/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

Lumentum Holdings (LITE) is a leading designer and manufacturer of optical and photonic products powering cloud data centers, AI networks, telecom infrastructure, industrial lasers, and 3D sensing applications. The company supplies high-speed transceivers, lasers, and subsystems to major tech firms, enabling faster data transmission and advanced manufacturing in semiconductors, EVs, and displays.

Founded in 2015 as a JDS Uniphase spin-off, Lumentum is headquartered in San Jose, California, USA. It operates worldwide across the Americas, Asia-Pacific, Europe, the Middle East, and Africa.

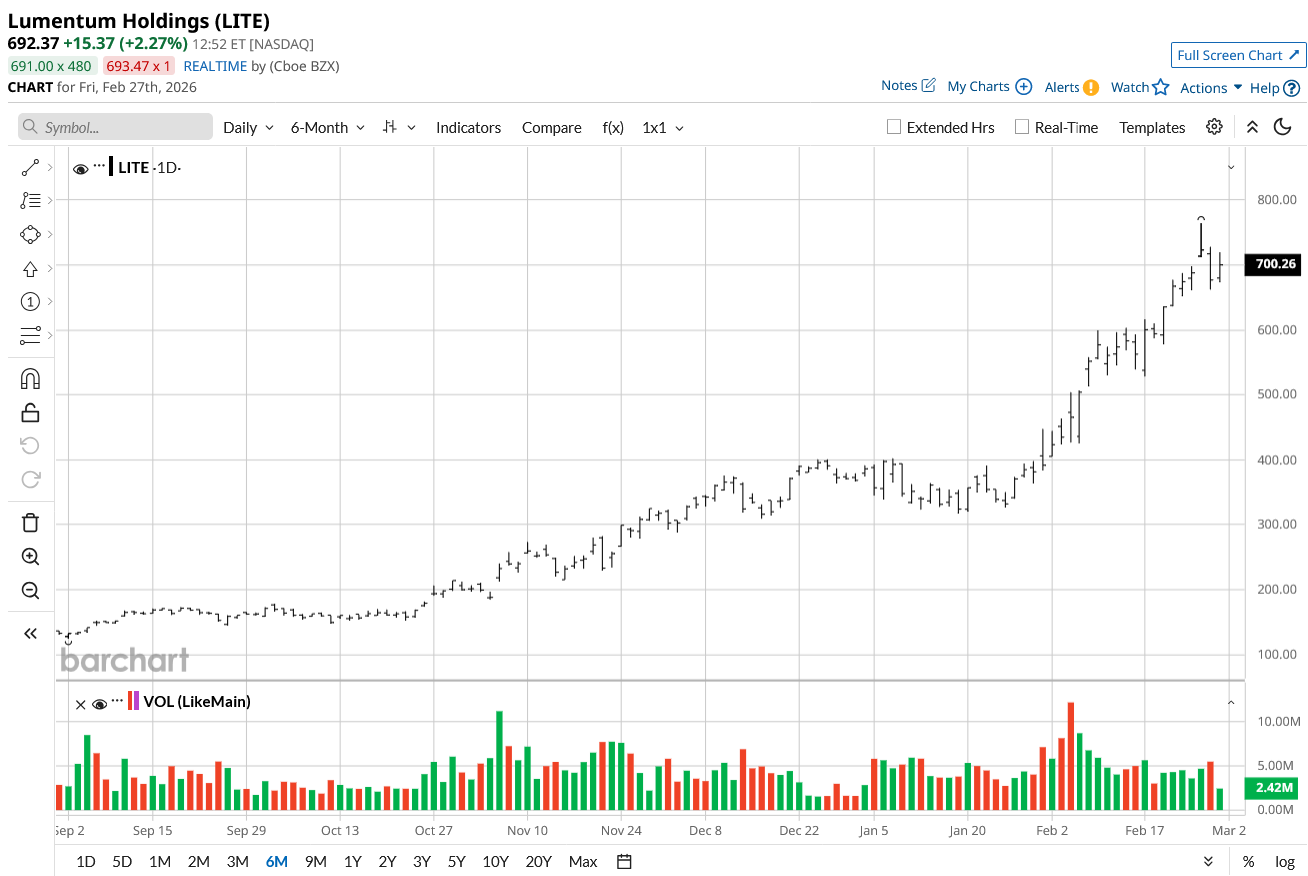

Lumentum Holdings Stock

Lumentum Holdings' stock has exploded on AI and data center demand, trading near $692 after massive rallies. It's up 5% over the past five days, soaring 90% in the last month and 128% in three months. Six-month gains hit 458%, year-to-date (YTD) 91%, and 52-week returns reached 1,438% from $45.65 lows.

Against the S&P 400 MidCap Index, Lumentum crushes it; the index gained 0.11% in five days, 3% monthly, 9% in three months, 11% in six months, and 8-15% YTD/52-week. LITE's multiples dwarf them, fueled by the optics boom vs. midcap steadiness.

Lumentum Holdings' Results

Lumentum Holdings announced second-quarter 2026 results on Feb. 3, 2026, marking a record quarter with net revenue of $665.5 million, up 65% year-over-year (YoY) from $402.2 million and 25% sequentially from Q1's $533.8 million. This beat estimates of $646.7 million. GAAP EPS was $0.89 (net income $78.2 million), while non-GAAP EPS hit $1.67, crushing the $1.39 consensus by 20%.

Segments shone: Components revenue reached $443.7 million (+68% YoY), driven by datacom lasers and AI chips; Systems $221.8 million (+60% YoY). Margins expanded sharply, GAAP gross 36.1%, non-GAAP 42.5% (up 1,020 bps YoY, thanks to utilization, pricing, and AI mix). Non-GAAP operating margin 25.2% (up 1,730 bps YoY), operating profit $167.7 million, adjusted EBITDA $198.3 million. Cash/short-term investments grew to $1.15 billion, and CapEx was $84 million for capacity.

For Q3 2026, Lumentum guides revenue at $780-$830 million (21% sequential growth midpoint), non-GAAP operating margin at 30-31%, and EPS at $2.15-$2.35. CEO Michael Hurlston highlighted the OCS backlog of over $400 million and a multi-hundred-million CPO order for H1 2027, signaling AI inflection.

LITE stock surged 7% post-earnings.

Lumentum Upgraded by Citi Analyst

Citi analyst Papa Sylla maintains a “Buy” rating on Lumentum with an $800 price target (from $560), signaling an upside potential of 16% from the market rate. Shares rose over 2% premarket on Wednesday as Citi added LITE to its upside 30-day catalyst watch ahead of OFC.

Sylla expects Lumentum's management to share stronger-than-expected OCS and CPO revenue forecasts or market size projections, potentially leading to upward revisions in long-term revenue guidance. He also sees potential announcements of new CPO/OCS deployments by Lumentum or its major customers, as these technologies approach broader adoption.

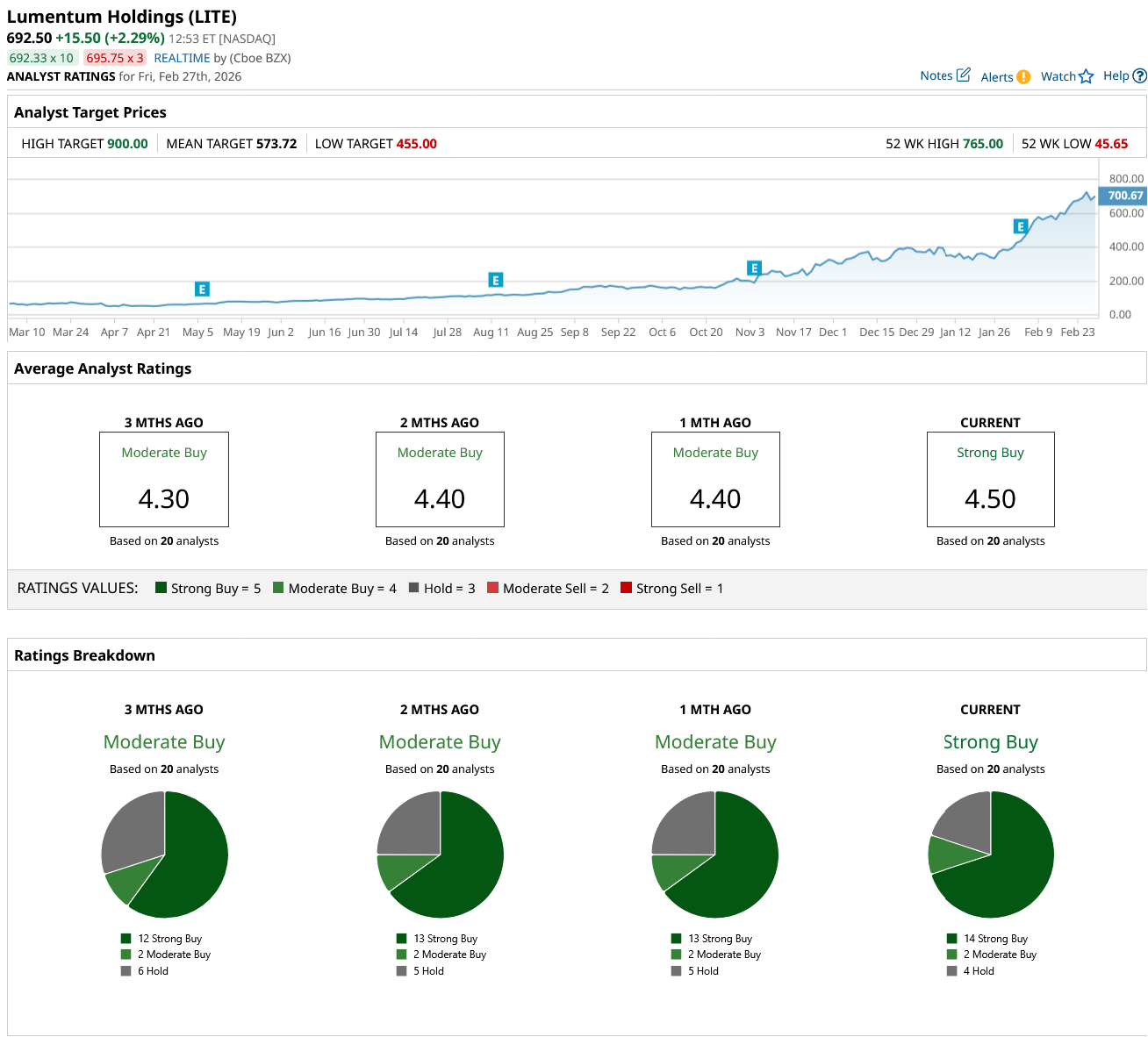

Should You Buy LITE Stock?

Lumentum Holdings has been a standout multibagger this year, hitting all-time highs as analysts race to keep pace. LITE stock now carries a consensus "Strong Buy" rating, upgraded from "Moderate Buy" last month, signaling growing analyst optimism. However, the mean price target of $573.72 implies a 17% downside from current levels, highlighting how targets lag the stock's rapid surge.

LITE stock has been rated by 20 analysts, receiving 14 “Strong Buy” ratings, two “Moderate Buy” ratings, and four “Hold” ratings.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)