a YTD basis, underperforming NASX’s 3.1% decline. In the longer term, shares of Arthur J. Gallagher have dropped 34.1% over the past 52 weeks, compared to NASX’s 22.7% increase over the same time frame.

AJG stock has been trading below its 50-day and 200-day moving averages since early June 2025.

Shares of AJG rose 1.4% following its Q4 2025 results on Jan. 29 after the company reported 5% brokerage organic growth, 38% reported brokerage revenue growth, and 30% growth in adjusted EBITDAC, extending its streak to 23 consecutive quarters of double-digit EBITDAC growth. The stock reaction was further supported by management's reaffirmation of 2026 brokerage organic growth guidance of around 5.5% and its confidence in $160 million of annualized integration synergies by end-2026, with a longer-term target of $260 million to $280 million by early 2028.

In comparison, AJG stock has shown a more pronounced decline than its rival, Marsh & McLennan Companies, Inc. (MMC). MMC stock has fallen 1.5% on a YTD basis and 13.6% over the past 52 weeks.

Despite the stock’s weak performance over the past year, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from 23 analysts' coverage, and the mean price target of $283.74 is a premium of nearly 26% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)