/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOGL) closed 2025 with annual revenue exceeding $400 billion, reflecting the scale at which artificial intelligence (AI) is now embedded across its operating segments. The company’s AI-driven product enhancements, particularly within Search and Cloud, are translating into significant revenue acceleration, supporting its share price.

For instance, in Google Search, fourth-quarter revenue increased 17% year-over-year (YOY), reflecting higher engagement with AI Overviews and expanded AI-native query experiences. The key financial implication is twofold. First, AI integration appears to be strengthening search monetization. Second, improved engagement metrics suggest incremental pricing power in performance advertising.

YouTube has evolved into a solid, diversified media asset, and AI is transforming the experience. YouTube generated more than $60 billion in annual revenue across advertising and subscriptions. The platform’s scale provides resilience against cyclical weakness in the ad market, particularly as subscription revenue from YouTube Premium and other services grows.

The most significant acceleration occurred in Google Cloud, where Q4 revenue rose 48% YOY, bringing the segment to an annualized revenue run rate above $70 billion. Importantly, backlog expanded to $240 billion, driven by demand for AI products from multiple customers.

With Alphabet showing that AI is accretive to growth across its business segments, should you buy GOOGL stock today?

AI Is Set to Push Alphabet's Revenue Higher

Alphabet entered 2026 with AI at the center of its growth strategy, driving performance across both its consumer and enterprise businesses.

AI is now deeply integrated into Search, Cloud, and subscription products. Management has indicated that features such as AI Overviews and AI Mode are driving higher search activity, including growth in commercially valuable queries. Higher engagement could translate into advertising revenue.

User engagement has also improved meaningfully since the launch of Gemini 3. Higher user engagement strengthens Google's pricing power in advertising and increases the long-term value of its search franchise. In effect, AI is strengthening the durability of the company’s core revenue engine.

The Cloud segment remains key to earnings. Google Cloud is positioned to deliver strong results again in 2026, supported by sustained demand for enterprise AI solutions. Within Cloud, Google Cloud Platform continues to expand at a solid pace. The company is reporting improved win rates for new customers, larger contract commitments, and increasing spend from existing clients. All of this indicates strong growth ahead.

Enterprise AI products are now generating solid revenue. Growth is being driven by both AI infrastructure and AI applications. On the infrastructure side, the deployment of specialized hardware, such as TPUs and GPUs, is supporting large-scale AI workloads. On the solutions side, demand remains strong for advanced models, particularly Gemini 3.

Core GCP services are also making meaningful contributions. Infrastructure, cybersecurity, and data analytics offerings continue to benefit from enterprises modernizing their technology stacks and consolidating vendors.

Alphabet’s subscription ecosystem is strengthening recurring revenue streams. Growth in paid offerings such as Google One and YouTube Premium adds diversification and improves revenue visibility.

In short, AI is strengthening the company's competitive moat. AI is increasing engagement in Search, accelerating enterprise adoption in Cloud, and deepening subscription penetration across consumer services, positioning Google to sustain durable top-line growth into 2026 and beyond.

Is GOOGL Stock a Buy Today?

Alphabet's recent financial performance shows that AI is a tangible growth catalyst for the company, embedded across Search, Cloud, and YouTube. Revenue acceleration in core segments, expanding enterprise AI demand, and strengthening recurring revenue streams suggest that its AI investments are translating into solid returns.

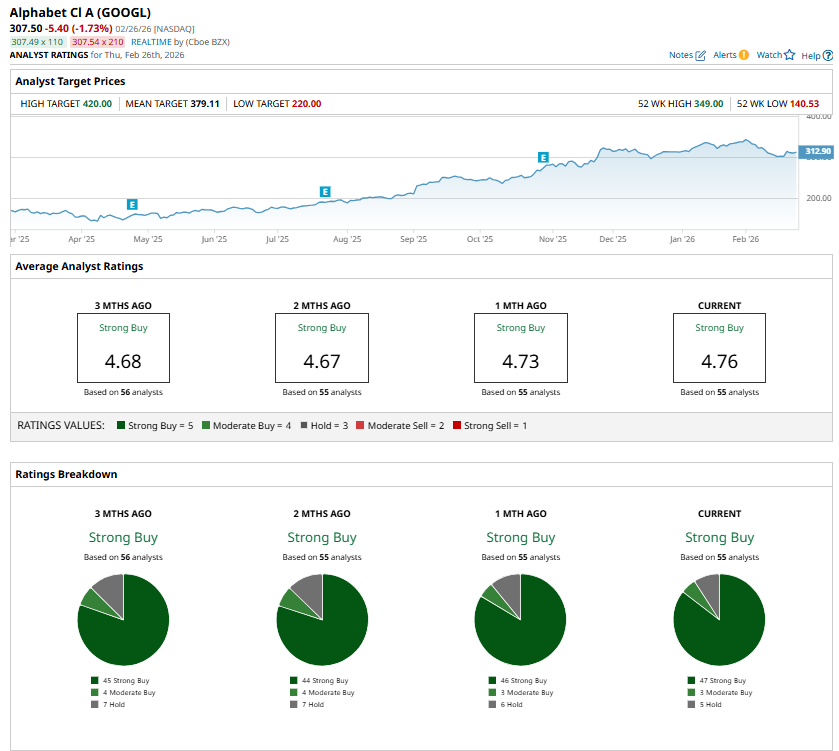

Further, analysts broadly maintain a “Strong Buy” consensus rating, reflecting confidence in Alphabet’s long-term potential.

However, with GOOGL shares up roughly 79% over the past year, a significant portion of the AI-driven optimism is arguably reflected in the current price. Additionally, capital expenditures are rising meaningfully as Alphabet invests in AI. While these investments are strategic and will potentially generate solid returns over the long term, they may compress margins and moderate near-term earnings growth, limiting upside potential.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Visa%20Inc%20gold%20card-by%20hatchpong%20via%20iStock.jpg)