Cybersecurity stocks rarely unravel on a headline that does not involve a breach. This time, a product launch lit the fuse. When Anthropic unveiled Claude Code Security, an automated artificial intelligence (AI) tool that scans codebases for vulnerabilities, investors wasted no time heading for the exits on Feb. 20. Within minutes, cybersecurity names slid sharply.

That wave of selling dragged shares of Okta (OKTA) down by 9.2% following the announcement. Yet the market’s knee-jerk reaction tells only half the story. Okta has not drifted through this cycle. It has delivered measurable financial progress and reshaped itself into a disciplined, profitable enterprise software company.

The bigger narrative revolves around agentic AI. Enterprises are racing to deploy autonomous software agents, and every one of those agents needs an identity layer. Okta has moved early and decisively. Its Q3 fiscal 2026 performance underscored that momentum, and the launch of Auth0 for AI Agents signaled clear intent.

Against this backdrop, let us discuss whether the recent stock price dip signals weakness or opens a door for long-term investors.

About Okta Stock

The San Francisco, California-based Okta provides cloud-based identity and access management solutions to enterprises. With a market cap of $13.3 billion, the company enables secure user authentication, single sign-on, multi-factor verification, API security, device access, and identity governance.

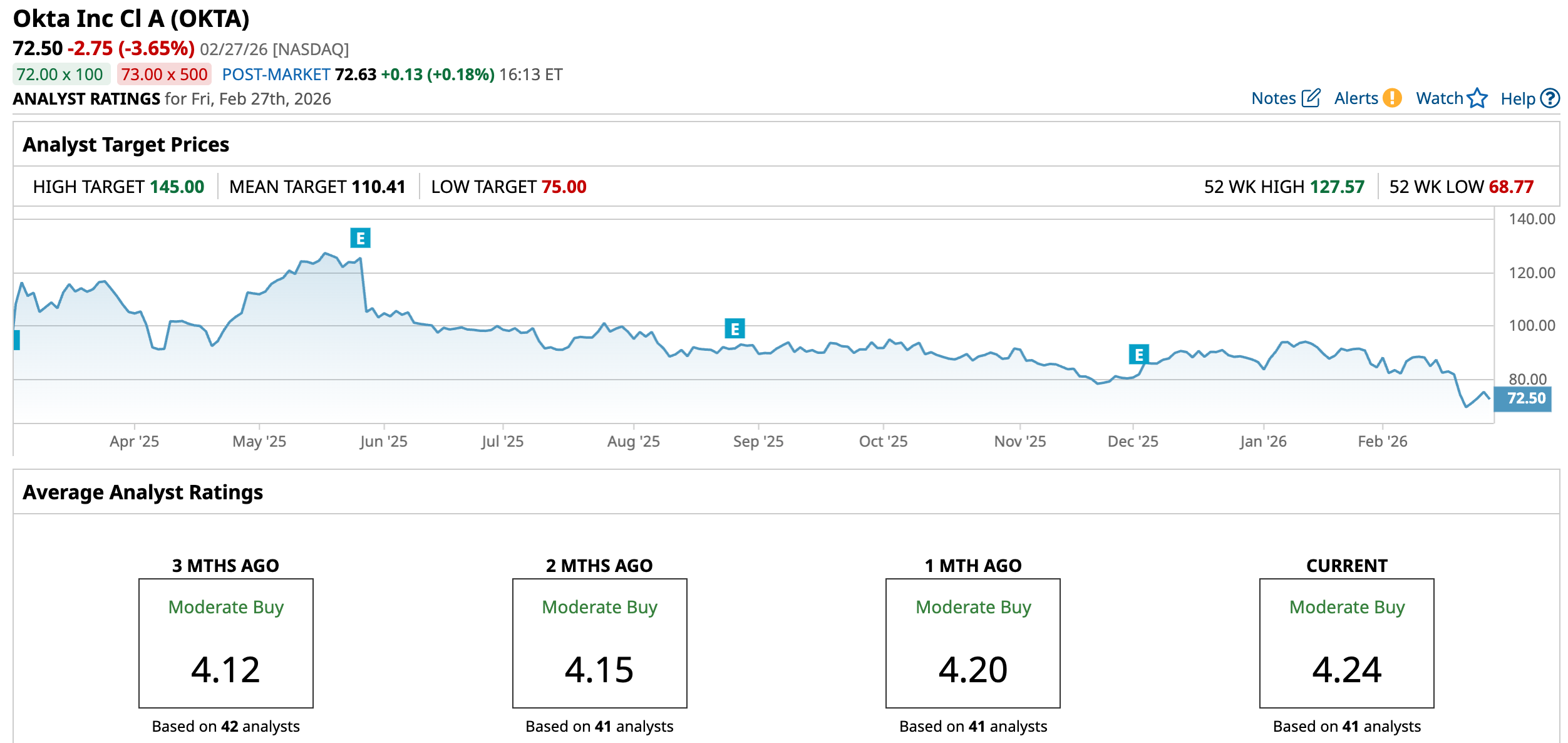

Its platform allows organizations to manage workforce and customer identities seamlessly across applications, devices, and cloud environments. However, the stock has struggled. Over the past 52 weeks, shares have fallen almost 18.7%. The decline deepened to 22.06% over the past six months, and the last three months alone brought a 10% drop.

From a valuation standpoint, OKTA stock is currently trading at 21.87 times forward adjusted earnings. The multiple is trading below both the industry average and the company’s own five-year historical average. For long-term investors who believe Okta can sustain double-digit growth while expanding margins, this reset might open a calculated entry point.

Okta Surpasses Q3 Earnings

On Dec. 2, 2025, Okta reported Q3 fiscal 2026 results that shifted the narrative, at least briefly. The stock rose 1.5% on the day of the release and added another 5.5% in the following trading session. Revenue increased 11.6% year-over-year (YOY) to $742 million, surpassing analyst estimates of $729.9 million.

Meanwhile, adjusted EPS climbed 22.4% from the prior-year period to $0.82, ahead of the Street’s $0.76 forecast. Subscription revenue reached $724 million, up 11% year over year. Remaining performance obligations (RPO) grew 17% to $4.292 billion. Current RPO (cRPO), which reflects revenue expected over the next 12 months, increased 13% to $2.328 billion.

Management attributed the outperformance to strong enterprise adoption of newer offerings, including Okta Identity Governance and AI-focused security tools. Looking ahead, management expects continued traction in AI security and improved sales productivity to support growth.

For Q4 fiscal 2026, the company guides for revenue between $748 million and $750 million, representing 10% YOY growth, along with non-GAAP diluted EPS of $0.84 to $0.85. For full-year fiscal 2026, management now projects revenue of $2.906 billion to $2.908 billion, up 11% YOY, and non-GAAP diluted EPS of $3.43 to $3.44.

Okta is scheduled to release its Q4 fiscal year 2026 financial results after the market closes on Wednesday, March 4. Analysts expect Q4 EPS to rise 16% YOY to $0.29. For full-year 2026, they project 212.5% growth to $1.25, followed by another 20% increase to $1.50 in fiscal year 2027.

What Do Analysts Expect for Okta Stock?

Analyst sentiment reflects tempered optimism. Eric Heath of KeyBanc Capital Markets maintains an “Overweight” rating while lowering his price target from $130 to $115. Junaid Siddiqui of Truist Securities also keeps a “Buy” rating and trims his target from $125 to $115.

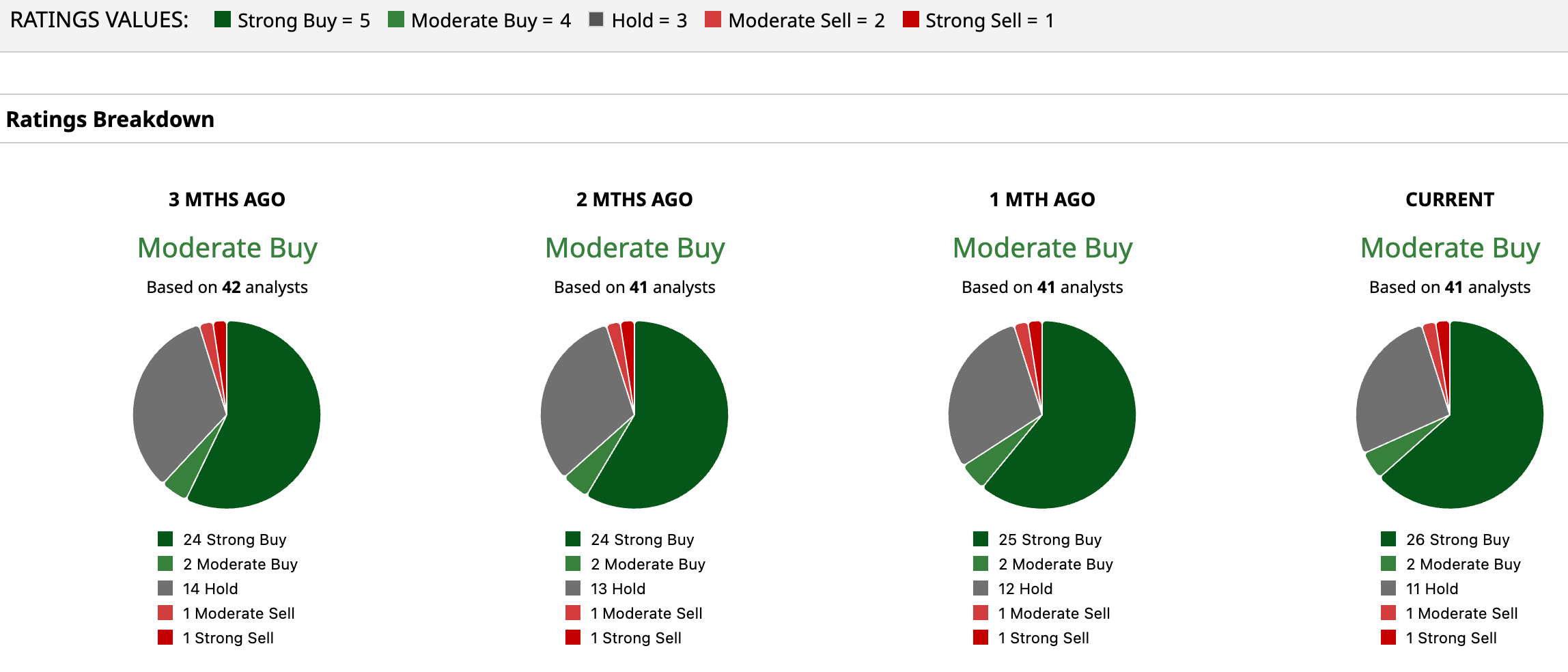

The reduced targets acknowledge near-term volatility, yet the maintained ratings signal continued confidence in long-term positioning. Thus, Wall Street assigns OKTA stock a “Moderate Buy.” Among 41 analysts, 26 rate the stock a “Strong Buy,” two assign a “Moderate Buy,” 11 recommend “Hold,” one issues a “Moderate Sell,” and one flags a “Strong Sell.”

To that end, the average price target of $110.41 implies potential upside of 52.3%. Meanwhile, the Street-high target of $145 points to a possible gain of 100% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)