Howdy market watchers!

How is the end of February already here! It sure doesn’t feel like it with highs in the 80s and plenty of sunshine!

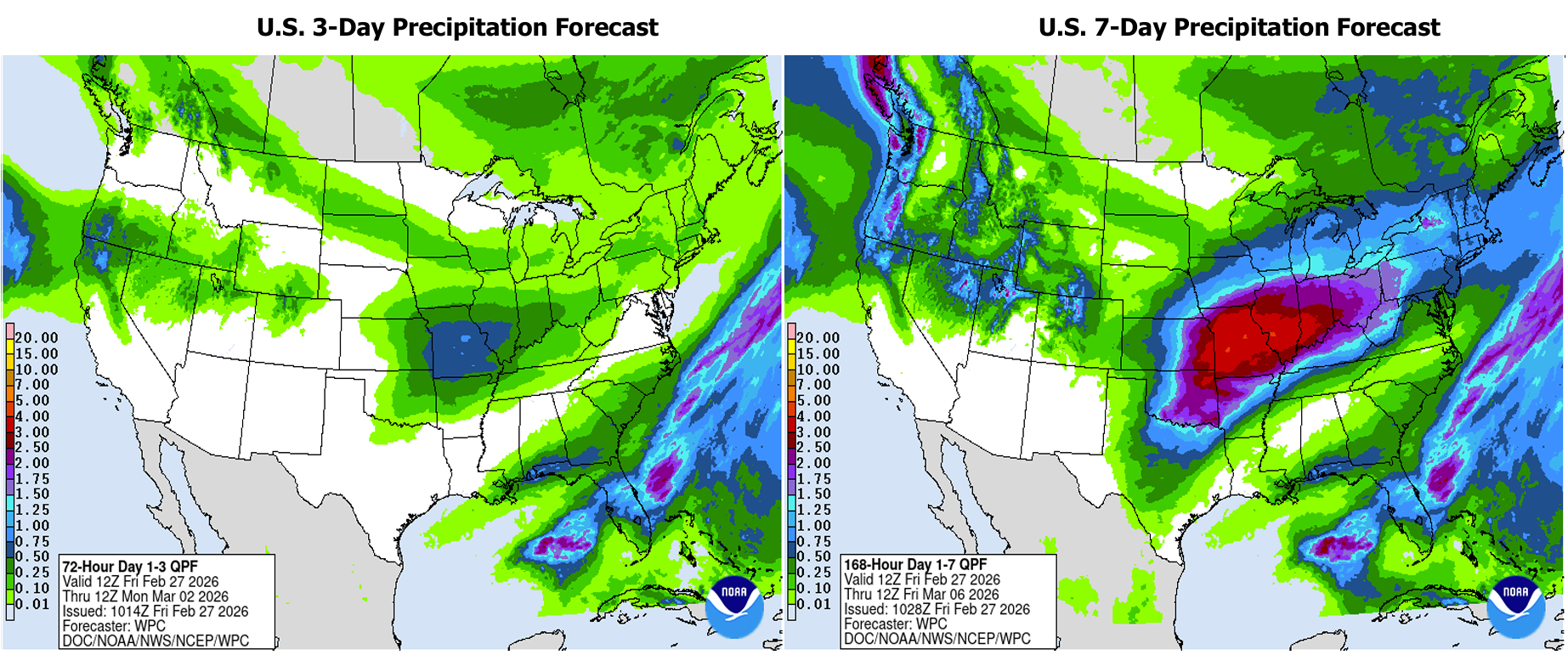

We are so hopeful that the heavy rains in the forecast will come true mid-next week as it is greatly needed! The entire state of Oklahoma is in some level of drought as is much of the country. The threat of wildfires remains high and we could sure use a good soaking rain to reduce such risk not to mention the growing crops and those about to be planted. It is prime time to topdress wheat ahead of this rain with warm temperatures for sure bringing wheat out of dormancy.

While the crop insurance deadline says that you need to take cattle off wheat on or before March 15th due to first hollow stem, be sure to check your own wheat as warmer than usual winter could advance that date and impact yield if cattle are left out until that date.

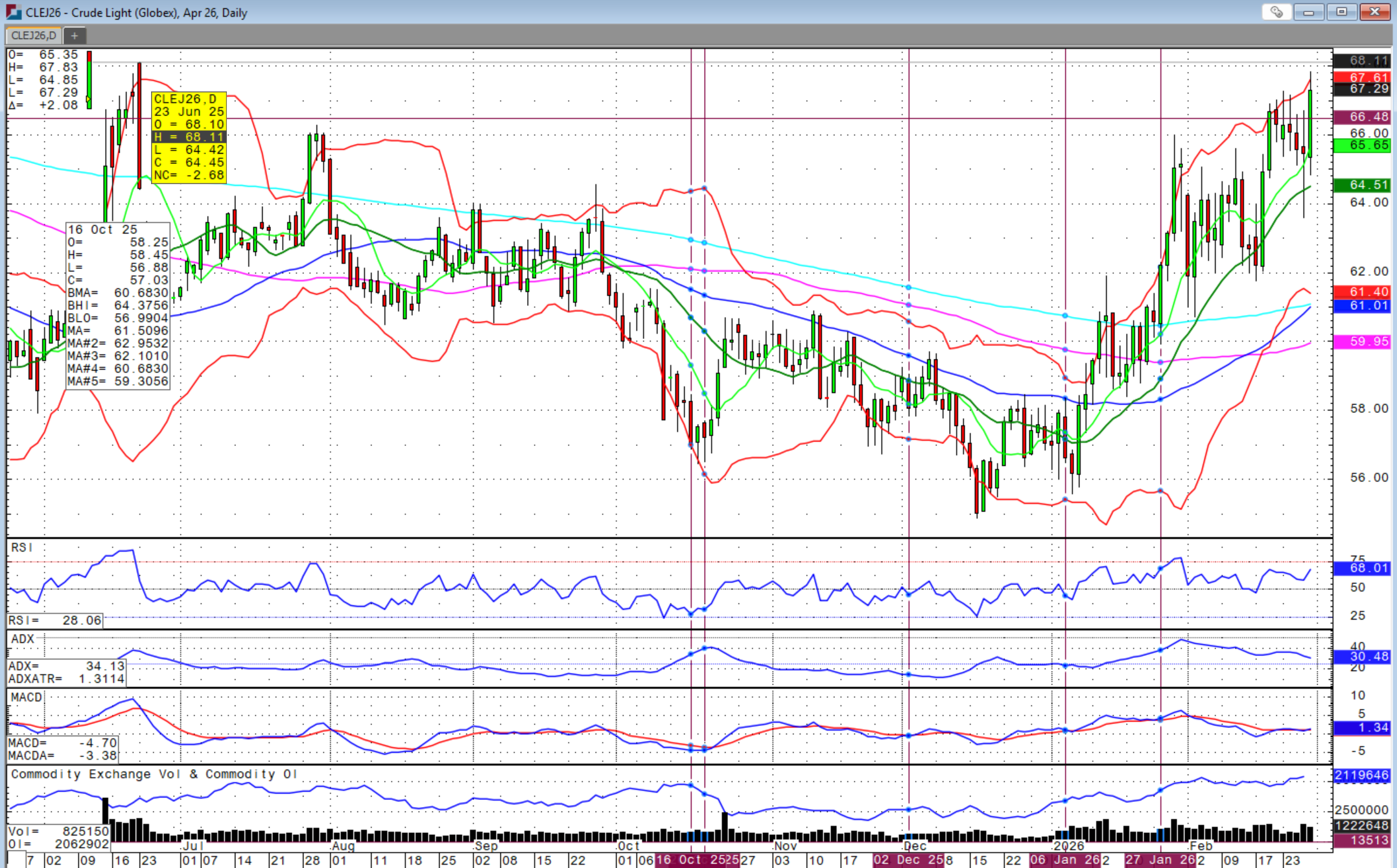

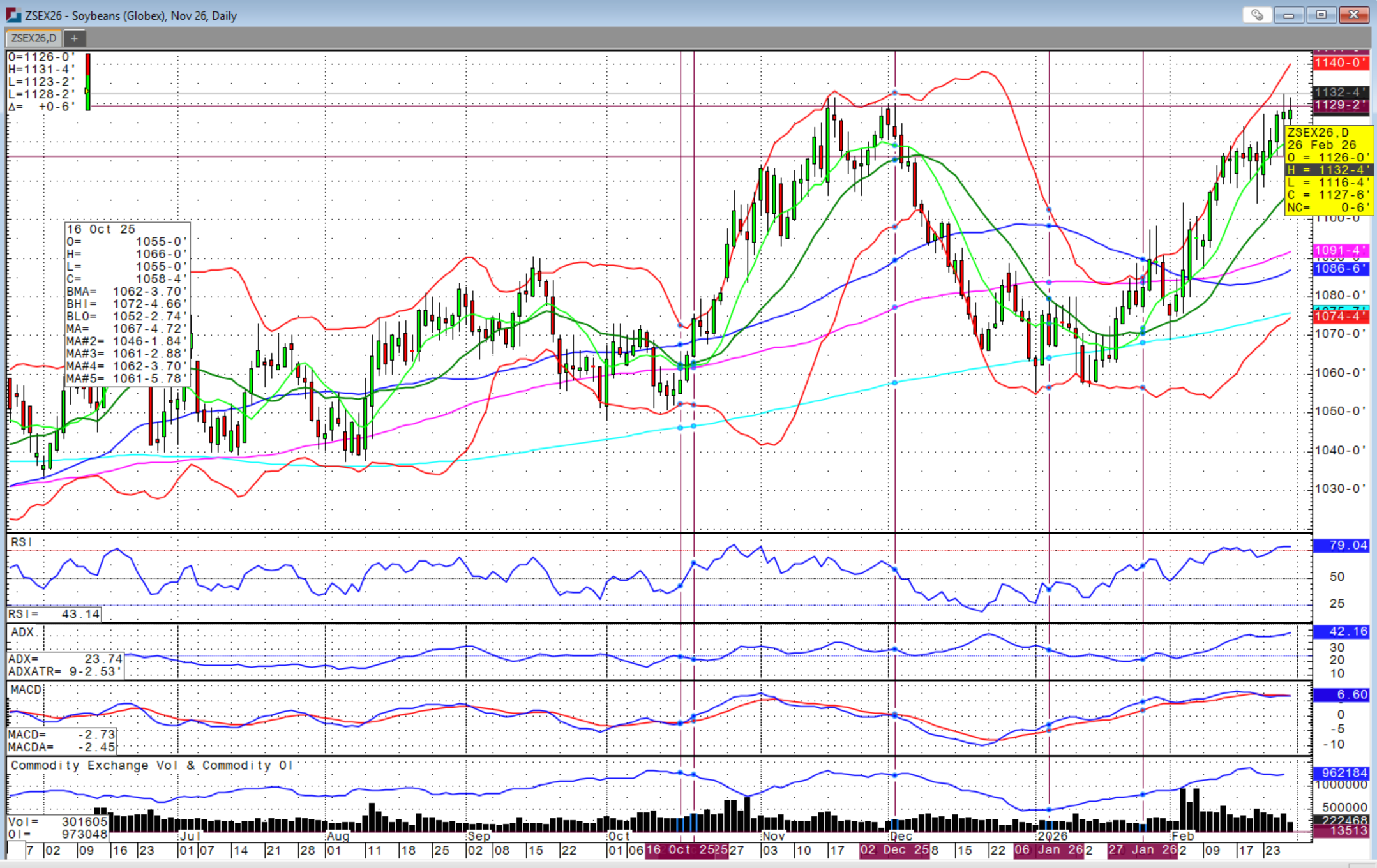

It is becoming more difficult to decide if graze-out or harvest is the best strategy for wheat this year. The wheat market has staged an impressive rally the past two Friday’s with concerns over escalation of the Iran tensions and potential for less rainfall in Western Kansas. There also seemed to be a shift of managed funds to the commodity complex this week perhaps from equities although the US dollar chopped sideways in a fairly tight range.

As warnings for Americans to evacuate Iran and Israel widen this week, there is increasing concern that an attack may be preeminent. Diplomacy made another attempt this week in Geneva although inconclusive with President Trump expressing frustration, but agreeing to more time. Patience is running thin. The Muslim ‘lent’ named Ramadan that is underway ends on March 30th, but it is unclear if the Trump Administration would wait until that time to take action should talks fail. Last week, the US said the deadline was in 10-15 days. However, as we now know, the attack has taken place overnight with this article written prior to that attack.

We will likely now see the Strait of Hormuz closed until tensions simmer. While Iran retaliated with attacks on Middle East locations including US air bases in the region, the extent of continued fighting and retaliation will determine the severity of market reaction. It is not yet certain if the Ayatollah Khomeini was killed in the attacks as is speculated, but that will likely be a critical item in terms of the length of this escalation.

The anticipation will likely continue to bring risk premium to the commodity complex, particularly oil, metals and wheat, to name a few. Such rally in agriculture commodities is welcome news for farmers although most of the grain is in the hand of commercials. However, it is a great time for farmers to watch new crop contracts to lock in prices above breakeven levels that have been difficult to reach in the past couple of years other than short windows of a spike.

As I have discussed at our recent road show meetings with Sidwell Insurance, it has never been more important to know your break evens and acceptable profit margin to begin protecting the downside in the price of the crop you’re producing. It can come and go so quickly that it is critical you have a target in advance as the opportunity may only present itself for a short time, which could be in the overnight commodity trade. If you would like help in calculating your breakeven or how to protect prices when they get to target levels, give us a call. It doesn’t matter where you are in the United States or what you are producing, the Sidwell Strategies team has experience and a network to support your cash sale and risk management needs.

Sidwell Strategies is now a StoneX brokerage after the completion of the acquisition of RJ O’Brien and we offer the full range of hedging, trading and investing tools for individuals as well as commercial customers and so give us a call for professional services offered locally.

Watch the coverage of rains this next week for direction on the wheat market. If western Kansas does not get broad coverage in addition to other parts of that state, we could see the rally continue. However, if rainfall expands, consider protecting the downside. Also, and perhaps as important, carefully monitor the fear factor of the Iran escalation. The wheat market is certainly being supported by short covering from geopolitical tensions, but should any peak fears fade or be delayed, we could see the risk premium from that and weather evaporate quickly.

While there are dry areas, the wheat still looks great for this time of year and wheat is a tough crop. Friday was First Notice Day for March wheat, corn and soybean futures, which means longs need to exit or roll to May or risk delivery. We can often see a rally on the day of and after First Notice Day, but it doesn’t necessarily indicate bullish technicals.

Corn and soybeans are battling for acres with the ratio near the deciding point at 2.4, but more USDA payments being sent out could likely shift the preference to corn despite that price ratio. Domestic biofuel policy has created plenty of optimism and is indeed the solution to the incredible productivity of the US farmer amid a challenging and hyper-competitive export environment. The recent increase in energy markets makes the use of a year-round biofuel blend more attractive, but we also need to be prepared for the guardrails of how that will look if and when petroleum energy prices are lower.

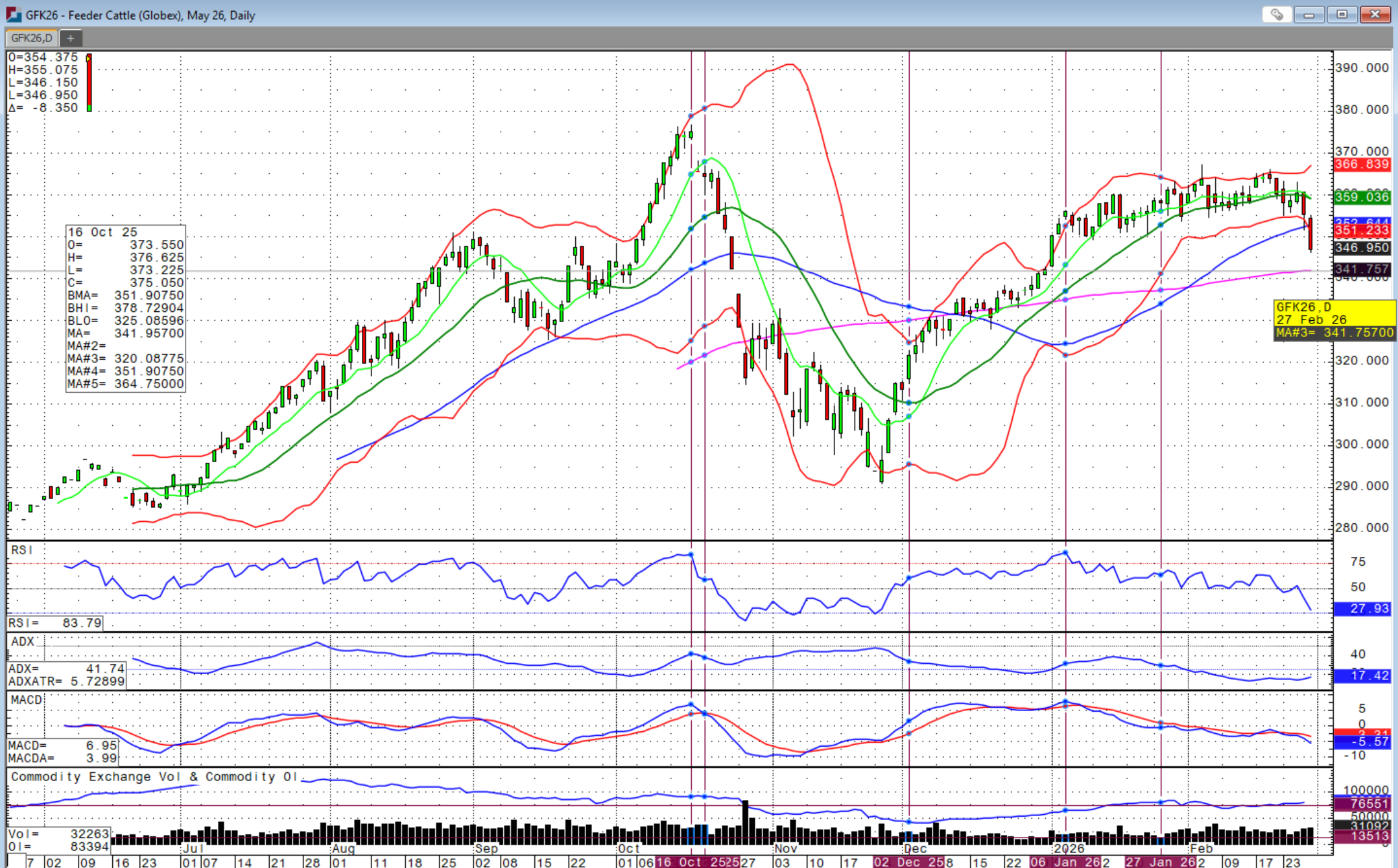

The cattle market did not finish on an encouraging note this week. The market action on Thursday and Friday was disappointing despite last Friday’s bullish Cattle-on-Feed report. However, weakness in the stock market, weaker-than-expected fed cattle cash trade at $244-245 versus last week’s $249 along with uncertainty surrounding the lingering potential of a strike by the labor union at the JBS packing plant in Greeley, CO, created enough uncertainty for sellers to take hold.

Escalation of the US-Iran conflict will likely be negative for the stock market as well as the cattle market. I have some concern of a larger number of heavy, slaughter-ready cattle amid slower slaughter numbers creating a short-term excess that allows some leverage to shift back to the packer. With February live cattle futures expiring that are trading at a premium to the April futures, there is a territory of basis exploration combined with ample front-end cattle in the immediate term that could see some liquidation in the cattle complex.

This is also the time of year when cattle are coming off wheat pasture that often results in some slippage in the feeder cattle futures and cash markets. While cattle supplies are tight overall, weights are increasing and it doesn’t prevent short-term pockets of excess supply that shifts the pricing leverage. The spring and summer grilling season are right around the corner, but it doesn’t mean that air pockets can’t exist.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall. If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)

/Salesforce%20Inc%20logo%20on%20building-by%20Sundry%20Photography%20via%20Shutterstock.jpg)